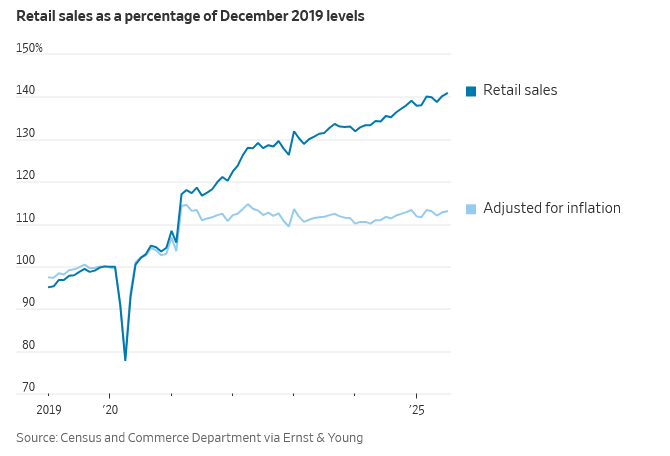

Another round of quarterly earnings reports has come and gone, and once again, many companies beat profit expectations. Yet a glance at the graph below from The Wall Street Journal, showing that retail sales have been flat excluding inflation, suggests that the ways in which companies are growing their earnings must be changing. The Wall Street Journal provided details on a “transformation” of earnings sources in Behind This Season’s Bumper Earnings. The bottom line of the article is that companies have had to increase productivity instead of relying on increasing revenues to drive earnings. Per the article:

The outcome of those transformations means less headcount, more productivity.-Damon Lee, CFO C.H. Robinson Worldwide

Some of these “transformations” include new technologies and cost-cutting measures, such as employee layoffs. While profit growth has benefited, the downside has been increased anxiety among the workforce, resulting in poor consumer sentiment and reduced spending, as recent data suggests. However, the expense cuts and layoffs have not been severe enough to trigger a recession. Gregory Daco, Chief Economist at EY-Parthenon, worries that this may still be on the horizon. Per the article:

My fear is that the longer this lasts, the more likely we are to enter something akin to a downturn

To his point, as companies run out of areas in which they can cut expenses and or add new technologies, they will become more reliant on layoffs to boost profit margins. A trend higher in the unemployment rate would likely confirm this is the case.

The article ends with another tool used by large companies to boost earnings, financial engineering. According to the article, share buybacks contributed to at least 4% of earnings (EPS) growth for one out of every six S&P 500 companies.

What To Watch Today

Earnings

(Click on image to enlarge)

Economy

(Click on image to enlarge)

Market Trading Update

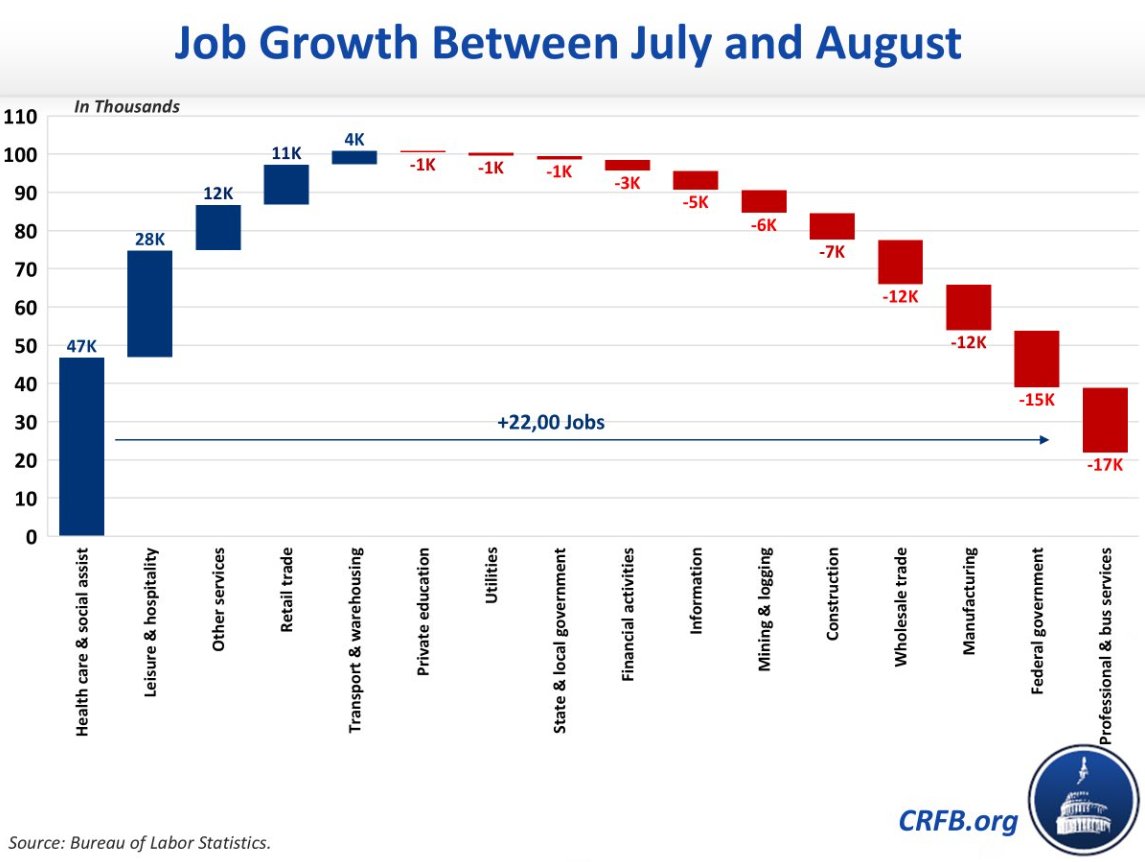

The August employment report painted a clear picture of a cooling U.S. economy. Employers added just 22,000 jobs, far below consensus expectations, signaling that hiring momentum has slowed. Even more troubling, June was revised to show a loss of 13,000 jobs, the first monthly contraction since 2020. Meanwhile, unemployment rose to 4.3%, its highest level in nearly four years. Job gains were concentrated in healthcare, while manufacturing and federal employment weakened further. Layoffs also surged, with about 86,000 job cuts announced in August, the largest total for that month since the pandemic years.

This weakness has several implications. First, it points to slowing economic growth as companies curb expansion and trim payrolls. Second, and more notably, a softer labor market reduces upward pressure on wages. That, in turn, eases one of the stickiest drivers of inflation. As wage growth cools alongside weaker hiring, consumer demand could moderate further, lowering inflationary pressures in the months ahead. That will give the Federal Reserve additional cover to shift from its more restrictive stance and join into the rate cutting race that is already happening globally.

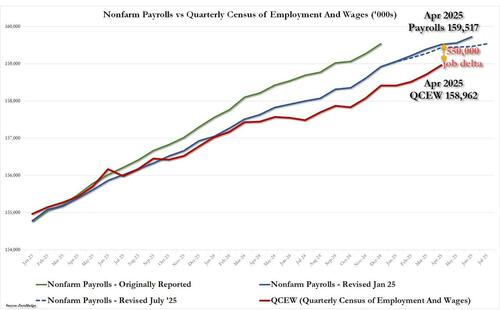

Next week, on Tuesday, we will also get the annual revisions to the BLS employment report. That adjustment will likely show that over the last 12-months somewhere between 550,000 to 800,000 fewer jobs were created than originally reported based on the QCEW report.

The bond market responded as expected. Bond yields fell as investors realized the disinflationary impact of slower employment and wage growth would increase recession risk. If the revisions to employment show a substantially weaker than expected outcome, bond yields will likely fall further.

(Click on image to enlarge)

But looking forward, the market faces a tug-of-war. Historically, lower interest rates support higher equity valuations by reducing discount rates and improving liquidity. However, slower economic growth directly pressures corporate earnings, particularly in cyclical sectors tied to consumer spending, manufacturing, and capital investment. If earnings revisions trend lower, the risk of the market questioning high forward valuations will increase.

Just a risk worth considering.

Outlook: Markets may remain volatile in the near term as monetary easing collides with weakening fundamentals. The balance of risks suggests that earnings deterioration could eventually outweigh the initial rate-cut optimism.

Technical Backdrop

The S&P 500 closed at 6,481.50 after hitting a record high earlier in the week. Momentum indicators remain supportive of further gains. The 14-day RSI sits near 58 and remains in a negative divergence with the market. At the same time, as the market trends bullishly, the risk of a corrective/consolidative period increases as relative strength erodes. The MACD further confirms that outlook, which suggests momentum is slowing. While there is a cluster of buying support at current levels, a break below the 50-DMA (~6350) will likely find a lack of buyers until the 200-DMA at ~6000.

(Click on image to enlarge)

However, the bullish bias remains for now. The index continues to trade above its 20-, 50-, and 200-day averages, and crossover signals from short- and medium-term moving averages confirm trend strength. Breadth also appears healthy, with multiple sectors participating in the advance, including technology, financials, and housing, which is an encouraging sign.

At the same time, traders should remain mindful of possible short-term headwinds, particularly as we move past mid-month, when corporate share buybacks will return to “blackout.” As noted above, with economic data already weak and seemingly getting weaker, a more substantial market risk remains earnings outlooks. If earnings estimates start to be revised lower, the valuation multiple currently paid by investors may be questioned. Still, the broader technical backdrop remains positive, and strong sector participation suggests that any dip is likely to be shallow rather than the start of a deeper correction.

Key support levels now sit at the 6,444 area (20-day moving average) and 6,350 (50-day moving average), which should provide near-term buying interest if tested. A break below the 6,350 level would open the door to a deeper retracement toward 6,000 (200-day moving average), though that level remains distant given current strength. On the upside, the immediate resistance lies at 6,525–6,550, the zone of recent intraday highs. A breakout above that range could target 6,600 as the next psychological milestone.

Outlook: The S&P 500 looks poised to extend its rally into next week, but traders should expect potential consolidation between 6,420 and 6,525 before a push toward 6,600.

The Week Ahead And Employment

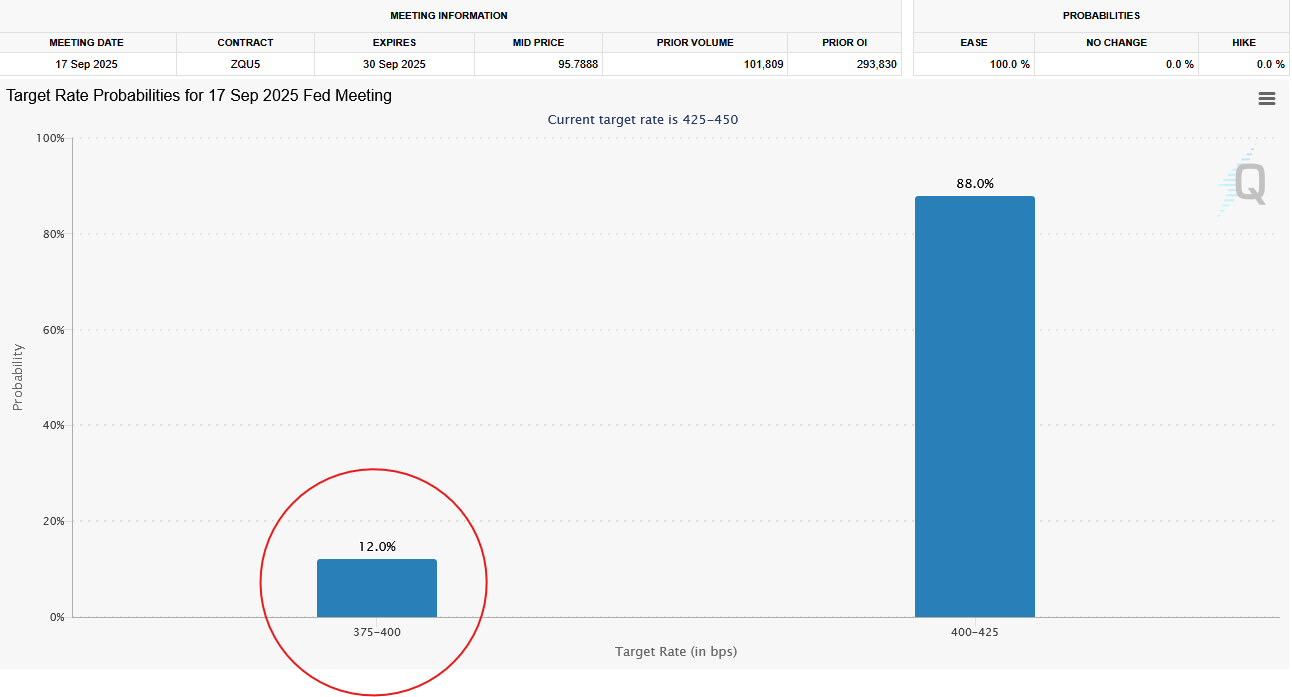

The BLS employment report once again shows very weak payroll growth. Last month, the economy added 22k jobs. Furthermore, the unemployment rate ticked up by 0.1% to 4.3%. Of concern, full-time jobs fell by 357k while part-time jobs rose by nearly 600k. As shown in the first graph below, 11 of the 16 employment sectors experienced job losses last month. Following the data release, the Fed Funds futures market assigned a 12% probability to a 50-basis-point rate cut at next week’s meeting. Weaker-than-expected PPI and CPI this week could further increase those odds.

With the FOMC meeting next Wednesday, this week’s inflation data will be the last piece of inflation information the Fed has to consider when making its decision. Following last month’s stunningly high PPI print, Wall Street estimates that it will rise by 0.6% this month. While below last month’s +0.9%, if Wall Street’s forecast comes to fruition, Powell may not be supportive of a rate cut. Even if the Fed does cut with a second high PPI number, talk of future rate cuts is likely to be limited.

CPI expectations are more tame at +0.3%. If PPI remains high while CPI sticks around current levels, corporate profit margins are at risk. Given that consumer sentiment is poor and recent spending has been weak, it should not be surprising that some companies are having to absorb much of the tariffs.

Federal Reserve members will be in a media blackout this week, heading into the September 17th FOMC meeting.

Why Keynes’ Economic Theories Failed In Reality

A recent post from Daniel Lacalle, “How Keynesians Got The US Economy Wrong Again,” exposed the widening gap between John Maynard Keynes’ economic theory and reality. Despite the confident forecasts of leading Keynesian economists, the U.S. economy in 2025 continues to defy expectations. The Federal Reserve’s tightening cycle failed to trigger the widely predicted “hard landing,” and growth has proven more resilient. Simultaneously, inflation remains somewhat sticky, but still declining, and the economy refuses to follow the neat, linear pathways that textbook models suggest.

This latest embarrassment for Keynes’ orthodoxy is part of a much larger story. The failures aren’t isolated miscalculations but the predictable result of a flawed framework that policymakers have clung to for decades. Keynesian economics didn’t just “get it wrong” in 2025, but has repeatedly failed to deliver on its promises for over forty years. And the consequences are becoming impossible to ignore.

At its core, Keynesian economics is deceptively simple. When demand for the private sector falls, the government should borrow and spend to fill the gap. The idea is that temporary fiscal stimulus injections will smooth business cycles, reduce unemployment, and quickly return the economy to full capacity.

Tweet of the Day

More By This Author:

Employment Sends Rate Cut Odds SurgingUsing MACD To Manage Portfolio Risk

Fed Policy Is More Restrictive Since Rate Cuts

Comments

Log in or sign up to join the conversation.