Back in the day, a double dog dare was often a kid’s first introduction to evaluating risk and reward. The rarely presented double dog dare happens when one kid dares another to do something foolish. Usually, the kid being dared asks for an incentive to complete the challenge.

When assessing a double dog dare, one usually first values the reward. Maybe there are a couple of candy bars or a soda for completing the challenge. Then comes the risk assessment. Does the potential to break an arm or leg exist? Maybe worse, at least in some children’s minds, what will the punishment be for being caught? Simply, is the reward enough to compensate correctly for the risks associated with the double dog dare?

Evaluating the risks and rewards of a double dog dare are not that dissimilar to equity investing, as we explain.

Risk-Free Rates

Investors should expect compensation in the form of capital gains and/or dividends/coupons commensurate with the investment risk. To help evaluate the amount of risk compensation the market is offering, investors need a risk-free return to base the evaluation.

U.S. Treasury securities are a perfect yardstick for this task. They are considered the only risk-free asset in the world. We can debate the merits of their standing all day, but regardless of your opinion, it is a fact in almost all investors’ minds. Further, we can easily find yields for investment terms ranging from next week to 30 years upon which to compare our risky assets.

BAAA

In our article, Goodbye TINA, Hello BAAA, we made the case that expected equity returns for the next ten years are about the same as Treasury bond yields. In the current pricing scenario, the premium paid to stock investors for taking risks is zero. Accordingly, the article makes the case that Bonds Are An Alternative to stocks.

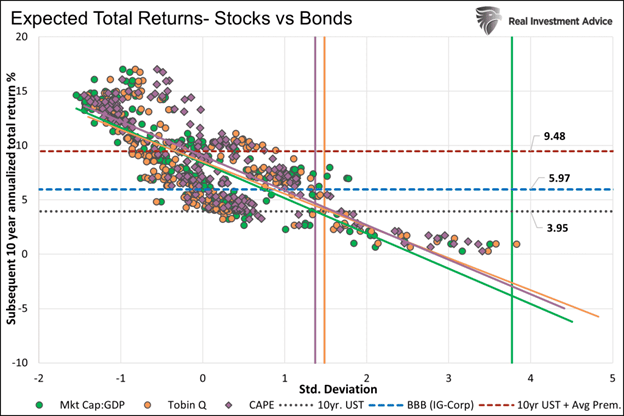

The graph below from the article shows that five popular methods for calculating equity expected returns range from 4% to -4%. At the same risk-free Treasury yields are near 4%.

Expected stock returns are on par with risk-free Treasury yields but woefully below the premium spread investors should demand. The simple conclusion is that for the entirety of the next ten years, bonds are the better bet.

Equity Risk Premium

In addition to the long-term stock-bond analysis presented in our article, there are other ways to help gauge whether stocks offer an acceptable premium to compensate investors for taking on added risk. One such model and the topic of this article is the equity risk premium.

The equity risk premium, like the three methods we share in the article, is a valuation-based calculation. However, it tends to rely on shorter-term fundamentals. Essentially our model looks at the expected EPS in one year divided by the current price and compares it to a 1-year forward UST bond yield adjusted for inflation expectations.

The higher the equity risk premium, the more compensation equity investors receive to take on risk.

The graph below charts the S&P 500 equity risk premium using trailing and forward earnings. We offer a special thank you to Kailash Concepts for supplying the equity data for the graph.

Fair Compensation?

Based on the graph, are equity investors fairly compensated for owning stocks? We can answer the question in a few different ways.

One way is to compare the current risk premium to recent pre-pandemic averages. As shown, outside of a few short-term instances, premiums have not been as low as they are today in 20 years. Further, those instances similar to today occurred after recessions, when the risk of another downturn was minimal, and earnings had significant upside growth potential as the economy recovered. While the premium was lower than average in those instances, the earnings and economic outlook were brighter, possibly justifying a low-risk premium.

Another way to consider the premium is to assess the risk associated with the current financial and economic environment and compare it to the premium. Today, given the potential market turmoil due to a possible recession, higher interest rates, inflation, an aggressively hawkish Fed, and the geopolitical situation in Ukraine, we should be paid more, not less compensation for taking on risk. The other consideration: playing it safe in bonds pays us a comfortable 4% with no risk.

Given the riskier-than-normal outlook and tighter-than-average risk premiums, bonds deserve more attention. BAAA!

How Equity Premiums May Normalize

Three key factors are used to calculate the equity risk premium: earnings, stock prices, and risk-free rates.

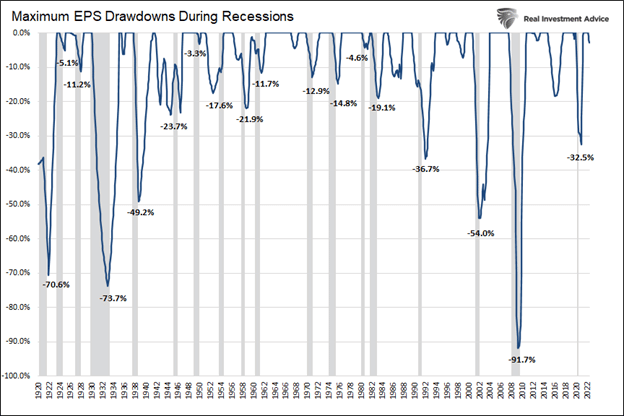

For the premium to rise to a more acceptable level, the numerator needs to increase, and/or the denominator falls. In other words, a combination of higher earnings, lower stock prices, and declining yields. We could create a complex table showing the many combinations, but instead, we think it best to focus on the elephant in the room – recession risk.

If we are indeed entering a recession, earnings are likely to fall. The graph below shows that earnings often decline significantly during recessions. If they do fall, the equity risk premium will also drop. Therefore, stock prices must also decline to keep the earnings yield stable.

However, the onus is not just on earnings and stock prices. If yields fall appreciably, the premium may rise. The bottom line is that all three factors will change. Appreciating what may change and to what degree, given various economic scenarios, will help you better appreciate how and when the equity risk premium may normalize.

Portfolio Management

The model presented above is for the S&P 500. Each stock has its risk premium. While we may not think the market is compensating us properly, many stocks and some sectors have potential earnings growth rates well above market levels with potentially fewer earnings volatility in a recession.

Portfolio management involves holding stock and bond assets. We believe in active management in which the allocations to stocks and bonds change as their risk-reward calculus changes. Lower risk premiums in a risky environment are leading us today to reduce equity risk.

Summary

“There is no analog. Today’s starting points are like none we have seen. The biggest risk is extrapolating to the future from a past that feels comfortable, confirmed by recent data. Disequilibrium is the new equilibrium.” Erik Peter One River Asset Management

The economic, financial, and geopolitical risks are outsized! Shouldn’t the equity risk premium reflect the situation?

If we double dog dares you to buy stocks, you should ask for a return that compensates for the additional risk in today’s market environment.

More By This Author:

One Monetary Policy Fits All - Part II

Our Currency, The World’s Problem - Part I

Finance Is At Fault, Not Russia, Powell, Or Biden

Comments

Log in or sign up to join the conversation.