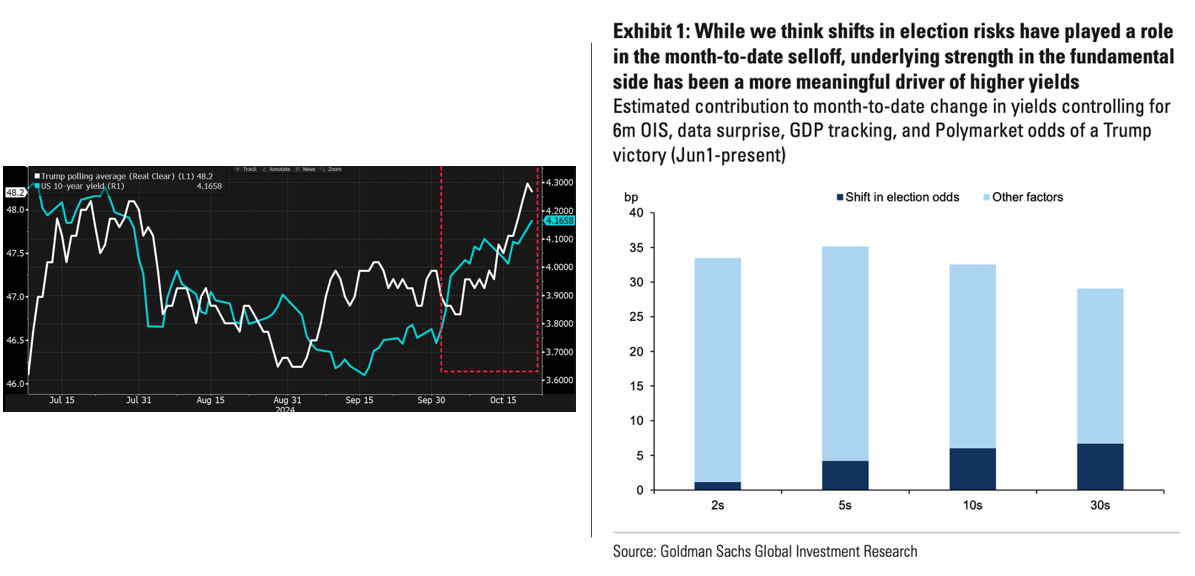

Bloomberg states: “The presidential race is still a coin-toss with two weeks to go, but Republican Donald Trump has the advantage over Democrat Kamala Harris in betting markets. His support for higher tariffs and looser fiscal policy has been seen as unfriendly to bonds because it means faster inflation and more debt.” Furthermore, the graph on the left supports their statement. It highlights that yields and the betting odds of Donald Trump winning have recently been well correlated. While one can make a narrative that Trump’s plans may result in larger deficits, inflation, and ultimately higher yields, we caution that correlation is not causation. In other words, the relationship between yields and Donald Trump’s reelection odds may not be as robust as some assume.

Two of our recent Commentaries (HERE & HERE) showed the correlation between bond yields versus oil prices and the Citi Economic Surprise Index surprise index. In both cases, the relationships are often strong regardless of the President and political composition of Congress. The Goldman Sachs graph on the right supports our opinion that economic and inflation fundamentals are primarily responsible for higher bond yields. Their graph attributes five basis points of the 35 basis points increase in ten-year yields to the shift in election odds favoring Donald Trump. We, Wall Street nor the betting markets, know who will win the election. Moreover, knowing which campaign promises will ultimately be enacted and which are vote-getting fodder is extremely challenging. Accordingly, focus on oil prices and economic data to assess the future direction of bond yields.

What To Watch Today

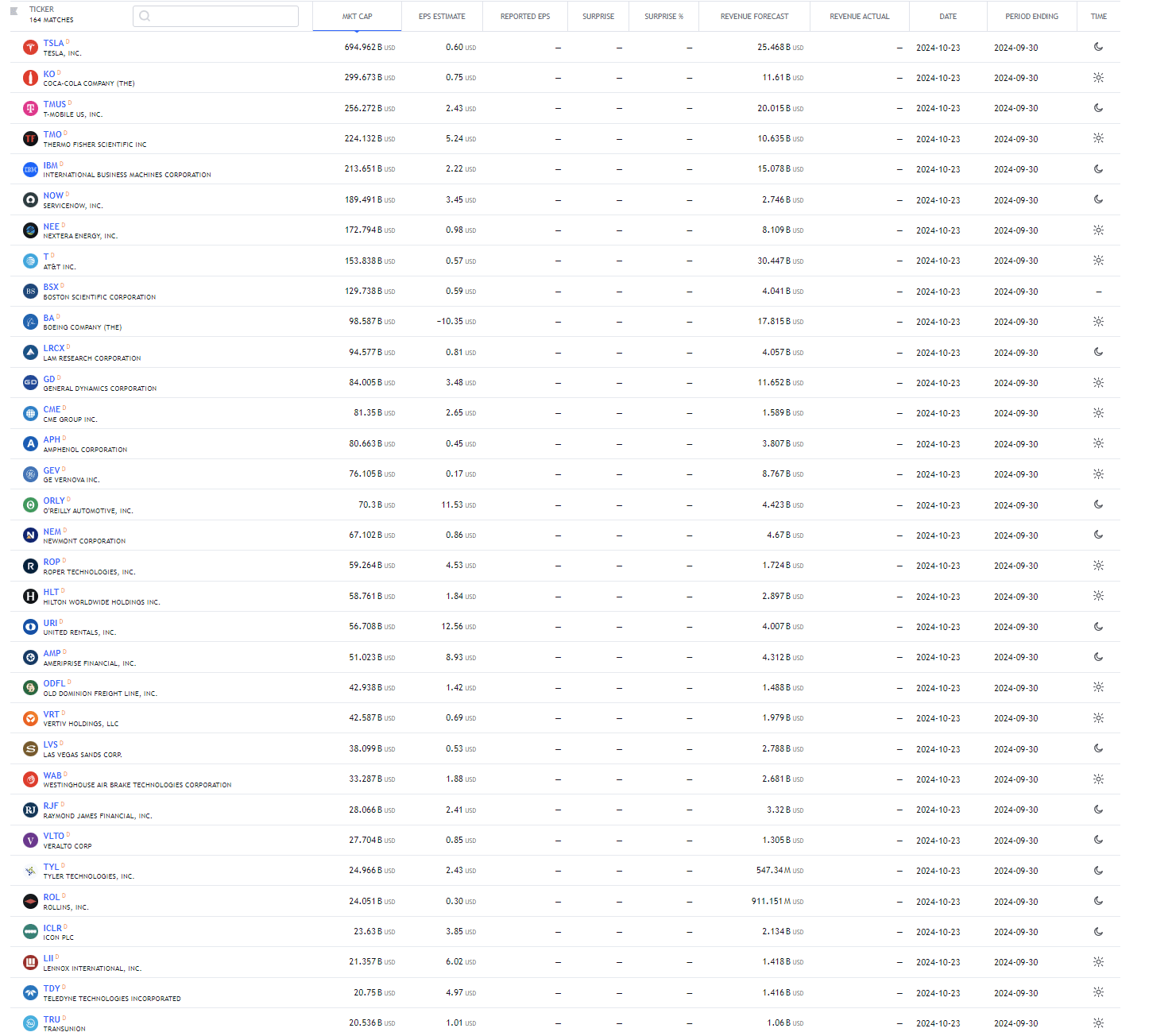

Earnings

(Click on image to enlarge)

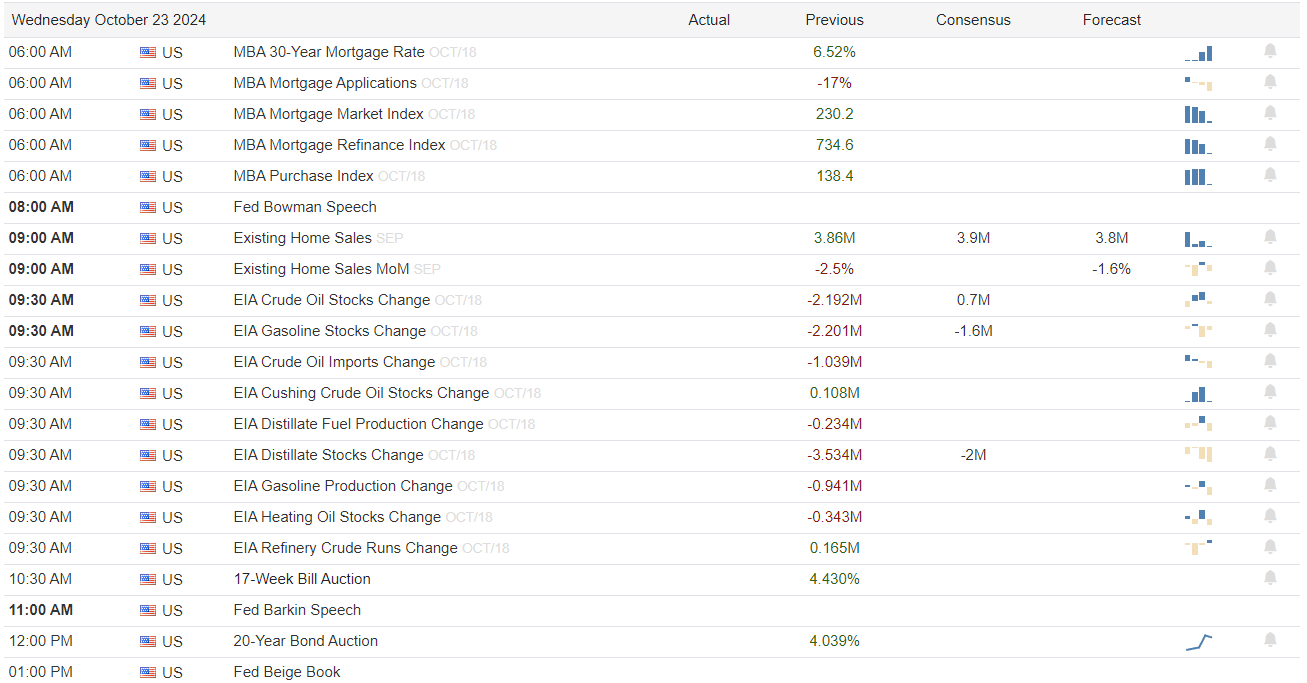

Economy

(Click on image to enlarge)

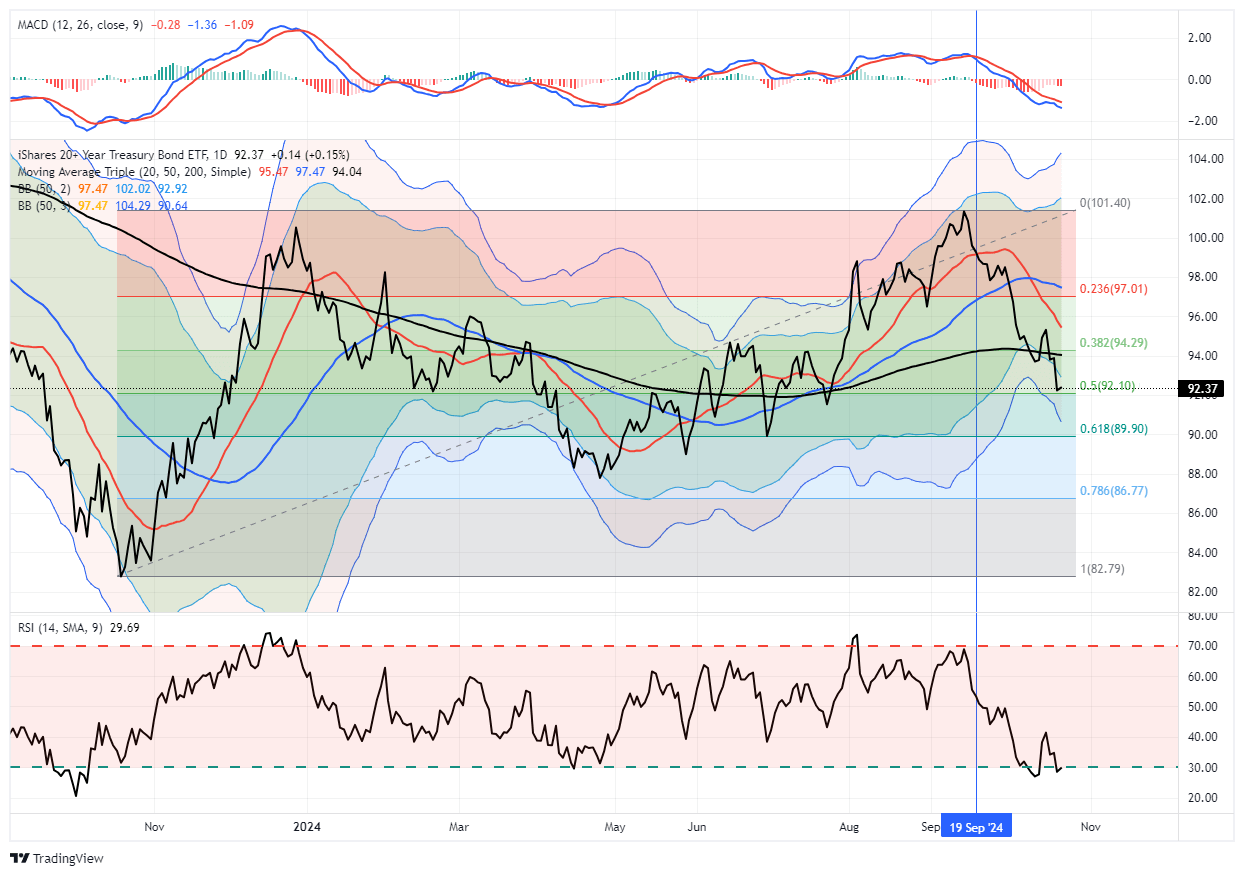

Market Trading Update

In yesterday’s update, we discussed the onset of seasonality and the market. The full blog post is linked below for your review. Yesterday, in my personal trading account (not our client accounts) I took a speculative long position in the iShares 20+ Year Treasury Bond ETF (TLT). I also bought December call options at the money for a trade.

My reasoning is purely technical. As shown in the chart below, TLT is pushing well into 3-standard deviations below the 50-DMA, with a deeply oversold MACD and RSI. Historically, it has been a decent setup for a reflexive trade higher, particularly after a 50% retracement of the rally from the previous lows. I am maintaining a short-term price target of $96-$98/share and will close out my call options early. However, the long position of TLT may well be maintained longer if evidence of economic weakness becomes more apparent, which I suspect will be the case.

(Click on image to enlarge)

So, why did we not do this for client accounts? Great question.

- In our client portfolios, we work to buy longer-term positions for capital appreciation and create tax efficiencies over time.

- This is my personal account. If I am wrong and lose money, I can live with that. However, I don’t speculate with our clients’ money, which they are dependent on for their financial goals.

- Furthermore, our client portfolios already have significant bond holdings. Taking on additional bond risk for a speculative trade will not create a return sufficient to warrant the increased portfolio risk and volatility.

However, I wanted to be transparent about my personal actions. We discussed previously why the recent bond correction was likely. I believe we have completed the correction between now and the end of the year..

We will see if I am right.

Bank Of Canada And The ECB Mull Faster Rate Cuts

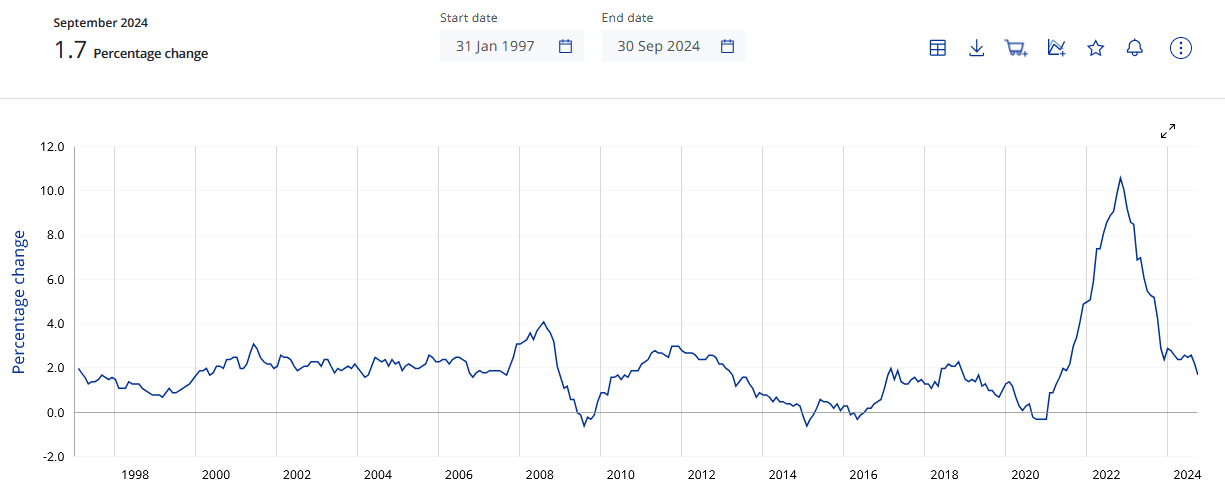

While the Fed and U.S. investors are backing off of rate cuts, other countries are moving to ramp up rate cuts. ECB member Mario Centeno sees the risks skewed toward undershooting its inflation target rather than higher-than-target inflation. With ECB inflation running at 1.7%, below its 2% target, Centeno will find support to cut rates more quickly from other voting members. The first graph below shows Euro inflation is back to normal.

The Bank of Canada is expected to cut rates by 50bps to 3.75% at today’s meeting. The action is being taken against the backdrop of lower inflation. The latest core CPI for Canada was 1.6%, as shown in the second graph. Per Bloomberg:

“Arguably the Bank of Canada is well behind the curve,” Jason Daw, head of North American rates strategy at Royal Bank of Canada, said by email. “They had to wait due to inflation uncertainties, but with price growth normalizing quickly, the economy no longer needs the current degree of restrictiveness.”

Global inflation is slowing and quickly returning to pre-pandemic levels. Quite frequently, inflation in most developed Western nations tracks each other. While U.S. inflation is still running above target, its trend and that of other countries, as we note, will likely keep the Fed cutting rates, even if economic activity remains firm.

Seasonality: Buy Signal And Investing Outcomes

For investors, this seasonality signal could be an opportunity to increase exposure to equities, particularly in large-cap stocks that tend to drive the broader market. However, it’s essential to recognize that while the MACD signal aligns with historical trends, it does not guarantee future performance.

Despite the historical reliability of seasonality and the MACD buy signal, investors must still be aware of risks.

- Monetary Policy: Inflation, interest rates, and global economic uncertainty could weigh on stock performance, even during a seasonally strong period. Given the recent bout of strong data, if the Federal Reserve slows the pace of rate cuts, this could disappoint markets. A good example is 2018, where the Federal Reserve’s more hawkish stance preceded a 20% correction in November and December.

- Geopolitical Risks: Ongoing geopolitical tensions, whether in Eastern Europe, the Middle East, or relations between major economic powers, can quickly disrupt financial markets. Unexpected events, such as escalating conflicts or trade wars, could derail the seasonal trends.

- Market Volatility: Volatility can spike unexpectedly, leading to sharp market corrections. Even during strong periods like the “Best Six Months,” short-term market corrections are always possible. Investors should be prepared for heightened volatility, especially if other risk factors, like earnings surprises or economic data, create uncertainty.

- Historical Trends Are Not Guarantees: Past performance, while instructive, does not guarantee future results. Although the MACD buy signal has been a reliable indicator in the past, external factors could reduce its predictive power. Investors must be cautious and not rely solely on seasonality and technical signals.

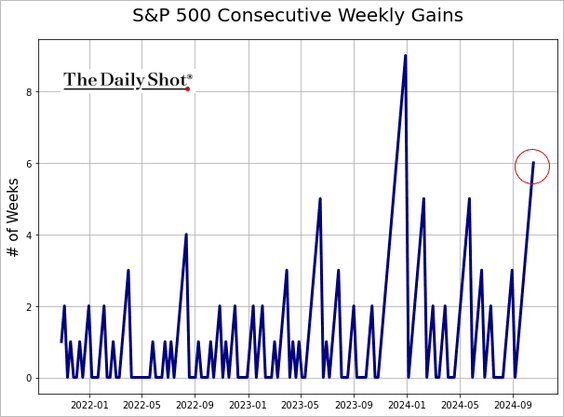

Most crucially, the technical backdrop also poses near-term risks. The market has been up six weeks in a row, which historically is a very long stretch without a correction.

Tweet of the Day

More By This Author:

Memory Inflation Warps Bond YieldsAmazon Is Challenging The Work From Home Trend

Seasonality: Buy Signal And Investing Outcomes

Comments

Log in or sign up to join the conversation.