Desperately Seeking Yield - Friday, May 5

Image Source: Pixabay

Trailing yields have increased for most of the major asset classes recently, based on a set of ETF proxies. The question is whether the relatively high payout rates offset concerns about the possibility of capital losses in the near term.

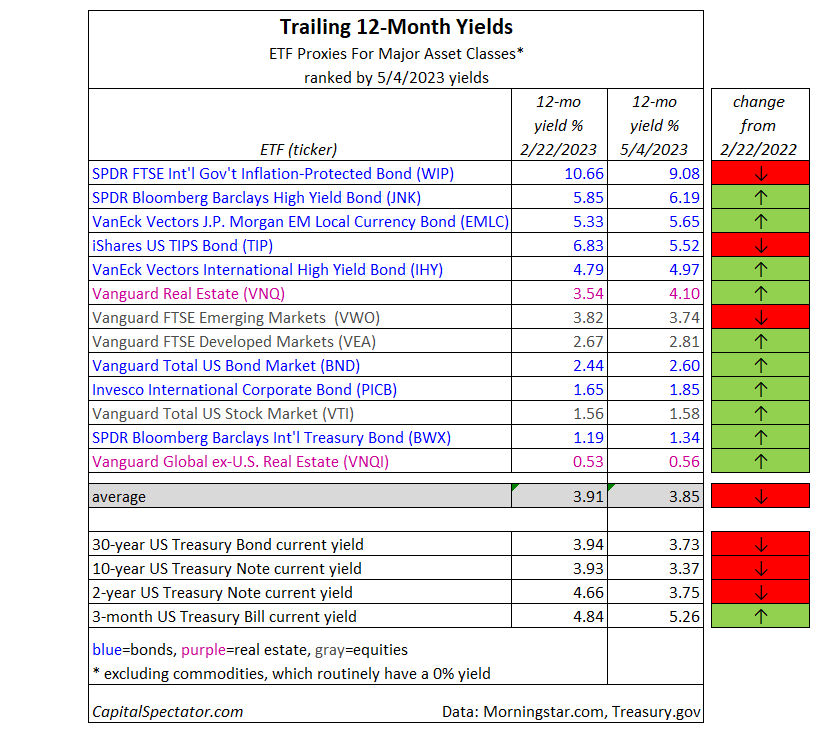

What is clear is that yields have generally edged higher since our previous update in late February. The highest payout rate by far is still found in inflation-protected government bonds ex-US (WIP), which topped 9% over the past 12 months, according to Morningstar.com. The average yield for the funds listed below is 3.85%. That’s slightly below the February update, but primarily due to an outsized drop in WIP’s rate. Excluding WIP reflects a slight uptick overall.

As always, a key decision for yield seekers is whether the safe-haven Treasury market offers a compelling alternative. A 10-year government bond, for instance, is currently yielding 3.37%, or about 50 basis points below the average yield for the major asset classes per the list above.

The 10-year rate is risk-free, of course, while the moderately higher trailing yield for the major asset classes overall can and will fluctuate and comes with no guarantee. Indeed, the standard proposition for assessing risk assets is that the trailing payout rate is only a guide for estimating the future.

Another factor to consider is the possibility that the Federal Reserve’s rate-hiking cycle has peaked. If so, bond prices look set to rise, which offers a capital-gain sweetener to Treasuries. Then again, if rates have peaked, the tailwind will likely support risk assets to some degree too.

“We expect the Fed to pivot to cutting rates once the battle against inflation is won,” notes Preston Caldwell, a senior US economist for Morningstar Research Services. “[Fed Chair] Powell stated that contingent on the Fed’s inflation forecast playing out (with the year-over-year inflation rate hitting 3.3% at the end of this year), it won’t be ready to cut rates then. But we expect inflation to fall faster than this, which is why we think the Fed will be ready to cut rates in December 2023.”

Meanwhile, investors can lock in a 3.37% yield in a 10-year Treasury with no risk. That’s well below the recent peak of 4.25% set in October, but it’s still near the highest level in over a decade. If the forecasts for lower inflation and an upcoming pause and then cut by the Fed are accurate, the 10-year Note’s total return will be competitive vs. pursuing yield in risk assets.

More By This Author:

Markets Consider A Path For Fed Pause And Cut On RatesFed Hike Expected Despite Ongoing Risks For Regional Banks

Total Return Forecasts: Major Asset Classes

Disclosure: None.