Credit spreads are critical to understanding market sentiment and predicting potential stock market downturns. A credit spread refers to the difference in yield between two bonds of similar maturity but different credit quality. This comparison often involves Treasury bonds (considered risk-free) and corporate bonds (which carry default risk). By observing these spreads, investors can gauge risk appetite in financial markets. Such helps investors identify stress points that often precede stock market corrections.

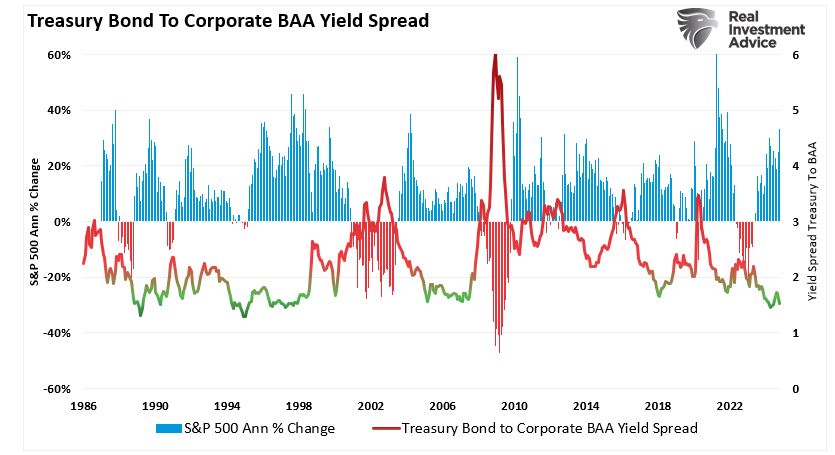

The chart shows the annual rate of change in the S&P 500 market index versus the yield spread between Moody’s Baa corporate bond index (investment grade) and the 10-year US Treasury Bond yield. Rising yield spreads consistently coincide with lower annual rates of return in the financial market.

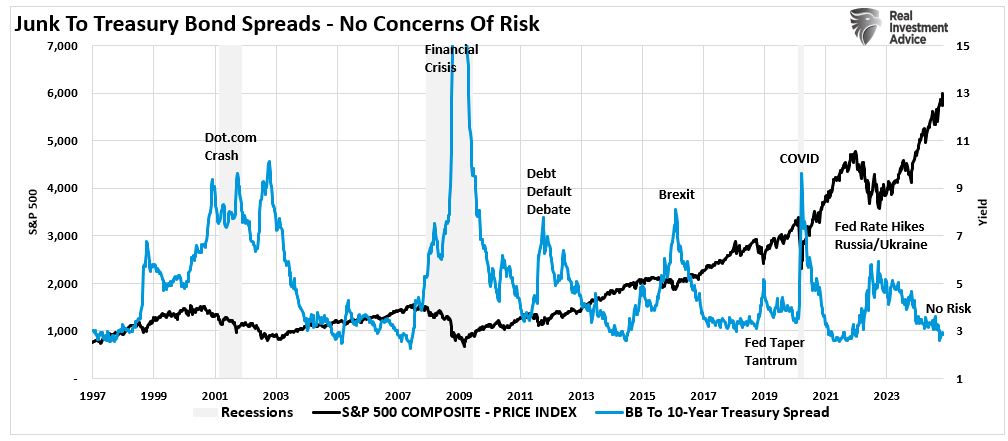

Another measure we watch is the spread between corporate “junk” bonds (BB), often referred to as “high yield,” to the “risk-free” rate of U.S. Treasury bonds.

The “Junk to Treasury bond” spread provides signals of market stress or impending market corrections. The reason is that if you are buying bonds that have a high risk of default (aka “junk bonds”), you should be paid a premium for the risk that is undertaken relative to the “risk-free” rate offered by U.S. Treasury bonds. The spread identifies when investors are willing to speculate in the markets and forgo the “risk premium.”

As shown, this has typically not ended well, which is why understanding credit spreads is important to investing outcomes.

Why Credit Spreads Matter

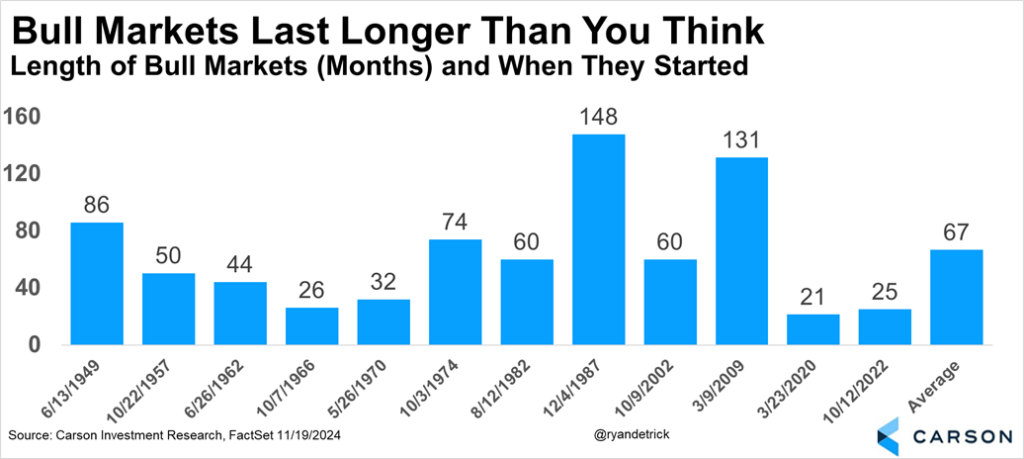

Many financial prognosticators on YouTube and other media suggest that an imminent crash is coming. This is understandable, given the substantial advance over the last two years. But just because the market has increased significantly doesn’t mean a crash is imminent. As Carson Research pointed out recently, the current advance following the 2022 correction is relatively young regarding months of advance. However, 1966, 1970, and 2020 show a reversion after a two-year advance is not out of the question.

However, credit spreads can greatly assist in determining the risk of a correction or bear market.

Credit spreads reflect the perceived risk of corporate bonds compared to government bonds. The spread between risky corporate bonds and safer Treasury bonds remains narrow when the economy performs well. This is because investors are confident in corporate profitability and are willing to accept lower yields for higher risks. Conversely, during economic uncertainty or stress, investors demand higher yields for holding corporate debt, causing spreads to widen. This widening often signals investors are growing concerned about future corporate defaults, which could indicate broader economic trouble.

The two charts above show that credit spreads are essential for stock market investors. Watching spreads provide insights into the health of the corporate sector, which is a major driver of equity performance. When credit spreads widen, they often lead to lower corporate earnings, economic contraction, and stock market downturns.

Widening credit spreads are commonly associated with increased risk aversion among investors. Historically, significant widening of credit spreads has foreshadowed recessions and major market sell-offs. Here’s why:

- Corporate Financial Health: Credit spreads reflect investor views on corporate solvency. A rising spread suggests a growing concern over companies’ ability to service their debt. Particularly if the economy slows or interest rates rise.

- Risk Sentiment Shift: Credit markets tend to be more sensitive to economic shocks than equity markets. When credit spreads widen, it typically indicates that the fixed-income market is pricing in higher risks. This is often a leading indicator of equity market stress.

- Liquidity Drain: As investors become more risk-averse, they shift capital from corporate bonds to safer assets like Treasuries. The flight to safety reduces liquidity in the corporate bond market. Less liquidity potentially leads to tighter credit conditions that affect businesses’ ability to invest and grow, weighing on stock prices.

Given the exceptionally low spread between corporate and treasury bonds, the bull market remains healthy.

The Most Important Credit Spread: High-Yield vs. Treasury Spread

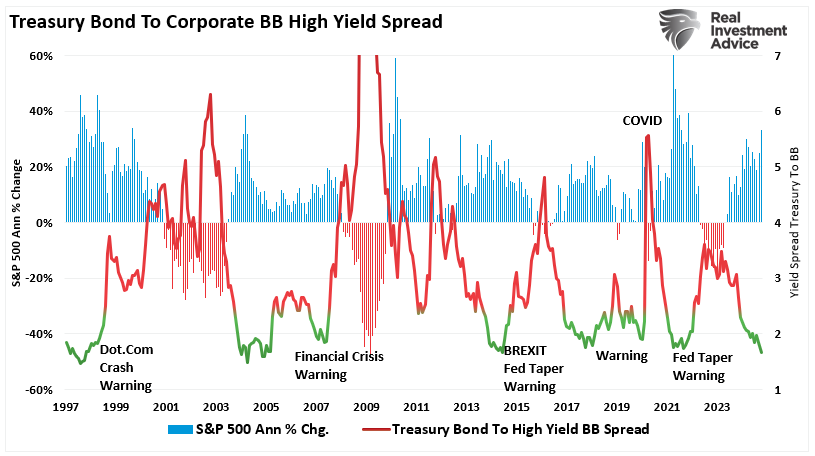

While there are several credit spreads to monitor, the high-yield (or junk bond) spread versus Treasury yields is considered the most reliable. That spread has been a reliable predictor of market corrections and bear markets. The high-yield bond market consists of debt issued by companies with lower credit ratings. Such makes them more vulnerable to economic slowdowns. As such, when investors become concerned about economic prospects, they demand significantly higher returns to hold these riskier bonds. When that happens, the spreads widen warning of increasing risks.

Historically, sharp increases in the high-yield spread have preceded economic recessions and significant market downturns, giving it a high degree of predictive power. According to research by the Federal Reserve and other financial institutions, the high-yield spread has successfully anticipated every U.S. recession since the 1970s. Typically, a widening of this spread by more than 300 basis points (3%) from its recent low has been a strong signal of an impending market correction.

Key Historical Examples:

- 2000 Dot-Com Bubble: Before the tech bubble burst, the high-yield spread began widening in early 2000, warning of increased corporate credit risk. As the spread expanded, the stock market declined steeply later that year.

- 2007–2008 Financial Crisis: The high-yield spread widened significantly as early as mid-2007, well before the 2008 stock market crash. Investors recognized the growing credit risk among corporations, particularly in the financial sector, which eventually led to the Great Recession.

- 2020 COVID-19 Crash: As the global economy ground to a halt, the high-yield spread soared in early 2020, anticipating the severe stock market correction that followed in March.

I reconstructed the chart above to show the Treasury Bond to Junk Bond (BB) spread versus the annual rate of change in the market. The spread between Treasury and “high yield” bonds rose before significant market corrections. Currently, that spread shows no sign that the risk of a more severe market correction is prevalent.

As investors, we suggest monitoring the high-yield spread closely because it tends to be one of the earliest signals that credit markets are beginning to price in higher risks. Unlike stock markets, which can often remain buoyant due to short-term optimism or speculative trading, the credit market is more sensitive to fundamental shifts in economic conditions.

A significant increase in the high-yield spread typically suggests that:

- Corporate earnings may decline: Companies with lower credit ratings may struggle to refinance debt at favorable rates, leading to lower profitability.

- Economic growth is slowing: A widening spread often reflects concerns that the economy is heading for a slowdown, which can lead to reduced consumer spending, lower business investment, and weaker job growth.

- Stock market volatility may rise: As credit conditions tighten, investor risk appetite tends to decrease, resulting in higher volatility in equity markets.

What This Means for Your Portfolio

If the high-yield spread does start to widen, it may be time to reassess your portfolio’s risk exposure. Consider the following steps:

- Reduce exposure to high-risk assets: This includes speculative stocks and high-yield bonds, likely to be hit the hardest in a downturn.

- Increase exposure to defensive assets: Treasury bonds, gold, and other sectors like utilities and consumer staples may offer protection in a volatile market.

- Review liquidity needs: Ensure your portfolio has enough liquidity to weather market stress without selling assets at unfavorable prices.

While bear market and crash predictions generate headlines, clicks, and views, most perennial calls continue to be wrong, leading investors to miss out on generating investment gains. Instead of listening to generally incorrect market analysis, credit spreads, particularly the high-yield spread versus Treasuries, are critical indicators for predicting stock market downturns. Historically, they have been a reliable early warning signal of recessions and bear markets.

However, there is no evidence that a “bear is on the prowl.”

When spreads do widen, we will certainly let you know.

More By This Author:

Bitcoin Is Entering Volatility Season

Market Forecasts For 2025 Are Very Bullish

Market Forecasts Are Very Bullish

Comments

Log in or sign up to join the conversation.