Bond Bull Market Coming? Take The Road Less Traveled

Over the past decade, historically low bond yields have converted many bond investors into bond traders. Bond traders strategically buy and sell bonds to generate price gains. A bond coupon, a primary reason many investors buy bonds, is nothing more than a bonus for traders.

Trading bonds is ages old and was typically dominated by institutional investors. Recently, however, the historically low yield environment and the liquidity and ease of trading ETFs make bond trading more commonplace among retail investors.

With the ten-year U.S. Treasury note yield eclipsing 2%, some bond traders think we are approaching another peak in yields. We know 2% seems low, but bond yields have trended lower for the last 30 years. Within the trend, each local peak in yield was followed by lower peaks as shown below.

With poor demographics, weak productivity growth, and a slew of new pandemic-related debt on the books, we tend to agree that another lower peak is probable.

For those agreeing in a coming bond bull market, we present a road less traveled. Closed-end bond mutual funds (CEFs) have a unique structure that, at times, can produce larger price gains or losses than bonds and higher yields than traditional bond funds or ETFs. If we are correct that yields will decline soon, some fixed income CEFs can produce double-digit returns in a relatively short period.

CEFs versus Open-End Funds and ETFs

Closed-End Funds (CEFs) are mutual funds with a fixed number of shares. Because of the structure, they trade on exchanges between investors. This unique feature often causes CEFs to trade at a premium or discount to their net asset value (NAV).

More traditional open-end mutual funds are always bought and sold through the fund’s management company at the fund’s NAV. As such, the share count on open-end mutual funds fluctuates daily with investor interest, but the daily price is always equal to its NAV.

ETFs can fluctuate slightly from their NAV, but dealers can arbitrage the difference when it occurs. Through the ETF creation and destruction process, dealers are financially incentivized to make sure the price of the ETF is very close to its NAV. Some unique instances exist, especially in the case of illiquid underlying assets, that entails such may not always be true.

CEF Return Components

Changes in the premium or discount from the NAV are an important differentiator between CEFs and open-end funds and ETFs. Further, the changing premium or discount can often result in over or underperformance versus other alternatives.

Given its importance, let’s consider the three biggest factors determining the premium or discount of a CEF.

- Supply and Demand. Strong demand and low supply of the fund may result in a premium, while weak demand and excess supply will often result in a discount.

- Quality of the fund management team. Investors may be willing to pay a premium for access to a management team that is highly regarded. Conversely, a discount may apply for managers perceived to be below average.

- The liquidity of the CEF and its underlying fund holdings. Often CEFs with unique or illiquid assets will trade at a premium as investors cannot replicate the fund’s holdings. As such, the more liquid the CEF trades in the market, the less volatile its premium or discount.

The change in the premium or discount to NAV is just one factor determining the total return for CEFs. The table below highlights other factors influencing the total return for CEFs.

| Total Return Factor | Comment |

| Price of underlying bonds | As yields decrease, prices increase, helping the total return. The opposite occurs when yields increase. |

| Dividend (coupon)/Yield | Many CEFs pay dividends monthly, unlike bonds which are often semiannual. |

| Discount/Premium divergence from NAV | A declining discount or rising premium versus the NAV result in positive price gains. Conversely, an increasing discount or declining premium reduces the price. |

| Leverage | Leverage used by many CEFs can amplify price changes (gains and losses) and dividends. |

| Expense ratio | The fee that the fund manager extracts from the CEFs return. |

Example of a CEF (NBB)

It is worth exploring a specific CEF to understand its unique structure better. We chose the Nuveen Taxable Municipal Income Fund (NBB). As its name suggests, NBB invests in investment-grade taxable municipal bonds.

As of February 21, 2022, NBB is trading at a 6.8% discount to its NAV. The most recent annualized yield is 6.09%. It employs 41% leverage on the portfolio, which boosts the yield. The leverage implies that each dollar of equity in the fund supports $1.41 of investments.

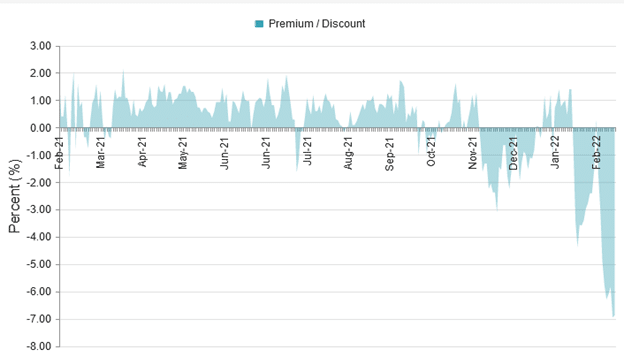

As shown below, courtesy of CEF Connect-Nuveen Funds, NBB traded at a 1-2% premium to its NAV for the better part of the last year. However, the recent spike in yields and inflation concerns are primarily responsible for the current shift from premium to discount.

The Math Behind CEF Returns

Let’s do some math to understand how changes in the discount or premium affect returns and importantly provide guidance if a bull market in bonds surfaces. If the current discount (6.8%) returns to a 1% premium, shareholders will earn about 7.8% in price gains. In addition, they would also receive monthly coupon payments and any NAV price changes over the period.

The fund has an effective duration of 7.60 years. Accordingly, if yields were to change by 1%, we expect the fund’s NAV to change by approximately 7.60%.

If we assume yields fall by 1% and investor concerns about inflation and higher interest rates abate, and NBB trades back to a 1% premium, investors will pocket a double-digit return. Such would be at least double what a municipal bondholder of the same bonds would earn. We caution that math works both ways. The discount could fall further, especially if yields continue to climb.

In 2018, NBB returned -6.38% as the Fed raised rates and embarked on QT. During that year, the discount to its NAV fell from -4.8% to a low of -9.5%, accounting for a significant portion of its loss. In 2019 the bull market in bonds was back on, the Fed reversed course, and the fund returned nearly +20%.

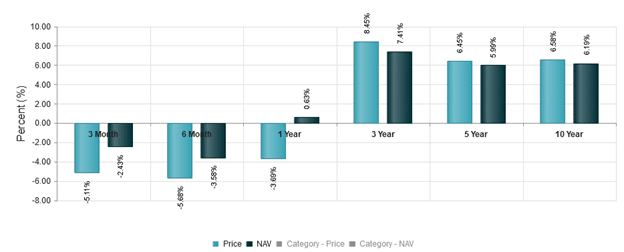

The graph below shows the fund’s returns over various periods. Note the 1-year NAV is up .63%, yet the price is down by 3.69%. The difference is a function of the current discount to NAV. Returns data from Nuveen’s CEF Connect can also be broken down annually to see how various CEFs did during bull and bond bear markets.

The Case for Lower Yields

We wrote the following paragraph in 2016. Now, six years later and we believe it is just as pertinent today:

“Having begun in 1981, the current bull market in bonds is well-seasoned and no doubt much closer to the end than the beginning. At the same time, the velocity of money is still declining in the U.S., the U.S. dollar is strengthening versus other currencies, and global deflationary forces emanating from abroad remain influential. The U.S. economy is more sensitive than ever to the level of interest rates, and economic stress resulting from higher yields can easily halt economic growth and push the economy into recession.”

Higher interest rates are starting to depress economic activity, especially in interest rate-sensitive sectors such as housing. There is little doubt that as the benefits of fiscal stimulus continue to erode over the coming quarters and the Fed raises interest rates, halts QE, and eventually reduces their balance sheet (QT), the economy will slow, and inflationary impulses will subside.

Such a result would help put a lid on rising interest rates and kick off the next bull market in bonds. Likely the bond markets will price for such an event in advance. While timing markets is difficult and yields can certainly rise further, we believe that yields will peak within the next few months, and CEFs will offer similar opportunities as in the past.

Summary

There are always opportunities in markets. Sometimes they are obvious and well followed by the public. Other times they lurk in underfollowed markets. We believe we are approaching a period in which bond yields will fall. While a typical investment in bonds, bond funds, or ETFs will prove valuable in such an event, CEFs can do even better.

Steep discounts to NAV and leverage separate CEFs from other fixed-income alternatives. While more volatile and riskier, they can also be more rewarding.

Disclaimer: Click here to read the full disclaimer.