It's been a while since the market witnessed a meaningful correction, as pullbacks have become brief and shallow in recent months. In fact, the market has not seen a 10% correction in almost a year. The last "market top" came right as I put out my "Warning Article" last September. Now, I am not saying that the market will fall apart today or tomorrow, but I expect a correction to materialize within the next several weeks, and here's why.

Yes, It's The Coronavirus Again

The first factor we need to discuss is the coronavirus. I know some of you are probably tired of hearing about it, but we cannot ignore the growing threat of this virus.

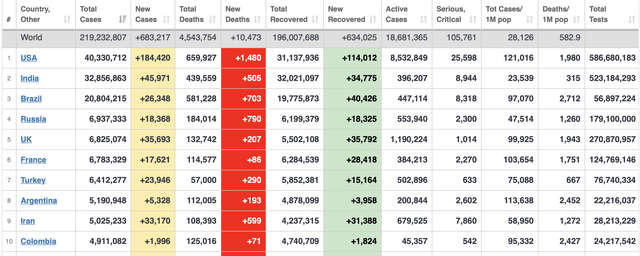

Source: worldometers.info

The U.S. continues to lead, and this is not a good thing. We see that the U.S. registered a whopping 184,000 new cases just yesterday. Moreover, the death count of nearly 1,500 people is exceptionally high. The coronavirus is not going away like many hoped that it would by now. Contrarily, things are getting progressively worse, and fall is just starting.

If we look at hospitalizations and other factors, the situation with the virus is worse now than it was a year ago. With over 100,000 hospitalized patients, it hasn't been this bad since the highs in January.

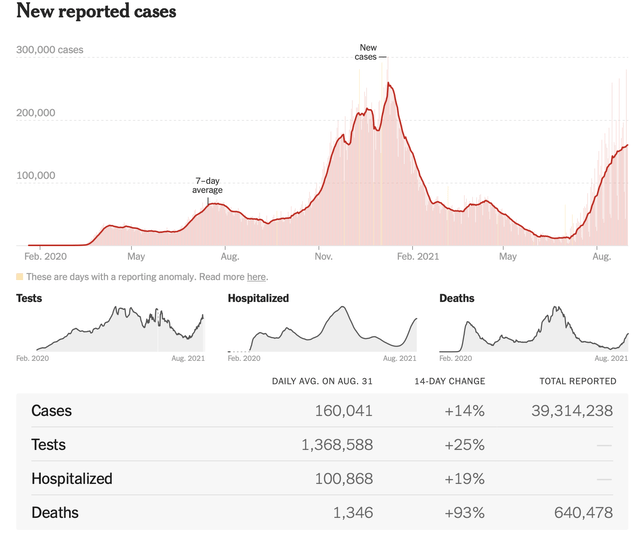

Source: nytimes.com

I wrote about the upcoming third wave about two months ago, and it looks like the situation with the coronavirus will get a lot worse. You can avoid these stats at your peril, but some of the figures are simply staggering. First, the seven-day average was only about 40,000 cases at the end of last August. Now we're looking at about 160,000, 4x as many. Next, look at the devastating death count of about 1,350, nearly doubling the number from two weeks ago.

Again, this is only summertime, and things will get progressively worse as colder weather months arrive. Less sun, more vitamin D deficiency, more indoor gatherings, the holiday season, the Delta variant and other mutations, the upcoming flu season, and an overly relaxed attitude towards the coronavirus could drive case numbers into the stratosphere this fall and winter in my opinion.

While about 50% of the U.S. population is fully vaccinated, don't let these numbers give you a false sense of security. Despite unvaccinated people being nearly 30 times more likely to be hospitalized, many Americans still refuse the shot. Polls indicate that anywhere from 20-25% of adult Americans will probably decline to get the vaccine. This phenomenon could make herd immunity a fantasy. Furthermore, we need to consider that while fully vaccinated people are less likely to be hospitalized or die from the coronavirus, they can quickly spread the virus.

The third wave is already materializing in the U.S., and an economic slowdown will probably occur as things advance into the fall. Now, this may not seem like anything new, but the market is pricing in substantial growth, and an "unforeseen" slowdown could cause the market to reprice equities.

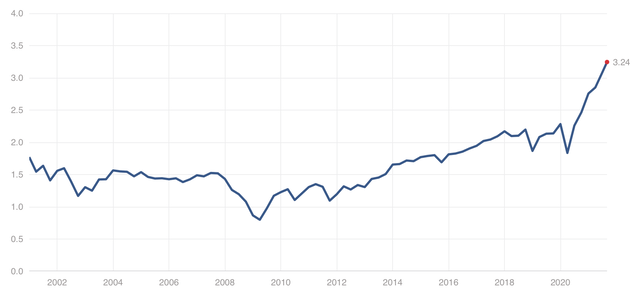

Valuations May be a Problem

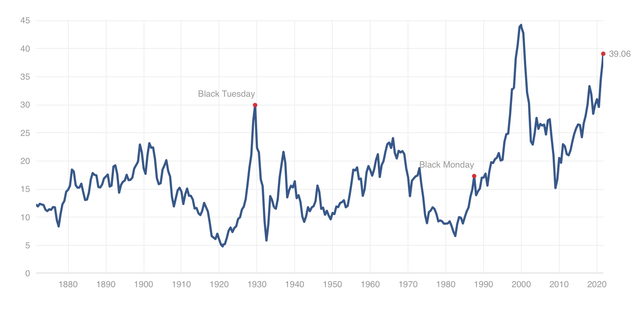

Shiller P/E Ratio

Source: multpl.com

We see the Shiller P/E climbing towards the ultra-frothy dot-com bubble-like levels. Could it continue to climb higher? Possibly, but it feels like this is an excellent time to get more cautious on equities here.

- Historical median: 15.85

- The percentage needed to adjust: 59%

- Plausible impact on the S&P 500: From 4,540 to 1,860

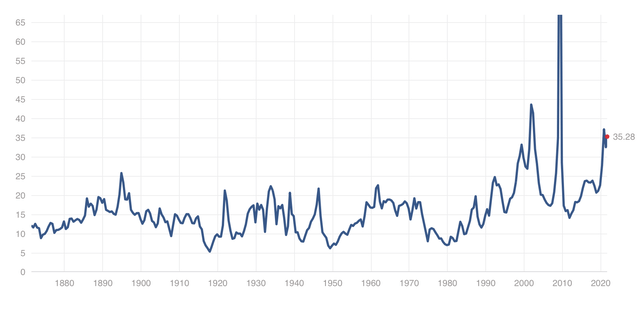

P/E Ratio

Source: multpl.com

If we exclude the skewed financial crisis P/E data, the S&P 500's P/E ratio is also approaching levels only witnessed during the fantastic boom and bust dot-com cycle.

- Historical median: 14.86

- The percentage needed to adjust: 58%

- Plausible impact on the S&P 500: From 4,540 to 1,900

Price to Sales Ratio

Source: multpl.com

The S&P 500's price to sales ratio is at its highest levels in history, eclipsing even the days of the 2000 bubble. This dynamic implies that stock prices are appreciating at record levels relative to their revenue growth.

- Historical median: 1.52

- The percentage needed to adjust: 53%

- Plausible impact on the S&P 500: From 4,540 to 2,130

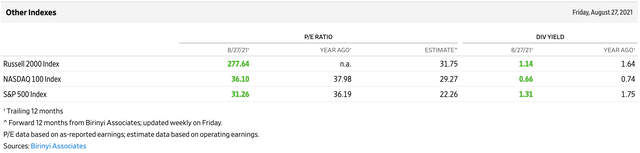

Analysts Are Too Optimistic

Extremely optimistic forecasts are a reason why ratios are so overextended here.

I'm even skeptical that estimates are realistic at this point

Source: wsj.com

For instance, while the trailing S&P 500 P/E multiple is around 31, the forward estimate is only 22. This elevated ratio is still about 50% higher than the historical median, but can it even be attained? With a possible coronavirus-induced slowdown approaching, are S&P 500 earnings going to rise by nearly 30% YoY? It seems that the current expectations may be too optimistic. As corporate profits begin to miss estimates, analysts could revise lower, which will likely cause stock valuations to adjust.

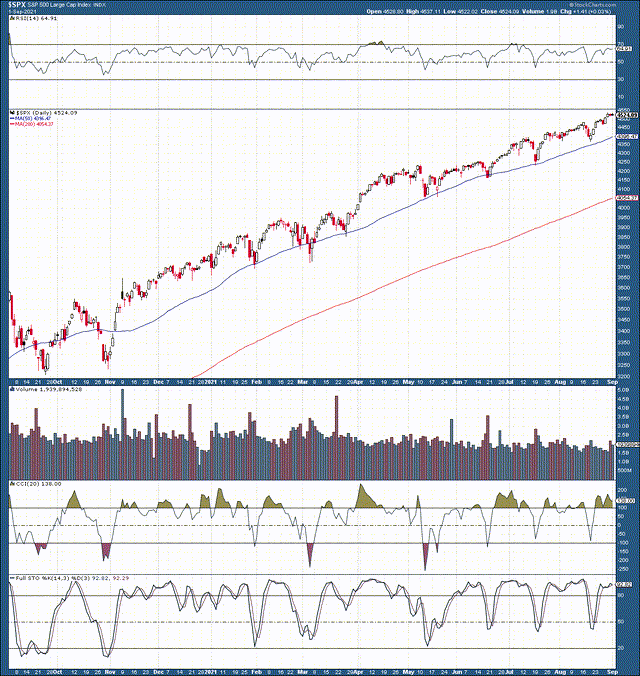

Technical Image

Source: stockcharts.com

The S&P 500 has not notably dipped through the 50-day moving average since the correction of last fall. We see numerous textbook 2-3% pullbacks that get bought up quickly just as the market touches down on the 50-day MA support. However, as fundamental factors start to weigh on price action, the S&P 500 could fall through support during one of these pullbacks, and a 5-10% correction will likely occur.

The Takeaway

While the market will likely continue to trade higher in the coming days, a notable correction is probably close. The Fed taper is coming and it should coincide with the continuous rise in coronavirus cases. The coronavirus phenomenon is perpetually getting worse, and the growing case count may not peak until the winter months. The dynamic of growing virus numbers coupled with the Fed taper will likely impact economic growth and corporate profits. Earnings may have peaked in Q2, and Q3 numbers may disappoint with slower growth forecasts and lower guidance. Therefore, analysts may need to reevaluate and lower their ultra-bullish forecasts. In this scenario, the market will very likely need to reprice the S&P 500 and equities in general to the downside. Thus, we should see a correction of about 10% materialize over the next several weeks (September/October).

Comments

Log in or sign up to join the conversation.