“It is elementary, my dear Watson” ---Sherlock Holmes

Daily investors are met with a barrage of claims that inflation is taking off, if not truly out of control. Reports are rife with examples of product shortages, labor shortages, jobs going begging, and all manner of goods and services experiencing price hikes. The central banks are coming under extreme pressure to raise rates as a means to rein in the inflation beast. Wall Street analysis have largely jumped on this bandwagon and widely expect that the Federal Reserve will raise its Fed funds rate, perhaps as much as three times during 2022. And, the Bank of Canada is expected to raise its policy rate at least as many times or more as the year unfolds. Many equity investors are nonplussed about inflation, citing that the opportunities available to increase revenues spurred by inflation. Investors of a certain age, however, recall the dismal stock market of the 1970s, featuring companies contending with ever-higher energy prices and wages demands. Amidst the confusion over inflation, let's look at how the economy will adjust to these inflationary pressures.

There is No Demand-driven Inflation

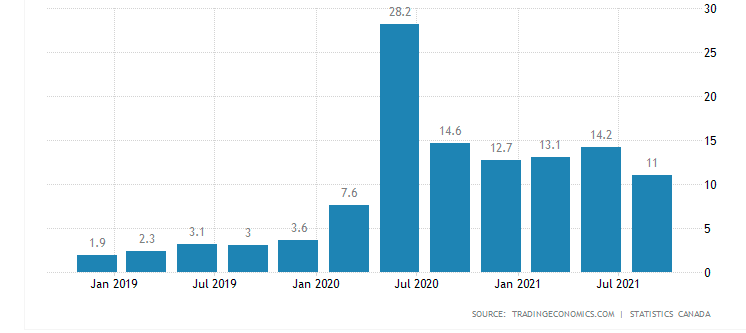

To begin with, North America is not importing inflation. Inflation is very low in China (2.5% y/y) and Japan (0% y/y). At home, consumers have not increased volume purchases significantly, that is, we are not buying more of everything as if the consumers were on a perpetual buying spree. There may be a lot of one-time purchases of goods, (e.g., bigger computers, exercise bikes, etc.) But we cannot expect these kinds of purchases to be made regularly during the course of this year and next. More importantly, the service sectors, (e.g., entertainment, food services, travel) are continually in a stop and start mode in response to local restrictions with each new wave of COVID-19. In all, total demand is not driving inflation. Should prices of non-essential goods and services continue to rise, we can expect the consumer to withhold purchases until prices fall. The best measure of why this is not a consumer-driven inflation is the rise in savings rates. Initially, the run-up in household savings rate was thought to be a strong factor in future consumption, boosting GDP. However, this “pent-up” theory of consumption never panned out. Canada’s household saving seems to be settling in and at around 12%, in stark to a rate of less than 5%, pre-pandemic. The consumer is very cautious and very concerned about the future.

Canadian Household Savings Rate

Supply Disruptions Ultimately Lead to Disinflation, Slowdowns

Globally, we have clearly experienced an unprecedented set of supply-side disruptions. The impact can best be explained by noting that the aggregate supply curve shifts inward, resulting in higher prices but, at the same time, lower GDP1. This drop in real GDP is what economists refer to as the “deflationary gap”. The Bank of Canada places considerable emphasis on the size of the “deflationary gap” which measures how far we are from our potential GDP growth path. Any widening of the deflationary gap, in turn, leads to slowdown economic growth. In some areas, the destruction in demand results in a fall in consumer prices. We only to have to ecall the 1970s when oil prices multiplied five-fold due to supply disruptions, then the economy slumped badly, ultimately leading to oil prices falling and disinflation setting throughout.

1 Imagine the X-axis as output and Y-axis as price, the supply curve moves inwardly so that any give price level output is smaller

Comments

Log in or sign up to join the conversation.