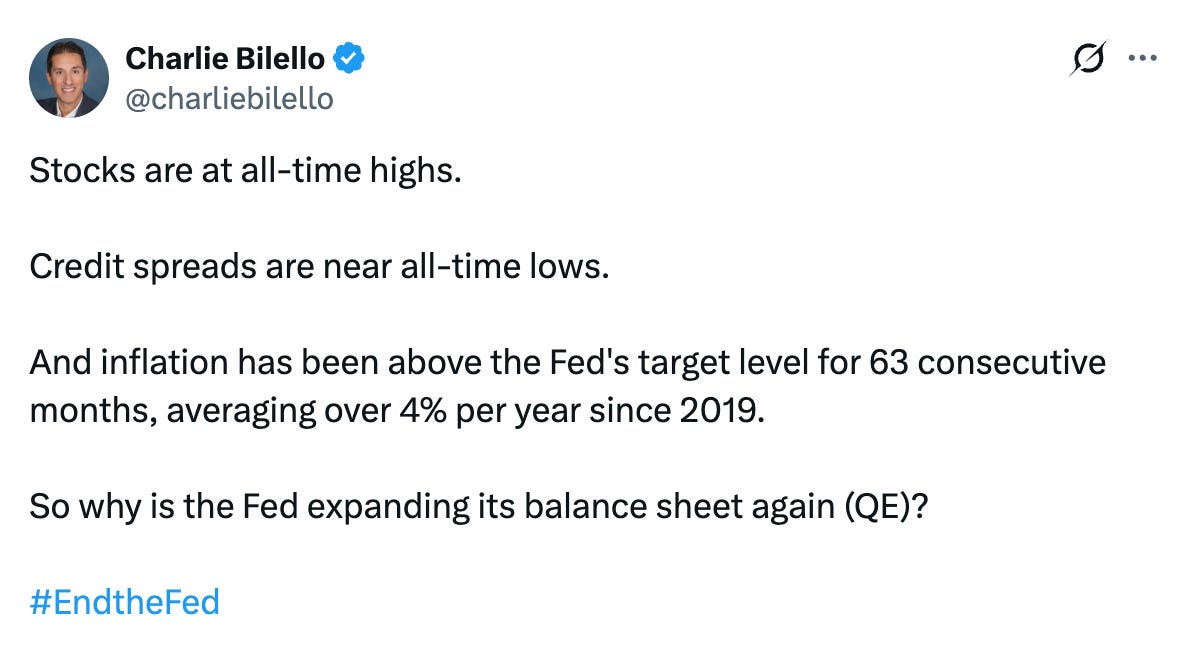

I don’t spend a lot of time on Twitter/X. But when I do, I’m usually looking at charts and conversations laid out by economist Charlie Bilello.

Charlie asked a question the other day that deserves a lot of attention…

If the stock market is at all time highs… and credit spreads are narrow, why is the Federal Reserve buying assets… why would they feed into the inflation machine?

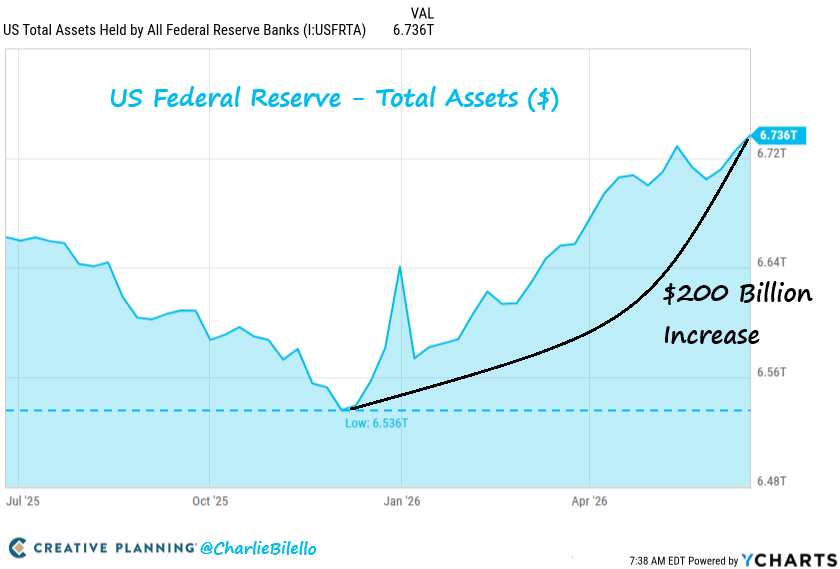

As Charlie explains… the Fed’s balance sheet has increased by about $200 billion in this chart (although when you add up other forms of liquidity, Lyn Alden and Michael Howell have hinted toward a much larger outcome in terms of fiscal support).

But this is about the Fed balance sheet…

There are six reasons as part of one bigger answer… and I’ll make them quick…

1. Treasury issuance is huge, structural, and tilted to the short end.

Federal deficits are over 6% of GDP and not closing on any current trajectory.

Net interest expense on the federal debt is now north of $1 trillion a year and growing.

To fund this without blowing out long-end yields, Treasury under Yellen and continuing under Bessent shifted issuance dramatically toward the front of the curve.

We’ve increased our front-end issuance from the mid-teens to around 22%.

T-bills became the funding vehicle of choice…

That keeps the long end from repricing and keeps headline rates politically tolerable.

But it requires constant rollover and constant absorption.

Trillions of dollars of bills per quarter, every quarter, forever.

Someone has to buy them. When primary dealers and money funds reach capacity at acceptable yields, the Fed becomes the marginal bid.

That is what reserve management means in practice.

2. Another 2019-style repo blowup is what the Fed wants to avoid.

In the fourth quarter of 2025, the Fed got busy again by stepping into the repo market. If you don’t know what the repo market is… well… it’s the machine of the underlying financial system… a market that sees roughly $12 trillion a day in transactions… while everyone else is too busy worrying about the Fed and rates…

The Fed and its press conferences are largely theater…

The real game is in repo… and it’s been the real story for about seven years.

On September 17, 2019, overnight repo rates spiked to 10% because bank reserves had drained too far.

The Fed had to scramble… so they bailed the whole thing out and started to buy again.

They opened standing facilities and wrote new rules, and now institutional memory of that day runs everything... Most people have forgotten about the impact of that day on markets because the COVID crisis started just a few months later.

But the funny thing is that the repo crisis in 2019 was probably a bigger deal than the actual problems that happened due to the pandemic for people who spend their days digging through BIS reports and drinking Mellow Corn after the market closes...

“You know me. I'm drinking my classic corn whiskeys all the time. It's just me and the open bar…” - Clay Bob Odenkirk, probably.

But get this… the Fed restarted this program that Charlie referenced - the Reserve Management Purchase program in December. And what else… they removed the Standing Repo Facility aggregate cap... They’re allowed do buy as much as they want… when they want… largely because of… the first reason above.

They are the same insurance policy. The Fed is putting a permanent floor under overnight funding because if repo goes again, the basis trade unwinds, hedge fund deleveraging cascades, Treasury market liquidity vanishes, and the whole leverage stack you saw in Episode 4 starts forcing sales.

That cannot happen. So they buy bills.

3. The non-bank financial system depends on stable repo. Full stop.

This is an extension of the previous two statements.

Hyun Song Shin at the Bank for International Settlements has been documenting this for three years.

Foreign central banks stopped accumulating Treasuries around 2012.

The marginal foreign buyer of U.S. sovereign debt is now leveraged hedge funds running cash-futures basis trades funded almost entirely in overnight repo.

That trade is estimated to be hundreds of billions of dollars in size.

It is the unspoken absorber of new Treasury issuance.

That basis trade… it’s tolerated. The safest asset in the world - the risk-free rate - is levered up to the tilt… a reminder that Bitcoin won’t cause a financial crisis… “safe” Treasuries will.

Remember, Janet Yellen said that leveraged funds were dumping Treasuries in April 2025… and the journalist interviewing her didn’t ask… “What the hell are you talking about?”

This entire system… it’s centralized and it runs on stable funding.

If the basis trade gets jumpy, the trade unwinds, and the Treasury market loses one of its largest functional buyers.

The Fed knows this and it can’t let the thing break…

So they just lie to us about their intentions… and they buy the Treasury bills.

4. Fiscal dominance has quietly arrived (but it’s not quiet at all to me).

Now… this goes back to work by Lyn Alden.

All roads point to what the Bank of Japan has done for decades…

It’s all about fiscal dominance. As Lyn says… “There’s no stopping this train…”

Fiscal dominance is the regime where central bank policy choices become subordinate to the government’s funding needs.

We’re living through it… good and hard. And when people complain about cost of living and other issues in the economy… they should be looking here…

But instead it becomes a conversation about trillionaires and billionaires.

Trillionaires and billionaires… I hate to break it to everyone… are a policy outcome.

But that isn’t going to stop the Jacobins.

Don’t underestimate the ability of economic ignorance to spread… fast.

They’re rising… and as fewer people understand fiscal dominance and the impact of the Fed… then the more social and political strife we’ll likely endure.

The Fed can’t tighten meaningfully without blowing up the fiscal arithmetic on debt service… and they can’t loosen rates aggressively without re-igniting inflation.

So they thread the needle by easing financial conditions quietly through balance sheet operations at the short end.

Reserve management is the legal cover.

The function is debt absorption.

And the political fallout will be a faster rise of socialism on the left and populism on the right… all while the center doesn’t have any clue how to explain the status quo.

Politicians who are trying to hold the center (and we need them), need to take 15 minutes and just read the latest BIS report. It’s utterly insane… and it explains so much about the problems we’ve endured since 2008.

5. Stealth liquidity supports risk assets… Who cares what you call it…

Again… an extension of what I just said…

Bills bought by the Fed free up bank balance sheet capacity.

That capacity can then absorb other assets.

Net liquidity expands across the financial system even when the headline framing says reserves are merely being maintained.

Equity markets read this exactly the way they read the original QE in 2009. Again, it doesn’t matter if they call it QE. What matters is whether the actions aim to achieve the same outcome of QE… which is financial stability…

Asset prices rise on every credible signal that the Fed is expanding, even supporting...

That isn’t a coincidence.

The market understands what reserve management is even if the press release does not say it out loud. Not explaining this to retail investors is a systemic failure of traditional financial media…

6. The structural growth path for the balance sheet is up, not down.

All roads point to more monetary inflation and currency debasement…

All… roads.

The Fed’s balance sheet was $900 billion in 2008.

It peaked at $8.9 trillion in 2022. It has shrunk since then but the floor is not $900 billion.

The floor is whatever level of reserves the modern fiscal-dominant, NBFI-dependent, leveraged-Treasury-market system needs to function without breaking.

That floor goes up over time, not down.

It happens every liquidity cycle, every fiscal restart, and every quiet expansion.

The next move is probably toward the $10 trillion level for the Fed balance sheet…

We’ll have another crisis… maybe they’ll blame climate change… and they’ll pump the living hell out of it… and the stock market will go up because there is a weird financial paradox where everytime we do QE or something like it… it leads to more foreign capital flooding into the U.S. markets…

Meanwhile, even if Kevin Warsh wants to run down this balance sheet… he’s going to run into gravity at some point. That’s what happened to Alan Greenspan.

Greenspan spent decades arguing against the very machine he’d ultimately run…

And when the credit markets froze in 1987… he had to make a choice.

The result in 1987 would have been the very thing that every doomsday person in the financial media world has warned about. That’s because 1987 remains so fresh in the mind of the people who have predicted 74 of the last 1 depressions.

They will not allow a debt-deflation spiral. It nearly happened in 2008 as well… and the only pathway for these central bankers was to turn the firehose back on.

They will do this until it breaks… and the fiscal repression can EASILY last another 20 to 25 years… The next pump will be bigger… not smaller.

So, just know that the balance sheet was never going back to pre-crisis size.

It was always going to ratchet higher across cycles.

The quiet buying of assets that started in late 2025 was the formal acknowledgment of that ratchet. It goes until it breaks…

So… one more time for my friends in the back

The Fed is expanding its balance sheet because…

The U.S. has crossed into a fiscal dominance regime…

The Treasury cannot fund itself at the long end at acceptable rates…

The non-bank leveraged buyer base requires stable overnight funding…

The 2019 repo trauma cannot be repeated, and…

The structural floor under the balance sheet ratchets higher every cycle.

Reserve management is what they’re calling it now. They’ll come up with another term at some point in the future for whatever facility they create next…

All that matters is that this is… really… Bond Market Central Planning…

Everything runs on top of it…

The Fed put is real, it is permanent, and it now operates through balance sheet plumbing rather than headline rate cuts.

So you need to own real assets and cash-flowing assets.

And the next time you hear a Fed official say reserve management, translate it correctly the first time.

Comments

Log in or sign up to join the conversation.