.jpg")

The Financial Times has an article discussing Argentine inflation, which remains stubbornly high in 2026:

Javier Milei’s push to bring down Argentina’s chronic inflation is stalling, with the monthly rate hitting 3.4 per cent in March — its highest level in a year — as economists warn that tackling the final stretch could be far harder than halting the crisis at its peak.

Inflation has fallen sharply from the double-digit monthly rates Milei inherited when he became president in 2023. But the monthly rate bottomed out at 1.5 per cent in May and hit 2.9 per cent in both January and February. . . .

The libertarian president, who wrote a book called The End of Inflation as part of his pitch to voters in 2023, has said inflation could soon “start with a zero”, meaning a monthly rate of less than 1 per cent.But economists are sceptical, particularly as the energy price surge caused by the Iran war adds fresh pressure to already sticky price dynamics. Its annual rate of nearly 33 per cent is a long way from its peak of nearly 300 per cent, but still among the world’s worst.

Two things struck me about the FT article. There is no mention of the money supply and there is no explanation for why Milei has refused to ask the central bank to control inflation:

The government has resisted committing the central bank to an explicit policy of targeting inflation. In the absence of such a framework as well as the abandoned exchange-rate anchor, the process has lost its engine, argues Gabriel Caamaño, an economist at consultancy Outlier.

“The disinflation process is at an impasse,” he said.

Yes. But why?

Milton Friedman famously said that persistent inflation is always and everywhere a monetary phenomenon, by which he meant a money supply phenomenon.

I’d say that high rates of persistent inflation are always and everywhere a money supply phenomenon.

I say “money supply”, because it is a tautology that inflation is a monetary phenomenon. After all, (by definition) inflation is literally the percentage decrease in the purchasing power of money. But while the value of money can change because of shifts in either the supply or demand for money, when inflation rates are persistently very high the cause is virtually always a rapidly expanding supply of money.

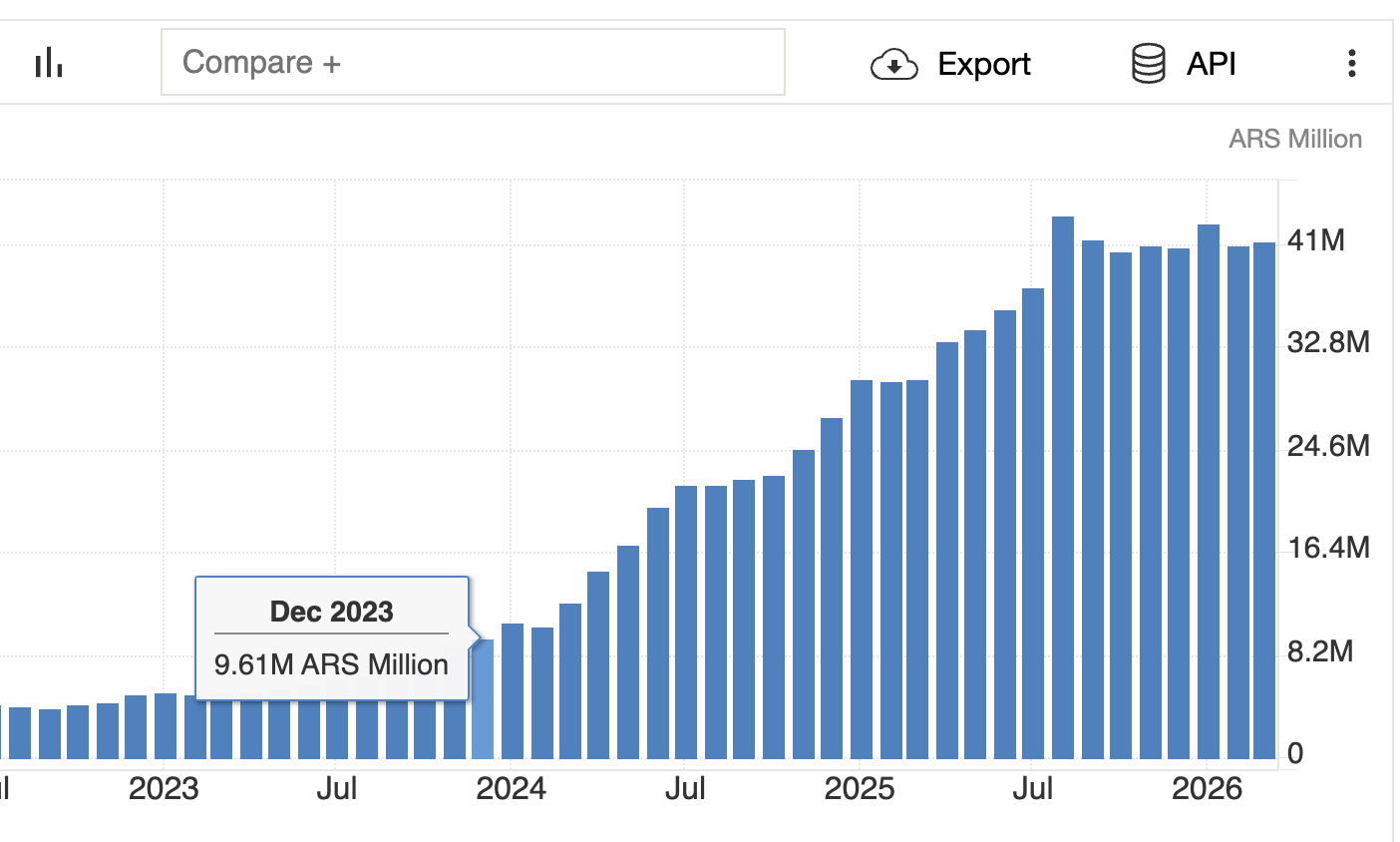

Here’s a graph from Trading Economics showing explosive growth in Argentina’s monetary base. Milei was elected in December 2023:

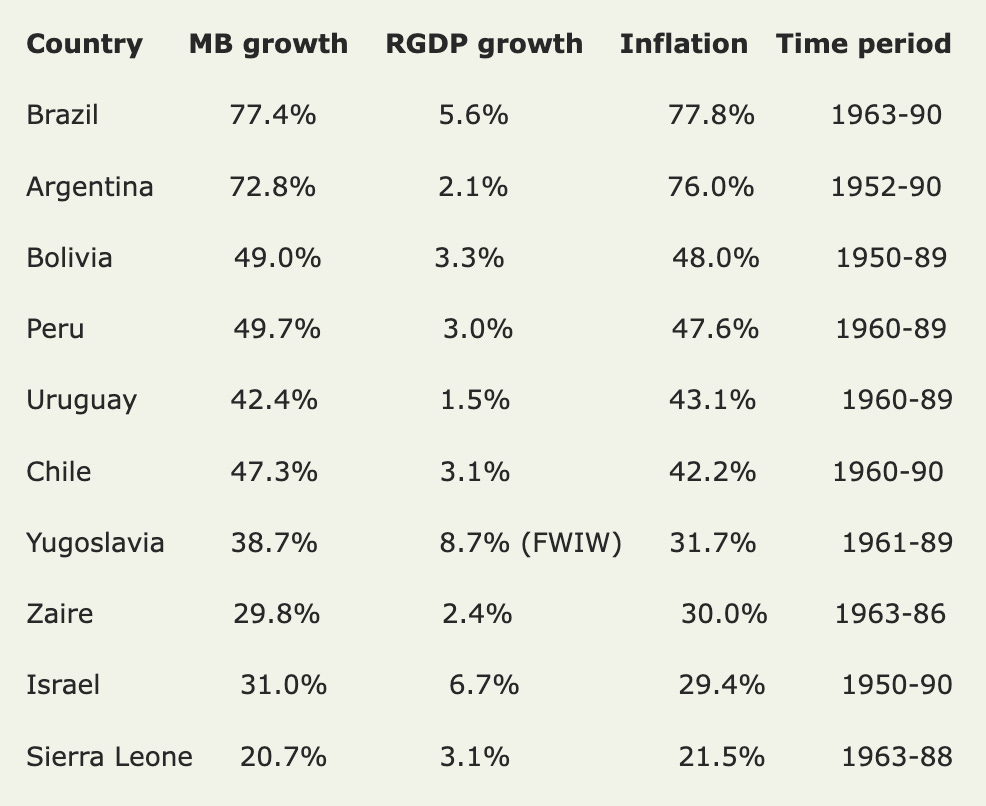

To be clear, it is not true that the inflation rate is exactly equal to the growth rate of the money supply. When inflation is slowing, as in 2024 and 2025, then real money demand tends to rise and inflation is usually less than the money growth rate. When inflation is accelerating, as in 2026, then real money demand tends to fall and inflation often exceeds the money growth rate. But over any extended period of time, the sort of extremely rapid growth in the monetary base that we see in Argentina will produce high rates of inflation. Notice the strong correlation between base money growth rates (annual averages) and inflation rates for the ten highest inflation countries in the mid- to late 20th century:

Comments

Log in or sign up to join the conversation.