Several Federal Reserve’s Board of Governors want to begin the process of reducing the size of the Fed’s balance sheet by the year’s end, according to minutes from last month’s meeting. This revelation creates considerable uncertainty as investors want to know:

- will the reduction take place before short rates are normalized;

- will all the assets will be shed or will some be retained indefinitely;

- how are they going to do this, e.g. sell assets or stop re-investing; and,

- what will be the ultimate size of the balance sheet?

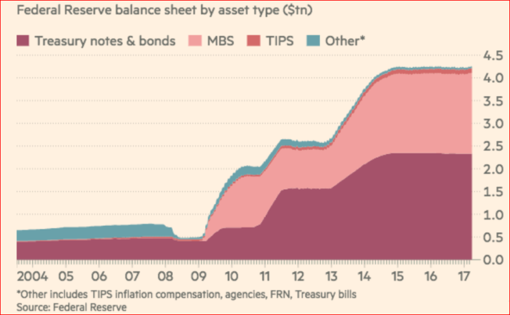

The Fed’s balance sheet has swollen from $869 billion in 2007 to $4.45 trillion as of today. Thus the effort to shrink the balance sheet will take a lot of careful doing and time. Currently, the Fed reinvests income into the same type of securities it holds and thus maintains the level and composition of Treasuries and MBSs so as not disturb those markets.

How will the markets react to the unwinding of the Fed’s balance sheet?

In 2011, for example, Bill Gross (then at PIMCO) shorted Treasuries in anticipation of the end of QE2 saying “ who will buy Treasuries now?” The trade backfired as the market interpreted Fed policy as a reduction in monetary stimulus and stocks went down and bonds prices went up.

In June 2013, the financial markets experienced some gyrating moments when the Fed announced that it would cease its third and last quantitative easing program. The so-called “taper tantrum” resulted in a 4.3 per cent drop in the stock market in a matter of three trading days and the yield on the 10-year Treasuries backed up by 55bps in less than two months. This time the bond market had a totally different reaction than in 2011. Many feared that the Fed, being the only game in town, would cash in their chips and force long-term interest rates to soar. It took the better part of a year for long-term rates to fall as deflationary concerns took the upper hand in the minds of traders starting when the oil price collapsed in 2014.

Now, the market is asked to consider a somewhat analogous case whereby the Fed slowly, but, surely, eliminates any stimulus by reducing its balance sheet. In turning his attention to the issue, Ben Bernanke advocates that the Fed bear in mind two points:

to minimize the risk that unwinding the balance sheet will disrupt markets and the economy, the best approach is to allow a passive runoff of maturing assets, …. even with such a cautious approach, the effects of initiating a reduction in the Fed’s balance sheet are uncertain. Accordingly, it would be prudent not to initiate that process until the short-term interest rate is safely away from the effective lower bound.[1]

That is, his approach is for the Fed to complete normalization and then turn its attention to the balance sheet. No doubt Bernanke does not want a repeat of the 2013 taper tantrum. But he does acknowledge that there is a lot of uncertainty on how the markets will react.

In sum, it is not all that clear why the Fed needs to shrink the balance sheet at all, considering that the international environment is so risky. As well, it is not as if the U.S. economy doesn’t have its own domestic problems - including extremely slow economic growth and poor industrial productivity.

In the past, the Fed has been able to function with a relatively stable balance sheet, and it could probably achieve its twin economic goals (the unemployment and inflation targets) simply by stabilizing the balance sheet, albeit at a much higher asset level than in the past.

Nonetheless, should the Fed decide to shrink the balance sheet, we agree with Bernanke that the correct approach is to do this by not renewing maturing securities. The one caveat to this approach is that by not renewing the mortgage-backed securities (MBS), the Fed maneuver would endanger the U.S. housing industry recovery as well as the mortgage market itself.

Comments

Log in or sign up to join the conversation.