Yellen “Brings It” and Bulls “Leave It” With Selling

Yellen emphatically declared to the market that she does not need a unanimous vote to return to a normalization of monetary policy. Inflation doves will argue that some slack exists in the Fed’s target inflation and that global economic weakness should not be ignored. However, Yellen isn’t interested in group think, which translates into “you may opine as you please, but in case you didn’t get the memo, I’m hiking rates now.”

The November-2015 ADP Employment Report (actual @ 217k vs. consensus @ 183k and prior revised @ 196k) and Productivity and Costs for Q3-2015 (non-farm productivity @ 2.2% vs. consensus @ 2.2% and prior @ 1.6%; and unit labor costs increasing @ 1.8% vs. consensus @ 0.9% and prior @ 1.4%) pretty much provide all the circumstantial evidence she needed to press her case for incremental interest rate hikes.

Performance Summary

Equities

- Volatility was back on top again as the major equity indices all retreated.

Bonds

- Treasuries split paths with the 30-yr bond rising on falling long-term rates while the 10-yr note pulled back slightly on more than a few upticks in rates. Perhaps the market perceives some risk to sustainable longer-term growth.

Currencies

- The U.S. Dollar Index closed above 100 while consolidating in preparation for another breakout.

- I say the above with some degree of confidence because the trend for the EUR/USD remains bearish and today’s weaker than expected November-2015 CPI data issued by the Eurozoneonly reinforces the thesis of monetary policy divergence from the Federal Reserve.

- Lastly, the abject failure of Abenomics (it’s the demographics, stupid!) continues to guarantee Yen weakness vs. Dollar.

Commodities

- Crude Oil surrendered key support after a bearish energy report (inventory supplies increased +1.2mm bbl vs. consensus @ -0.426mm and prior @ +1.0mm). The prospect of OPEC’s inner turmoil between the Saudis and Iran does not help either. Iran refuses to concede to further cuts in production as it has already suffered severely from economic sanctions. Yet, the Saudis do not want to be the only one doing OPEC’s heavy lifting. If Iran wants to be a regional power then it has to pay the price and share the burden with the Saudis. Good luck with that.

- Gold didn’t fare any better due to Yellen’s comments which point to normalized rates and a view that the U.S. economy is strong enough to reach full employment in lieu of slack in the inflation target, which she mainly attributes to lower oil prices.

Real Estate

- MBA Mortgage Purchase Applications for the week of November-27-2015 may have been exceedingly strong (purchase applications @ +8.0% mth/mth vs. prior @ -1.0%; and refinancings @ -6.0% vs. prior @ -5.0%), but it wasn’t enough to stop The Dow Jones Real Estate and Home Construction Indexes, both representing a capital market in which performance is levered to interest rates, from significantly underperforming.

*Trends: ST = short-term; MT = Intermediate-term; LT = long-term

Market Condition

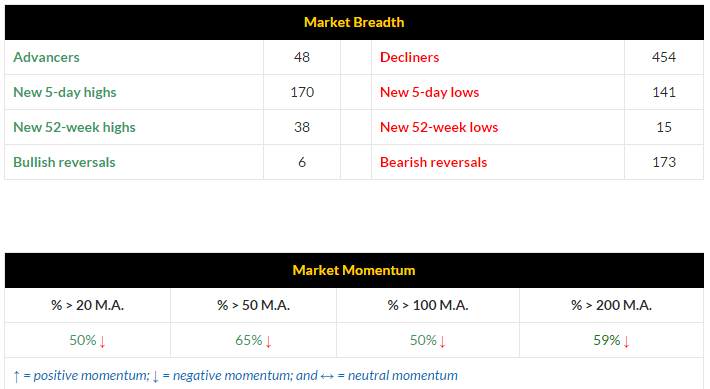

Yesterday I forewarned of the resistance at the lower channel of the previous uptrend. The SP-500 encountered collided with it today and got slammed. Market momentum came to a screeching haltas well. Like I said, things are starting to get interesting and today was anything but boring. The battle between bulls and bears is hardly over so don’t give up just yet. The current uptrend is still intact but a bit overextended. Further consolidation may be necessary. A pull-back after a breakout like yesterday is even healthy and normal. Today’s price action does not concern me as much as how the market responds tomorrow. Remember, the mark of a true winner is the ability to overcome setbacks and adversity. Let’s see how the bulls respond.

Keep Hillbent for the Market Direction…

Daily Chart Technical Analysis

Volume Radar Alerts

- Vol % = volume percentage greater than average volume

- SIR = short interest ratio or days to cover

Comments

Log in or sign up to join the conversation.