Image Source: Pixabay

April experienced another solid increase in jobs despite businesses struggling to find suitable staff. Wage pressures were not as intense as expected, but this is likely to be only a temporary lull. labor market tightness will keep upward pressure on inflation and the Fed hiking rates in 50bp increments.

Solid jobs gains, but wages undershoot expectations

The April jobs report shows that the labor market continues to strengthen with non-farm payrolls rising 428k, the same as the number of jobs created in March. The gains were spread solidly throughout all sectors with manufacturing posting a 55k increase, retail at 29k, trade and transport at 104k and business services up 41k. Leisure and hospitality continued to grow strongly with employment rising by 78,000 while once again it was the Federal government to be the only sector that lost jobs (-6k). Federal government employment is now down four out of the past five months.

While this is a good outcome markets may actually focus on other parts of the report. The unemployment rate held steady at 3.6% rather than dropping to 3.5% as expected, which in combination with a softer average hourly earnings figure of 0.3% month-on-month rather than the 0.4% consensus forecast (and slower than the 0.5% gain in March) may be taken as a signal of less inflationary pressures in the jobs market.

A lack of suitable workers will keep wages growth elevated

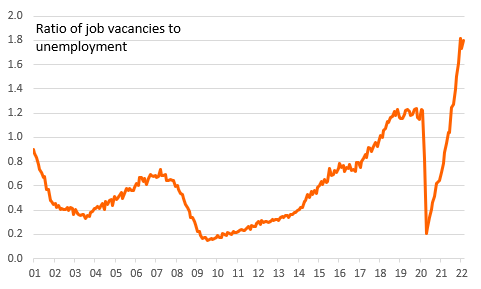

However, we don’t think this is the start of a new trend. The labor force participation rate fell quite sharply to 62.2% from 62.4% as 363,000 left the workforce. Consequently, the slower wage growth number might not last long as we know the demand for workers remains intense. After all, there are currently 11.55mn job vacancies in the United States while the National Federation of Independent Business (NFIB) reported that 47% of companies have vacancies they can't fill. If there are even fewer potential employees from which to choose, wages will continue to be bid higher

The ratio of job vacancies to the number of unemployed people

Image Source: DHI group, Bureau for Labor Statistics

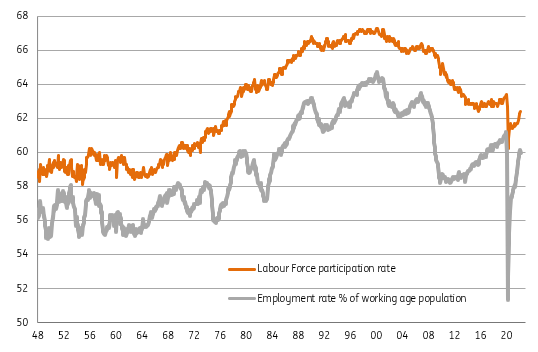

We should also point out that despite these solid job gains total employment is still 1.2mn below the February 2020 pre-pandemic peak. The numbers from the Job Openings and Labor Turnover Survey and NFIB report show that there is absolutely no issue with demand. The problem is the labor supply. The chart below shows the worker participation rate and also, more importantly, the employment ratio. It slipped to 59.9%, versus the 61.2% rate from February 2020 and well down on the 64.74% peak 22 years ago.

Employment ratios remain well down

Image Source: Macrobond, ING

Tight labor market to keep Fed hiking 50bp

Fed Chair Jerome Powell this week talked of optimism that labor supply will return, but we have seen little sign so far and we are skeptical that things will change soon. As such, we continue to expect a tight labor market that will keep upward pressure on employment costs. In an environment of decent corporate pricing power where firms can pass cost increases onto customers, this is a key reason why we believe inflation will be very slow to fall back to the 2% target. This would be fully consistent with the Fed continuing to hike interest rates in 50bp increments for at least the next three meetings.

Comments

Log in or sign up to join the conversation.