The Samuel Beckett play Waiting for Godot is about two people waiting for… well… Godot. Spoiler alert: Godot never comes. Is the wait for the return of the small cap effect the same?

The small-cap effect is the mooted long-term trend of smaller companies to generate higher risk-adjusted returns than their larger peers, compensating investors for their higher volatility and risk. This is premised on small firms’ faster growth potential, from a smaller base. However, UK small caps have outperformed only about half the time, on an annualised basis, over the past two decades, with the effect fading over time.

Over the past three calendar years, UK Smaller Companies funds returned an average of 12%, and over 2025, that figure was 4.12%. So, not much above inflation, for all that small-cap risk. The UK All Companies average return for the two periods was 33.35% and 15.35% respectively.

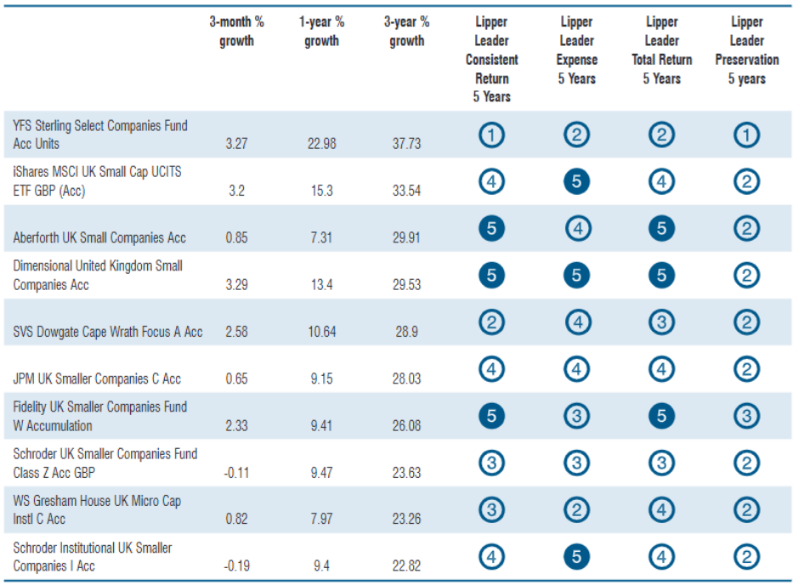

The top-performing small companies fund over three years returned 37.73%–not much above the average for the sleepy old dinosaur of All Companies.

So what’s happened to the small cap effect? Should we embrace big is beautiful, and move on? Certainly, that’s proved to be the market sentiment, with UK investors pulling £4.78bn from these funds over the past three years. But sentiment isn’t necessarily correct: over the same period, £55.28bn has been redeemed from UK equity funds, £17.88bn of it las year. Last year was the one where the FTSE100 was one of the best-performing global indices.

Will the FTSE drag its smaller sibling along behind it—will the rising UK market tide float all boats, both big and small?

Clearly that has not been the case so far, and for good reasons. The economic environment has been particularly trying for small caps. They struggled as bond yields rose and inflation expectations shifted, particularly because smaller firms tend to be more leveraged and thus more vulnerable to higher rates. Those higher rates ate into earnings, particularly for highly geared companies, which tend to be more the case for smaller companies.

UK large caps, by contrast, skew toward sectors that benefit from higher rates, such as banks, or are inflation‑resilient, such as energy and commodities. Valuations have also benefitted from these firms’ high levels of share buybacks.

What could turn the tide? Small caps tend to rebound harder and faster with an economic recovery. That’s not something I’m equipped to call, but worth bearing in mind, depending on your view of the world. Less speculatively, if rates continue to trend down, that could benefit UK smaller companies, as headwinds become tailwinds.

So far, investors are seeing the risk, less so the return in that risk-adjusted performance, and this is reflected in the sector’s consistent return scores, which are skewed to the lower end (1s and 2s) rather than the top (4s and 5s). Nevertheless, six funds retain their place in the table from last year, and five have the highest Consistent Return score: Aberforth UK Small Companies, Dimensional United Kingdom Small Companies and Fidelity UK Smaller Companies.

Unlike many sectors, where passives are high up the leaderboards, UK smaller companies still looks to be the territory of the active manager. Only one fund in the table below—the iShares MSCI UK Small Cap UCITS ETF—is a passive vehicle. However, this plain-vanilla ETF has crept from eighth place to second on our table over the past year, showing how hard it has been to add value through stock picking in this market—and also the corrosive effect of fees.

Bookending this piece, it would have been nice to finish with an uplifting Beckett quote, but that’s not really his style. So I’ll leave you with an uplifting statistic: despite all recent relative underperformance of UK small caps, the sector has still returned almost 350% over 20 years, compared with UK All Companies’ 230%.

Table 1: Top-Performing UK Smaller Companies Funds Over Three Years (with a minimum five-year history)

All data as of December 31, 2025; Calculations in GBP

Source: LSEG Lipper

Comments

Log in or sign up to join the conversation.