The San Francisco International Airport (SFO) is taxiing the tarmac with more than US$1.2bn worth of revenue bonds, as new supply in the U.S. municipal bond market is set to lift off.

Market participants have touted the total of around US$12.5bn of fresh muni deals in the week ahead as the busiest in 2019 for primary muni market sales, as demand remains squarely intact.

(Click on image to enlarge)

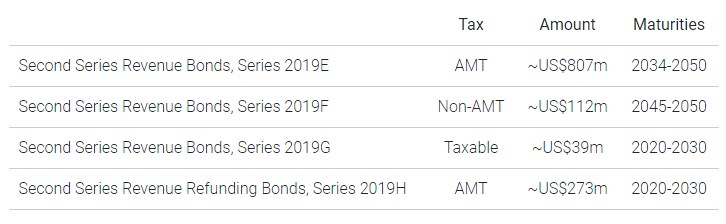

Among the deals on the radar, the Airport Commission of the City and County of San Francisco aims to sell second series revenue bonds in large part to help fund its recently approved US$7.6bn Capital Improvement Plan (around US$4bn of the CIP has already been funded). The SFO will also offer roughly US$273m of fixed-rate refunding bonds partly to repay certain variable-rate issuance.

The basic structure of the fixed-rate transaction:

(Click on image to enlarge)

The SFO mandated Bank of America Merrill Lynch and Barclays to jointly lead manage the offering and will be holding a round of investor meetings from August 6 through August 13.

The deal is set to price August 14 and close September 10.

According to Fitch Ratings, which assigned an investment-grade ‘A+’ credit rating to the transaction, SFO’s debt level is “high” at US$6.2bn as of fiscal year-end 2018 and contributes to the airport’s “high fixed-cost structure.”

The Airport Commission said it plans to sell almost US$3.8bn in new debt between September 2019 and May 2023, while assuming an estimated US$3.35bn worth of project costs.

(Click on image to enlarge)

Fitch analysts Jeffrey Lack and Emma Griffith noted that while additional borrowings to support capital spending will cause debt metrics to temporarily rise, “they should remain reasonable for an international gateway with stronger assessments for both revenue risks (volume and price).”

In any case, they added the airport has a “good” liquidity position and “stable” coverage levels, “demonstrating it can adequately meet its debt service obligations.”

Fitch expects SFO’s debt service coverage ratio (DSCR) to remain around 1.4x through fiscal 2023, including permitted transfers from its contingency account (1.1x – 1.2x without).

Meanwhile, SFO’s latest deal also falls against a host of headwinds for airliners, including certain challenging financial conditions such as Boeing’s (NYSE: BA) ongoing woes with its 737 MAX and Lufthansa’s (OTCMKTS: DLAKY) low-cost competition threats in Europe, as well as fuel cost concerns and protest-inspired international flight disruptions.

Furthermore, Hong Kong Airlines, which has been beset by deteriorating finances, as well as the ongoing protests in Hong Kong, said it will suspend its scheduled services between Hong Kong and San Francisco from October 5, 2019 following a review of its network and a change in business plan for the U.S. market.

Planned Improvements

Elsewhere, in terms of improvements, SFO’s CIP comprises two categories of projects – the Ascent Program Phase I and an Infrastructure Projects Plan.

The Ascent Program – Phase I – involves US$7.3bn of capital spending through FY2024 and encompasses 48 individual project categories. It mainly addresses aging infrastructure, as well as airline and passenger growth-related needs.

(Click on image to enlarge)

The Infrastructure Projects Plan is expected to deploy US$350m of capital spending on 18 separate projects through FY2023, including support systems, airfield improvements, energy efficiency and equipment.

The Airport Commission said that it expects US$2.4bn of project costs to be bond-funded in order to complete the CIP after the issuance of its Series 2019E/F/G/H debt.

Munis: The Demand Side

In the meantime, market participants generally anticipate municipal bond deals will continue to meet with healthy demand even as yields on U.S. government bonds sink, amid trade war uncertainties, as well as a host of other geopolitical worries.

The yields on the 10-year U.S. Treasury note and 30-year bond were last at around 1.76% and 2.31%, respectively, intraday Monday.

Analysts at Janney Montgomery noted they “do not expect the lowest yields in nearly three years to limit demand,” as bond investors continue to “pour cash into muni funds.”

In fact, for the week ended July 31, Thomson Reuters/Lipper U.S. Fund Flows reported a net inflow of roughly US$392m into municipal bond funds – not including ETFs such as the iShares National Muni Bond fund (NYSEARCA: MUB) and the Vanguard Tax-Exempt Bond fund (NYSEARCA: VTEB).

The report marked the 30th straight week of inflows into tax-free funds, contributing to a year-to-date record in 2019 of around US$60bn.

Janney Montgomery also observed the yield on the 10-year tax-free benchmark ended last week 9bps lower, capturing less than half of the 10-year U.S. Treasury yield’s 22bp plunge for the week and “suggesting an attractive entry point for tax-free investors based on longer maturity relative value indicators such as muni-to-treasury ratios.” They added that at 78.4% and 94.5%, respectively, the 10-year and 30-year M/T ratios are the highest in four weeks.

While prices tick higher on U.S. government debt, investors have also been enjoying a fairly steady rise in MUB and VTEB. The ETFs were up 0.31% and 0.22% to US$114.24 and US$53.60, respectively, intraday Monday.

(Click on image to enlarge)

MUB and VTEB have soared more than 9.30% and 9.37%, respectively since their latest 52-week lows set in early November 2018, according to the IBKR Trader Workstation.

Against this backdrop, new muni paper will likely continue printing, with the Bloomberg 30-day visible supply having recently surged to nearly US$17bn – a new 52-week peak.

Comments

Log in or sign up to join the conversation.