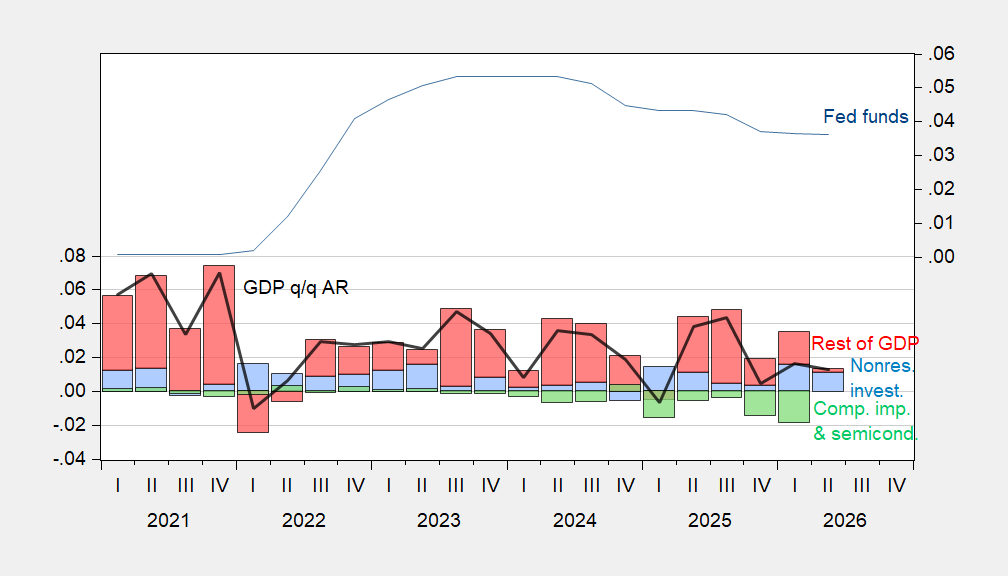

One of the mysteries of recent macro history is why tightening monetary policy failed to significantly slow economic activity, particularly capital investment. For instance, even as the Fed funds rate rose, nonresidential fixed investment rose throughout 2022-23.

FIgure 1: GDP growth, q/q AR (black line, left scale), contribution from nonresidential fixed investment (blue bar), from imports of computer, computer accessories, semiconductors (green bar), rest-of-GDP (red bar), Fed funds rate (blue line, right scale). 2026Q2 growth rates from Atlanta Fed GDPNow of 7/10; computer imports for 2026Q2 estimated off of 2 months of trade data. Source: BEA, Federal Reserve, Atlanta Fed, and author’s calculations.

This outcome — attributed to the boom in AI-related capex — has spurred the commonplace description of the US economy as being remarkably resilient. The question is whether this capex boom will continue, and by extension, the growth in the US economy.

For recent quarters, the contribution to growth emanating from nonresidential investment has been offset by imports of computer and semiconductor imports — in an accounting sense. In 2026Q2, it looks like a sizable chunk of GDP growth is accounted for by nonresidential fixed investment, which is not offset by imports, although this is contingent on 2 months of import data accurately representing Q2 overall imports. That means continued US growth is highly dependent on what happens with AI related capex.

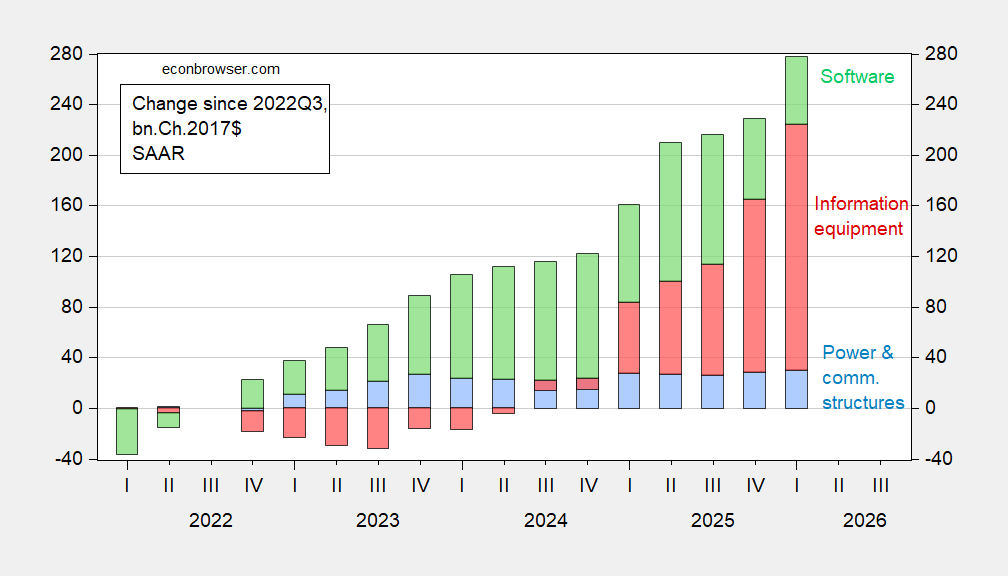

What has the composition of nonresidential fixed investment in AI looked like over the past few years. We don’t have a direct apportionment of investment to AI, but we can look at the change in investment since 2022Q3 (taking the November 2022 release of ChatGPT as a kind of marker for AI capex).

Figure 2: Change in investment in software (green bar), in information equipment (red bar), and power and communication structures (blue bar) since 2022Q3, in bn.Ch.2017$ SAAR. Source: BEA and author’s calculations.

BIS estimates 2026 investment by US hyperscalers and other AI firms at $800 bn, up from about $750 bn in 2025.

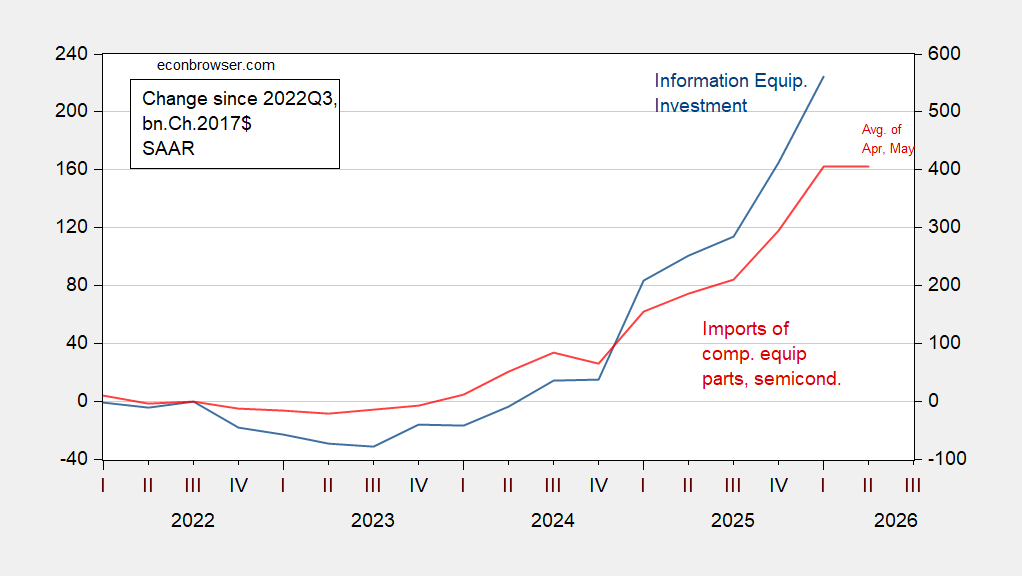

Is there any reason to believe that this level of investment won’t be reached? One leading indicator of nonresidential investment in the 2000 dot-com peak was imports of telecom and computing equipment (peak in latter was one quarter before peak in former). We only have data on information equipment investment through 2026Q1, while we have monthly data on imports of computers, computer accessories and semiconductors through May. Splicing series together, one obtains the following picture.

Figure 3: Change in investment in information equipment (blue line), imports of computer equipment, parts and semiconductors (red line) since 2022Q3, in bn.Ch.2017$ SAAR. 2026Q2 observation is based on April and May import data. Source: BEA and author’s calculations.

The 2026Q2 observation is just a guess, based on two months of data, which will be revised over time. It may very well be the case that imports continue to rise through Q2. However, there is reason to believe that there may be a downside surprise to AI-related capex.

First, Magnificent 7 stock prices have come down, and are below peak. As the equity market cools, there are (at least) two effects. First, the cost of capital will rise for AI related firms (as well as others). Second, wealth effects supporting consumption will dissipate. For AI capex should slow relative to what would have otherwise occurred.

Source: Bloomberg.

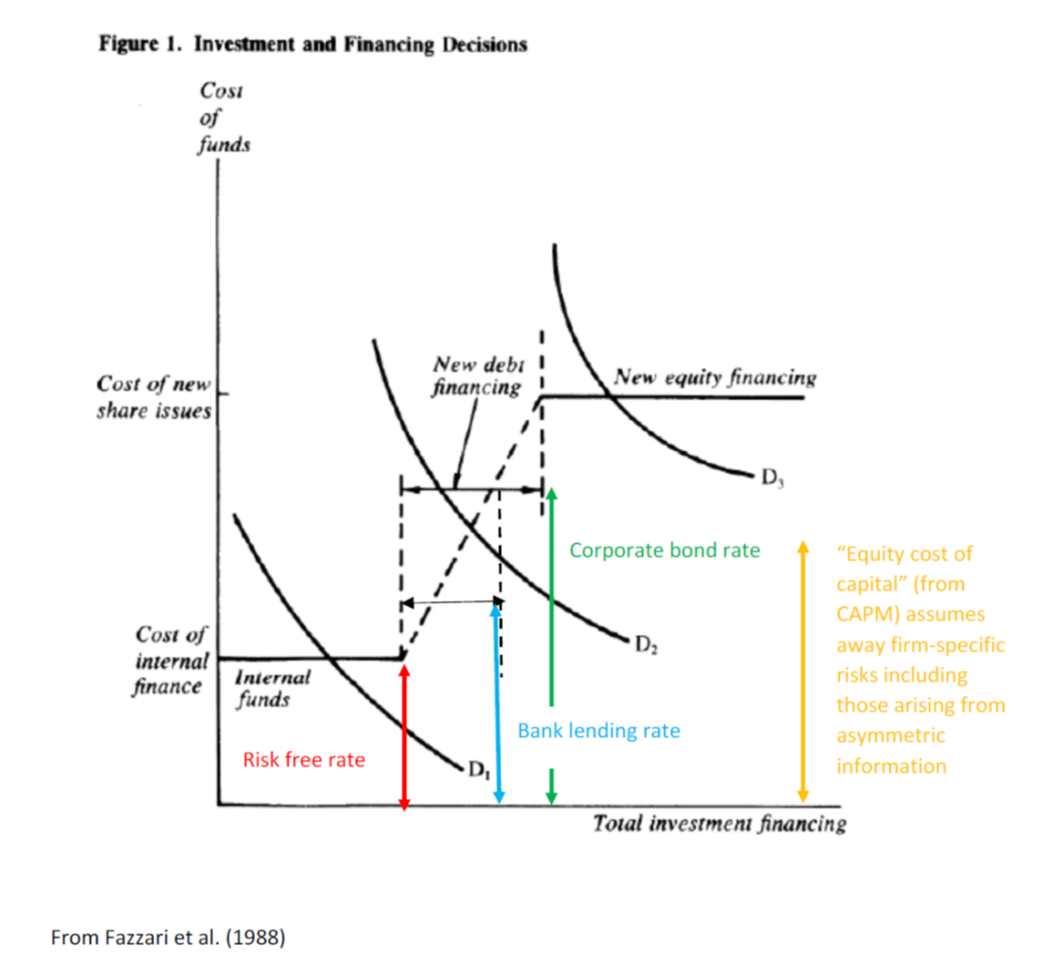

Second, investment is now outstripping cash flow, so that firms now have to rely upon external financing, i.e., through the bond markets.

Source: Economist.

The hyperscalers are hence moving up the finance pecking order. Internal funds (cash flow) was relatively cheap, and less influenced by market rates. Notice that as the corporate bond rate goes up, now investment will decline (as shown in Figure 1 below).

Source: Fazzari et al. (1988) as modified by Chinn.

Accessing bond markets mean that investment will now be subject to a higher hurdle rate, more closely tied to bond yields — and at the same time some firms will have to pay a noticeable risk premium. (Below, Microsoft (MSFT) bond yields serve as risk free rate).

Source: Economist.

Hence, while AI-related capex seemed relatively immune to higher interest rates in the past, this may be less true going forward. And indeed uncertainty regarding future expected cash flow may weigh more heavily on investment than in the past. All the more reason to reduce policy uncertainty, and reduce upward pressures on interest rates emanating from cost-push inflation.

Comments

Log in or sign up to join the conversation.