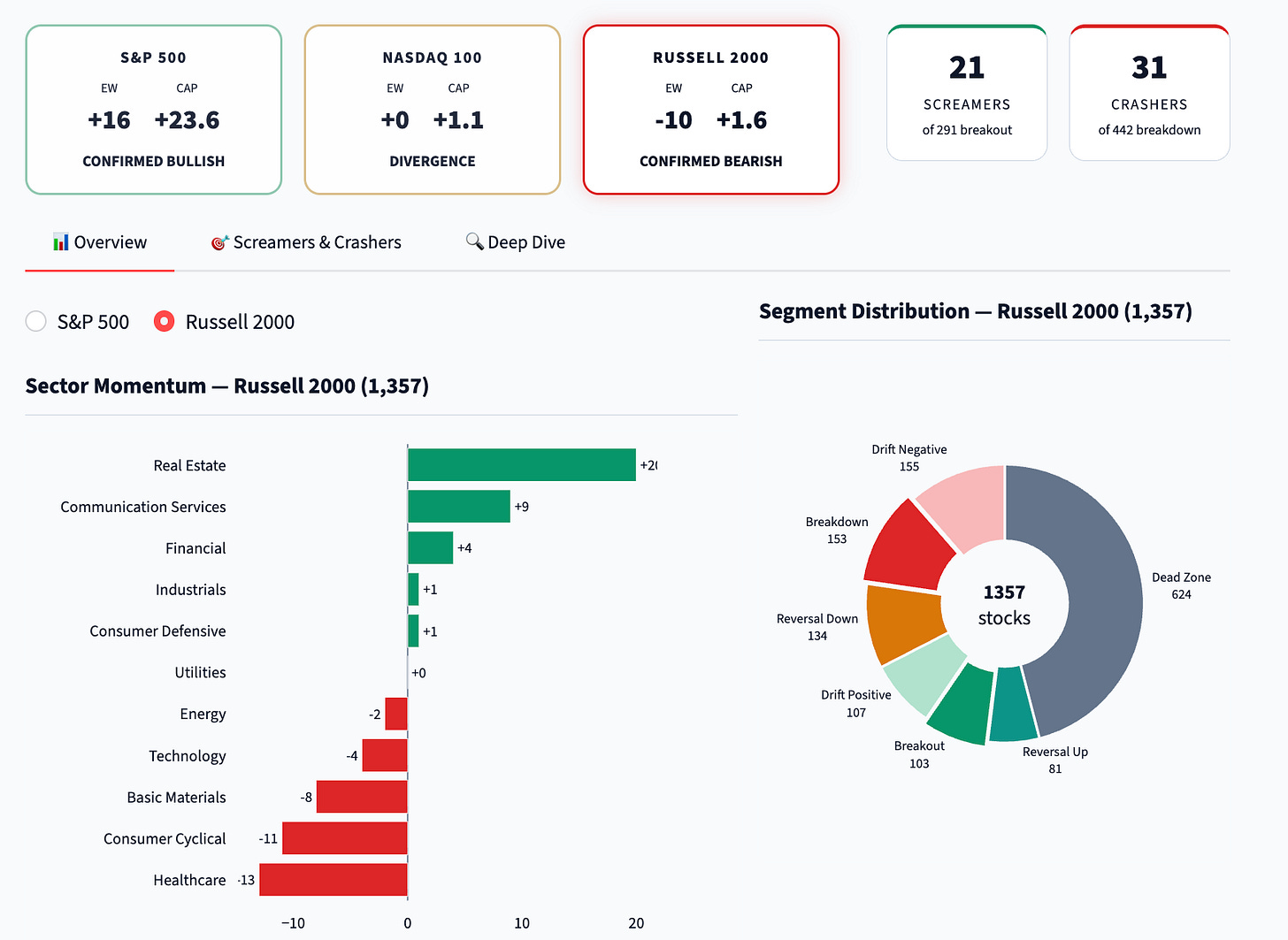

Well, we spent a week on the leverage side warning about the extreme positioning.

The Russell 2000 reading went negative yesterday morning only to lead us to a squeeze yesterday and an ensuing dump today…

Then… it just gave out today… in a pretty standard “risk off” selling event… It’s VERY comparable to the leverage that unwound after a Yellow reading on January 26. Two days later, the reading went red… and then gold and silver prices cratered as leverage unwound in those positions...

Today, the leverage is coming out of semi and AI trade…

The pressure right now on the Russell is clean in four sectors… Consumer cyclicals, healthcare (biotech especially), basic materials (miners), and technology. That tech IS the problem - as I warned about the start of selling on the IGV and software names this week after the squeeze.

Ark Innovation (ARKK) is down 7.8% today…

Which is a reminder… when this signal flips on the Russell… it’s time to buy Tradr 1X Short Innovation Daily ETF (SARK). It popped 7.8% today…

My prefered hedge Direxion Daily Small Cap Bear 3X ETF (TZA) popped 10.8%, and the $4 call for next Friday has run from $0.43 to $0.68… The trade I like that will buy a box of baseball cards…

Now… the media is blaming the jobs report…

I’m not really even sure that this jobs report was all that great in terms of the economy looking healthy. And we explained this week how so much of the actual lending in this economy is going to… other lenders… who are lending through alternative structures.

Mom and Pop aren’t getting the money…

All the while, it was a strange report in that about 50,000 of the new jobs came from the government, with a heavy lean toward local governments. And the new jobs were largely linked to hospitality - which could be seasonal… but also represents stickiness in the inflation side of services. We already knew that hiring was weak yesterday…

I’m a firm believer in looking for where the narratives shift…

How we suddenly have a qualitative shift to justify a clear quantitative environment that was out of buyers. The Direxion Daily S&P 500 Bull 3X ETF (SPXL) was crushed today… taking about a 30% hit, all while we’d warned about the leverage and the crowded nature of this trade when we started the week.

MicroSectors FANG+ Index -3X Inverse Leveraged ETNs (FNGD), which surged a stunning 15% as the tech sector now faces real pressure. The question now is whether the mechanical buying that dominated the last few weeks now has to turn to mechnanical selling - and what sort of media narrative we’ll tell if it does.

This was… the very “Risk off” type of selling that has occurred at extremes like in mid-2022… and in mid-August 2024… and right in that January window.

I think we’re only going to see more of these extremes based on the Every Buyer Thesis that I have… It all unwinds at once…

People are calling this selling healthy… I’m calling it what it is…

An unwind of max-level leverage that revealed itself earlier this week (Tuesday and Wednesday over at our paid letter.) In addition, the narrative is also shifting to rates.

I went through all of the implications around interest rates earlier today on YouTube.

Now, let’s get to the other things that are on my mind…

Thing I Think No. 2: Solomon’s Greed Bit

This week, at the Economic Club of New York, Goldman Sachs (GS) CEO David Solomon stood at a podium… He then told a room full of older men in slightly fitted blazers that greed has overwhelmed fear in financial markets…

He suggested that liquidity is ample, and that the system is ready to absorb a $1 trillion wave of AI IPOs starting with OpenAI, Anthropic, and SpaceX.

He also warned that greed could reverse to fear at any moment, by which he meant at any moment that does not happen to fall during a Goldman Sachs IPO fee window.

Seems that we might have had a historic S&P 500 win streak end on cue…

That’s the kind of timing that, if it happened to a tarot reader, would be called divination.

When it happens to a Goldman partner, it is called the schedule.

If a narrative shift comes… watch how quickly people will have forgotten about this rally. There is clear stress building in the system… and it tends to start at the Russell 2000 and Bitcoin (BTC.X) levels.

For now, we’ll see if we hit oversold and get a little bit of a bounce… remember markets don’t tend to go straight down over a series of days until the 1% pattern emerges and funds sell back into whatever strength markets can manufacture.

Thing I Think No. 3: The SpaceX Math Makes No Sense

Morgan Stanley (MS) sent a deck to its top investors this morning projecting SpaceX revenue of $3.4 trillion in 2040, with EBITDA of $2.7 trillion at an 80% operating margin.

Well, those numbers are insane… And they haven’t existed at any company at any point in commercial history.

Somehow, that math actually got through review on a Microsoft Excel file… after I assume some junior analyst ran out of conservative assumptions and just typed in what his managing director told him to type.

A guy named Brandon Carl, who has both a calculator and a few hours, ran the implied math and concluded that the Morgan Stanley projection requires the entire US economy to grow…

Seriously…

It would have to grow at 14% per year for 14 years in a row…

That figure is about double the long-run rate and requires a level of growth that would require either fusion, a lottery jackpot of biblical proportions, or a sustained collective hallucination.

The bankers have not retracted the deck.

The IPO is oversubscribed.

Thing I Think No. 4: The Twenty-One Banks on the Roster

There are 21 banks on the SpaceX underwriting syndicate.

There are also at least 21 New York Yankees on the active baseball roster at any given time.

The Yankees have a bench, which is where you sit when you are not contributing meaningfully to the inning at hand.

The 21 banks on the SpaceX deal also have a position called the bench, which is where 19 of them are sitting while Goldman and Morgan Stanley are eating the lead underwriter fees up at the plate.

The other 19 will list this deal in their year-end pitch decks as proof of capability, and the capability they are proving is the capability to be in the room when the room is doing the deal, which mainly requires sitting through an enormous number of meetings without anyone asking your opinion.

The compensation for that is, surprisingly, excellent.

Comments

Log in or sign up to join the conversation.