The COVID-19 virus continues to distort much of economic behavior that it is no wonder economists have been debating the nature of today’s inflation. Central bankers believe that surge in prices is ‘transitory’, although their patience is wearing thin. Many Wall St. analysts warn that inflation is here to stay for the long term and that central banks must act soon. The frustration with characterizing the state of the economy is best expressed in an NYT article, (Nobody knows how the economy works) So, why is it so hard to read the state of the economy right now? Why are we so unsure about the nature of inflation?

To begin, economists have long maintained that inflation is a general increase in the cost of living. A sudden large price increase in a commodity, for example, cannot be considered as inflation, but simply a spike in its price. We are witnessing this type of spike in oil and natural gas prices, but not a sustained increase in energy costs. Important as energy is to our daily well-being, this spike cannot be construed to mean that the general price level is on an upward slope. The difference between general and specific price changes is necessary to our understanding, especially in the current and very strange environment. Nonetheless, there has been a general increase in the CPI, currently about 200 pbs above the 2% target set by the central bankers. Hence, the calls from some quarters that central bankers are behind the curve and need to act decisively.

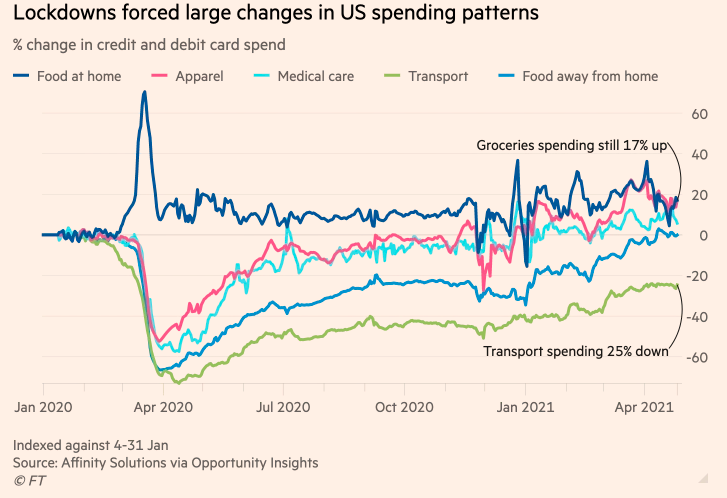

Even within the general price index, there have been fundamental changes to spending patterns arising from the pandemic effects on consumer behavior. A recent article by FT( virus distorts inflation measures) points out that price index numbers assume that expenditure patterns on food, clothing, housing, travel, entertainment, etc. have not changed over time. Official US data continues to use weightings that existed prior to the onset of the pandemic. However, the pandemic invalidates those assumed weightings when spending came to an abrupt halt for restaurants, bars, air travel, entertainment venues, etc. Most notably, grocery sales soared and public and private transportation spending slumped badly. Now the pendulum has swung in the other direction as economies resume normal consumption patterns, making it even more difficult to measure price changes over time.

Finally, it is customary to measure prices year-over-year. However, the extraordinary collapse in the price level during the depths of the 2020 lockdowns results in a huge increase in 2021 price readings--- the so-called base effect. Looking at the price level month-over-month, inflation has been slowing down since the spring. So, on balance, we are left with less than satisfactory ways to measure price changes because of the shortcomings of our measurement techniques. If anything, we need to proceed with considerable caution when debating the need for tighter monetary policy in response to the official inflation numbers. For the moment, inflation is in the eye beholder, and that should be a warning not to jump to the conclusion that something must be done.

Comments

Log in or sign up to join the conversation.