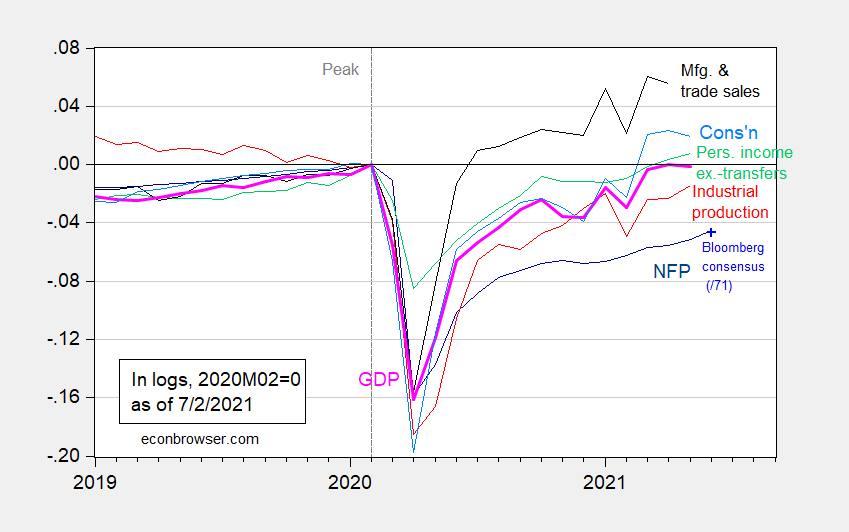

850K was the headline NFP number today. Just a reminder that, while a surprise on the upside (150K over Bloomberg consensus of just yesterday), employment is still down 4.4% relative to the NBER peak.

Figure 1: Nonfarm payroll employment from June release (dark blue), Bloomberg consensus as of 7/1 for June nonfarm payroll employment (light blue +), industrial production (red), personal income excluding transfers in Ch.2012$ (green), manufacturing and trade sales in Ch.2012$ (black), consumption in Ch.2012$ (light blue), and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (7/1/2021 release), NBER, and author’s calculations.

CEA discusses how to interpret these highly volatile employment numbers in such turbulent times, in a blog post from a few days ago.

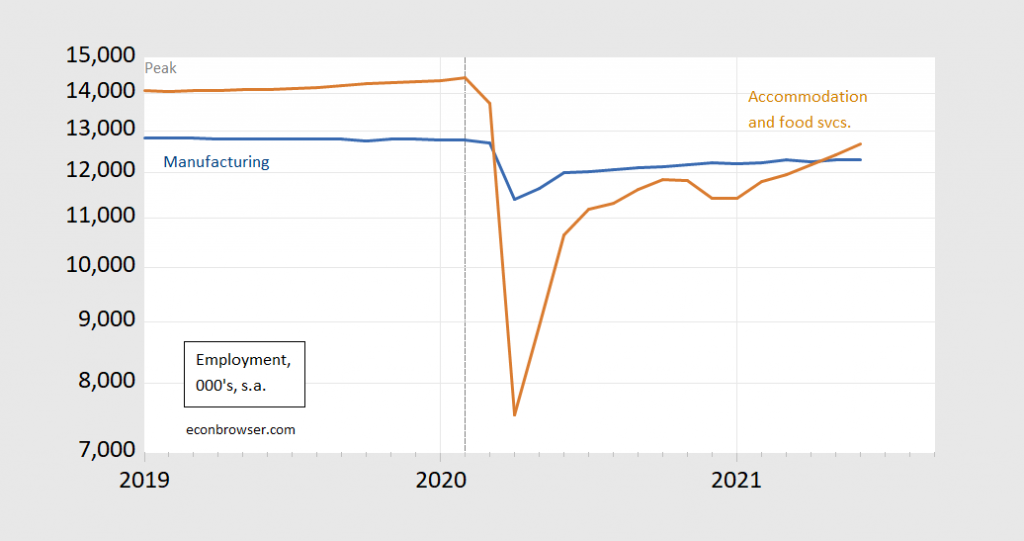

What is true is that the bifurcated nature of the labor market recovery is diminishing, albeit slowly.

Figure 2: Employment in manufacturing (blue), and in accommodation and food services (brown), both in thousands, s.a. Source: BLS.

Jason Furman and Wilson Powell discuss the messages from the employment situation from the release.

Comments

Log in or sign up to join the conversation.