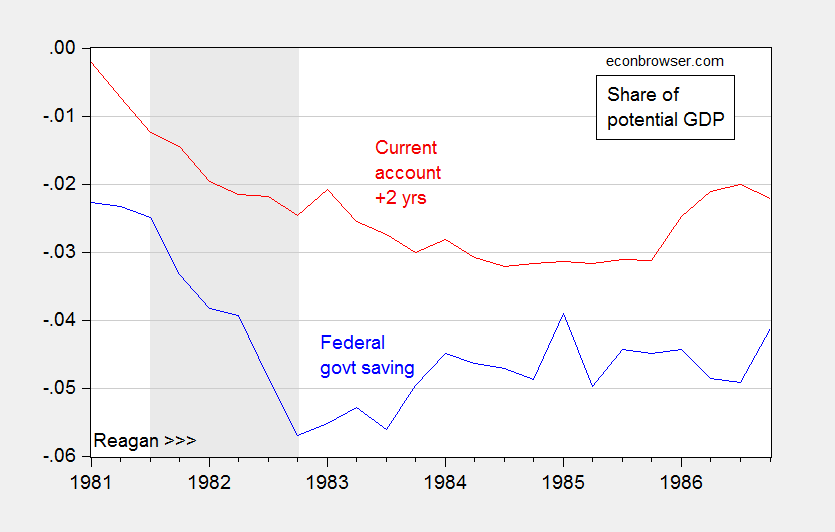

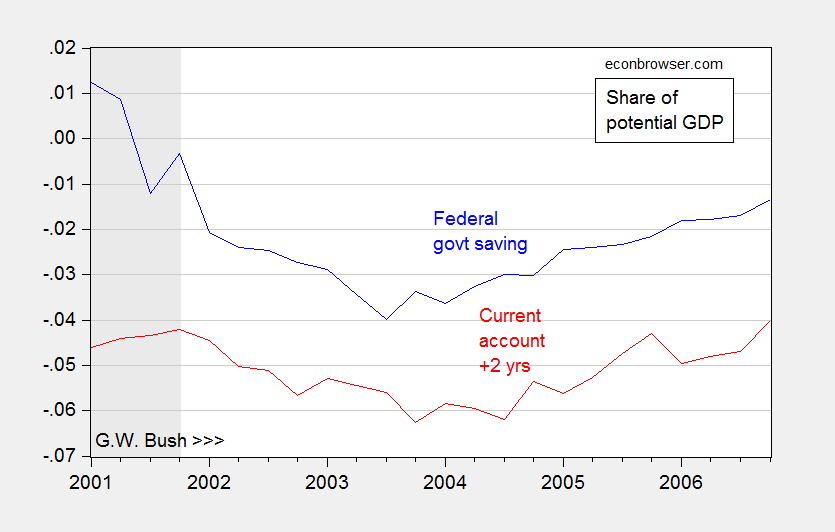

We have had previous experience with episodes of tax cuts unmatched by spending reductions, in terms of the impact on external balances. Below I plot the evolution of the Reagan twin deficits, and the evolution of the G.W. Bush twin deficits.

Figure 1: Federal government net saving (blue), and current account lead by two years (red), both as share of potential GDP. NBER recression dates shaded gray. Source: BEA, 2016Q3 3rd release, and CBO (August 2016), NBER, and author’s calculations.

Figure 2: Federal government net saving (blue), and current account lead by two years (red), both as share of potential GDP. NBER recression dates shaded gray. Source: BEA, 2016Q3 3rd release, and CBO (August 2016), NBER, and author’s calculations.

I cite empirical evidence and channels in my 2005 Council on Foreign Relations report. Greater fiscal stimulus increases absorption, pulling in imports. Deficits push up interest rates, especially combined with a Taylor rule, appreciating the dollar (see this post).

Astute readers will note that both episodes are roughly aligned with the beginning of Republican administrations: Reagan and G.W. Bush. I’m guessing the protectionist/fiscally expansionary/financial-deregulatory regime coming in with the Trump administration is likely to be in the same mold — leaving a mess for the succeeding administration to fix.

Bottom line: the way fiscal policy is likely to unfold, the current account balance (mainly accounted for by the trade balance) is likely to deteriorate, not improve. Tariffs, quotas and other restrictions — especially in an era of vertical specialization — are unlikely to offset the deterioration in the trade balance arising from absorption and dollar effects.

Comments

Log in or sign up to join the conversation.