Earlier this year, the Federal Reserve dropped its fed funds rate to near zero, opening up the possibility that the rate will fall further into negative territory. Although the Fed has resisted any temptation to go negative, European and Japanese bank rates have been below zero for several years and the indications are that they will remain so indefinitely. Both central banks realize that extreme measures are required to re-kindle growth after the 2008 crisis and now, evermore so, as the world struggles with the COVID-19 pandemic.

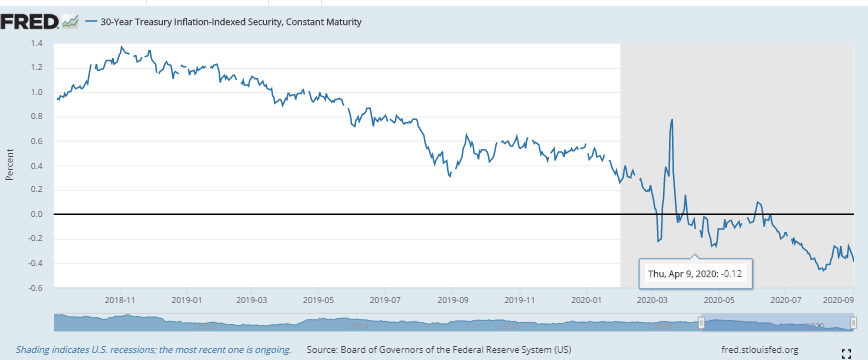

Central banks control nominal rates, the actual rate charged to the borrower, however it is real rates that ultimately affect investment and consumption decisions. Real rates, calculated as nominal rates minus the expected rate of inflation, reveal much about the health of an economy and its future growth path. Now that we are experiencing the damage from the lockdowns for most of 2020, central bankers are searching for ways to revitalize their respective economies and they have implicitly adopted a policy of maintaining negative real rates. Long term interest rates which have the greatest influence on business investment decisions have totally collapsed from a positive rate of 1.4% in 2018 to minus 0.4%.

(Click on image to enlarge)

This dramatic decline in real rates signals that investment spending will be anemic and reflect similar conditions for overall growth. However, as we emerge from the grip of the pandemic, the bond market indicates that future growth will be considerably below recent historical experience. There is a ‘deflationary gap’ which is a measure of the degree of unutilized resources. Overall, aggregate demand is insufficient to drive a robust economic recovery.

While the Fed has the most influence over short-term rates (3 years and under), the long end of the bond market is purely driven by investors’ outlook for growth and inflation years into the future. These rates are largely independent of central bank rate settings. Put differently, in the absence of a central bank authority, long term real rates would be negative as they today.

Many investors argue that negative real rates spell a great opportunity to invest by taking advantage of “cheap” money. However, the fact that money is so “cheap” is a sign that the economic outlook remains poor. The commercial banks may offer low borrowing costs but the important issue is whether they will lend at those rates. The great economist, Milton Friedman, warned that low rates of interest are not desirable because they indicate the difficulty in credit creation and ultimately in spurring economic expansion. Negative real rates are an example of the adage “be careful for wish for” since they map a future of underperformance.

Comments

Log in or sign up to join the conversation.