Amid the ongoing global trade war since January 2018, several sectors have been facing severe volatility, including various tech companies. However, throughout this turbulence, the MVP group of stocks: MasterCard, Visa and PayPal, have delivered relatively stable returns. The three FinTech companies are all benefiting from the secular growth trends in the electronic/ digital payments space, and offer great growth potential going forward.

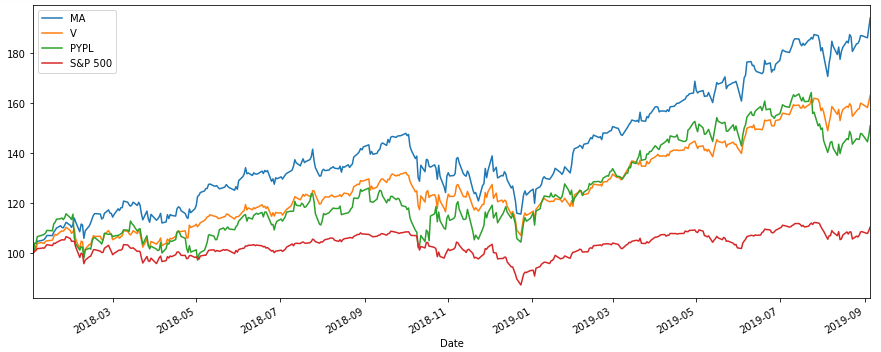

The chart below compares the performance of the MVP stocks and the S&P 500 since January 2018 (beginning of trade tensions).

(Click on image to enlarge)

The MVP stocks have clearly strongly outperformed the S&P 500 over the past 20 months. Moreover, MasterCard is evidently the strongest performer out of the group, while Visa and PayPal have for the most part been performing in tandem.

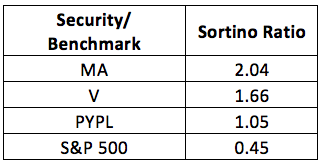

While MVP performance has indeed been stellar, they certainly were not immune to the market volatility witnessed in Q4 2018, and hence we must also assess the risk-adjusted performances of the stocks. In the table below, the Sortino ratios (for the period since Jan 2018) allow us to determine which securities offer the best returns relative to the level of downside volatility risks they pose.

MasterCard indeed offers the best risk-adjusted performance out of all three stocks. Moreover, while Visa and PayPal have mostly been performing in tandem, evidently Visa offers better risk-adjusted performance relative to PayPal.

Growth Drivers & Strategies

In order to better understand the growth prospects of each MVP stock going forward, we must also look into the companies’ strengths, challenges and strategies. Each of these FinTech giants operate with a platform business model benefiting from ‘Network Effects’, whereby the more consumers use electronic/digital payment-methods, the more willing merchants become to accept such payment solutions, and vice versa.

The two credit card companies are quite alike when it comes to generating income, and their revenue sources mainly comprise of Services revenue (dependent on payment volumes), Data Processing revenue (dependent on transactions volume) and International Transactions revenue (dependent on cross-border payments activity). The two companies have been around for several decades (even before the Internet), and both run well established global payments networks. They primarily started off as offering electronic payment methods as an alternative to cash/cheques. Amid the emergence of the Internet and the digital age, their services have evolved towards providing digital payments methods. The two tech giants are benefiting from secular growth trends as the importance of cash declines amid increased government crackdown on income tax-evasion and rising convenience of electronic/ digital payment methods. Furthermore, the rise in e-commerce and growing popularity of mobile-payment methods are also driving growth at Visa and MasterCard, as many digital wallets (e.g. Apple Pay, Samsung Pay, Google Pay) are dependent upon their enormous networks.

While the two companies employ several growth strategies such as providing value-added services (e.g. data analytics insights) and offering discounts to merchants to encourage payment method acceptance, their main strategy involves building new partnerships with financial and non-financial companies to encourage more widespread utilization of their services. For instance, Visa has recently announced a new partnership with Paytm; India’s largest mobile-payments provider, which positions it well to exploit the high-growth digital payments market in India. On the other hand, MasterCard has announced new partnerships with India’s Zoho (a cloud solution provider for SMEs) and also with Google and Amazon to incorporate the payment provider’s services into voice assistants. In terms of the global payments market, Visa has about a 61.5% market share, while MasterCard has about 25%. Hence, Visa still holds a significant lead, though MasterCard has been growing faster.

The greatest risk these card companies face is disintermediation risk, whereby their customers/ competitors find ways of replacing their payments networks with other means of fund transfers. Though it is important to acknowledge just how big of a moat these companies hold, as their respective global payments networks have been built over decades, hence making it very difficult to replicate, which is the reason why many new payment solution innovations, such as Square and Apple Pay, remain dependent on the well-established networks of Visa and MasterCard. That being said, the rise of crypto-currencies certainly challenges the services provided by the two giants, as they allow for both domestic and international fund transfers without the need for the credit card networks. However, in a previous article I had discussed the risks associated with crypto-currencies, including regulatory hurdles and susceptibility to fraudulent activity. While crypto-currencies offer an alternative method of payment, they are certainly not perfect, as payments are slow and not as safe as some like to portray.

Hence the card companies still hold significant strengths over crypto-currencies in vital aspects of payments solutions. For example, Visa’s network and infrastructure allows it to process 3000 transactions per second, whereas Bitcoin can only process 7 transactions per second, while Ethereum can process 15 per second. Amid these existing flaws/short-comings, the card companies are investing heavily in adopting and improving blockchain technology (which underpins crypto-currencies) to not only fend-off disintermediation risk, but to incorporate this new technology in order to be able to offer even more superior payment solution services. This is particularly true for MasterCard, which is in the lead in the blockchain race with 30 blockchain-related patents filed. MasterCard’s blockchain efforts are currently focused on enhancing the safety and security of their payment solutions, while Visa’s efforts are targeted towards offering enhanced payments solutions in the B2B payments market. Keep in mind that these card companies are already highly regulated and possess well-established infrastructure to ensure their payment solutions offer optimum safety and security. On the other hand, crypto-currencies face inevitable global regulatory uncertainty amid fraudulent-activity risks. Therefore, the threat of crypto-currencies replacing the card networks now or in the near future is minimal. In fact, it is interesting to note that in India, dealing with crypto-currencies is illegal. India is a high-growth market in terms of digital payment solutions as ore and more people gain access to the Internet, and is a nation that many multinationals are turning to for future growth. Hence, given that the MVP group is able to legally operate and grow in the high-growth market while crypto-currencies remain illegal undermines the disintermediation risk posed by the new digital currencies.

Therefore, Visa and MasterCard are likely to remain the market leaders for the foreseeable future as they incorporate blockchain into their services and continue benefiting from the secular growth trends in electronic/ digital commerce.

PayPal (PYPL)

PayPal is a FinTech company that offers digital money management, transfer and online payment capabilities, and runs a well-established digital payments network. PayPal greatly benefits from the secular trends towards e-commerce, as its services as a website payment gateway solution allow businesses to accept payments online. In fact, it is a market leader in the website payment gateway market, with a 61.44% market share. It is worth noting that PayPal has also partnered with Visa and MasterCard, whereby it offers these two payment methods as part of its payment gateway solution to enhance its services and network reach, which actually further evidences the strength of the card networks discussed earlier.

Apart from offering online payment gateway solutions, PayPal also runs popular mobile wallet app Venmo, which the company is currently trying to monetize so that it one day becomes profitable. PayPal’s prominent growth strategy also involves partnerships with both financial and non-financial companies. In fact, PayPal currently has partnerships with notable growing platform businesses such as Uber and Facebook (Marketplace); encouraging consumers of these businesses to use payment services provided by PayPal and thereby growing its transactions and payments volumes. While competition in this space is certainly rising from firms such as Shopify, Stripe and Square, PayPal holds a considerable market lead and unlike most of its competitors it is a profitable company with strong Free Cash Flow, allowing it to continually invest in its technology to enhance its services and stay ahead of competition. Furthermore, like Visa and MasterCard, PayPal is also making moves to fend-off disintermediation risk from the rise of crypto-currencies, and has actually filed for patents, including one where it seeks to use blockchain technology to enhance the speed of transactions (a shortcoming of current digital currencies), and another where it seeks to fight against crypto ransom ware to improve the safety and security of its payment solutions.

Therefore, PayPal is a stock that benefits from various secular growth trends including e-commerce, mobile payments and strategic partnerships with other high-growth companies that are also benefiting from specific secular growth trends, making it another attractive long-term investment choice.

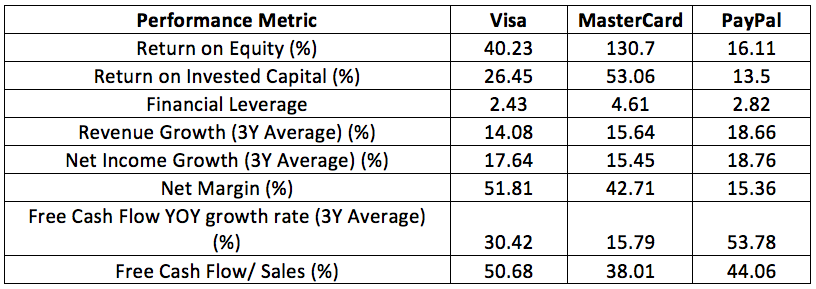

Financial Performance

Data Source: Morningstar

Out of the three stocks, MasterCard offers the best Return on Equity (ROE) at 130.7%, considerably higher than both Visa (40.23%) and PayPal (16.11%), though it also has almost double the financial leverage compared to the other two firms, at 4.61. Higher leverage helps boosts ROE as total equity becomes a smaller portion of the firm’s total capital used to drive growth. Hence, we must also assess its Return on Invested Capital (ROIC) to gain a better sense of investment efficiency. ROIC for MasterCard is at 53.06%, which is also significantly higher than those of Visa (26.45%) and PayPal (13.5%). Therefore, out of MVP, MasterCard evidently uses its capital most efficiently to produce returns for investors, which explains why the stock has so strongly outperformed the other two FinTech giants, as we found earlier.

With regards to revenue and net profit growth, PayPal has witnessed the strongest growth over the last three years. Nevertheless, the two card companies hold significantly higher net profit margins, with Visa at 51.81% and MasterCard at 42.71%, which are notably higher than PayPal’s 15.36% margin. That being said, PayPal holds the strongest Free Cash Flow (FCF) position with a 3-year average growth rate of 53% and FCF making up 44.06% as a portion of total sales revenue, allowing it to effectively allocate financial resources towards more innovation and fending off competition in this highly competitive and constantly evolving industry. As a matter of fact, all three stocks enjoy strong FCF, putting them in strong financial positions to compete with any newcomers.

Risks

While the three stocks have offered superior returns over the rest of the market during this period of trade war/ recession fears, it is mostly thanks to strong consumer confidence/ spending. Though the latest round of trade-tariffs are now targeting consumer goods, which could undermine this strength going forward. If this global trade war continues, it will inevitably drag the consumer down as well. Also keep in mind that consumer confidence/spending is greatly influenced by financial market conditions. Hence any deterioration in financial assets as a result of souring trade conditions/ worsening global economic conditions/ unfavorable political developments would also undermine consumer strength. Thus if consumers cut back on spending, it would lower the payments volume processed by these FinTech firms and weaken their earnings. Though it is important to note that MVP’s earnings are not completely dependent on payments volume, but that they also collect transaction fees. Even if we face a recession, consumers are still likely to continue spending on essential consumer staples, and thus the use of payment methods provided by MVP will continue to bring in transaction fee revenues, as well as a certain level of payments volume (though not as high as during a growing economy).

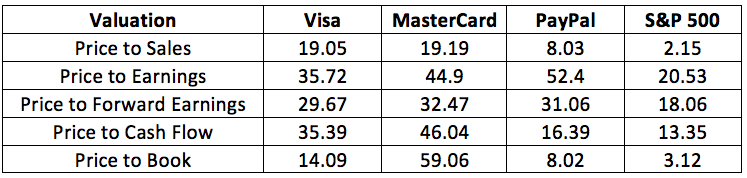

Another risk investors must take into consideration is valuation risk. The table below shows how MVP stocks are quite expensive relative to the overall market, especially MasterCard.

While all three companies are benefiting from strong secular growth trends that encourage investors to pay higher multiples for the stocks, their lofty valuations do make them more sensitive to severe economic/ market downturns. As discussed earlier, if consumers start showing signs of weakness amid a global economic slowdown/ recession, then this would negatively impact their revenues and earnings, and consequently push their stock prices lower. Therefore, while the MVP stocks certainly offer attractive long-term potential, it may be worthwhile waiting for a downturn in their stock prices amid weakening economic conditions globally.

Bottom Line

Throughout the trade war, the MVP stocks have offered appealing risk-adjusted returns, particularly MasterCard with a Sortino Ratio of 2.04. The long-term secular growth trend in the shift from cash and cheques payment methods to electronic/digital payment solutions is the common underlying growth driver for these FinTech stocks. Their strong financial positions and effective growth strategies, through building partnerships and investing in blockchain, makes the MVP group an attractive basket of stocks to hold exposure to over the long-run, though it may be worthwhile waiting for a pullback in their stock prices before allocating capital towards these securities.

Comments

Log in or sign up to join the conversation.