Canadian investors have always taken positions within the tightly-knit banking community, knowing that the Big Five banks would be sure bets for generating profits even in a challenging macroeconomic environment. This week’s release of bank earnings for fiscal 2019 reveals that banks have had, at best, a very mediocre year. More significantly, Canadian banks are not looking forward to fiscal 2020 as they set aside higher loan loss provisions, cut jobs and other expenses and maintain lending in a very slow growth environment. The banks are bracing for a very difficult year ahead.

On a quarterly basis, fiscal 4th quarter ending October 31, earnings growth was either negative (CIBC, TD, RBC) or slightly above zero (BNS). No bank enjoyed the last quarter. On a yearly basis, the best that can be said of the banks is that profit growth was largely positive but in the low single-digit range. At the same time, the economy grew faster in the first half than in the second half of the year and, yet the banks’ profitability barely met nominal economic growth. It appears that the banks are just treading water and adjusting their operations accordingly.

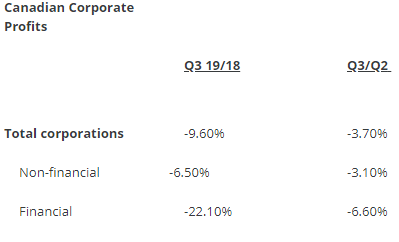

These figures are adjusted and are non-GAAP which usually indicates that a series of so-called “one-time” charges are not included. Using GAAP figures, as provided by Statistics Canada, all corporate profits fell for the 12 months ending in 2019Q3. Within the financial sector, the decline was even greater. The table below forms part of the GDP estimates and thus is more representative of corporate performance than that reported to Bay St. analysts. Clearly, all financial institutions have struggled in 2019. Euphemistically, the banks’ CEOs refer to 2020 as a “challenge”.

In supporting its position as the only central bank not to lower the bank rate, the Governor of Bank of Canada argues that the Canadian economy is “resilient” in the face of a difficult international environment. This resiliency will be put to the test in the financial sector next year and beyond. The Canadian banks have increased their loan loss provisions anywhere from 25% to 60 % compared to last year. Bankruptcies and delinquencies are expected to increase, especially in hard-hit regions like western Canada. BMO announced the biggest job cuts in 15 years and took a C$ 357 million provision for severance. The mortgage business has been negatively affected by tighter lending rules, introduced in 2017, and the banks now face tough competition from the unregulated mortgage lenders who have been able to service clients rejected by the major banks. Some banks have written down specific lines of business (e.g. insurance) and others have cited goodwill writes off associated with discontinued non-domestic operations. Finally, the banks are facing challenges from fintech competitors and are in the midst of improving their digital platforms.

Comments

Log in or sign up to join the conversation.