The good news is: The Dow Jones Industrial Average (DJIA), S&P 500 (SPX) and Nasdaq composite (OTC) all closed at all-time highs last Friday. (Same as last week)

The Negatives

Not much has changed in the past week.

The market is overbought.

Last week I wrote: The Russell 2000 (R2K) was the only one of what I consider to be the major indices that has not hit a new high recently. The R2K has been very strong for the past several weeks, but it is 1.6% off its previous highs so a new high, in the next few days, is not a sure thing.

Last week the R2K was the worst-performing of the major indices; up 0.6% and still off its previous high by 1%.

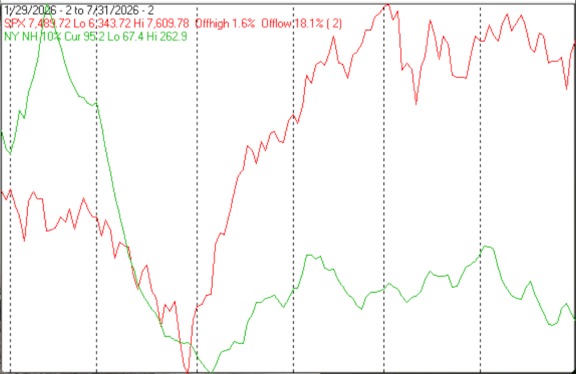

The first chart covers the past 6 months showing the SPX in red and a 10% trend (19 day EMA) of NYSE new highs (NY NH) in green. Dashed vertical lines have been drawn on the 1st trading day of each month.

NY NH faltered last week and is far from confirming the new SPX high.

The Positives

Some of the breadth indicators confirmed the new index highs implying higher highs ahead.

The next chart is similar to the first one except is shows the OTC in blue and OTC NH, in green, has been calculated with NASDAQ data.

OTC NH confirmed the OTC high implying higher highs ahead.

The next chart covers the past 6 months showing the OTC in blue and a 40% trend (4 day EMA) of NASDAQ new highs divided by new highs + new lows (OTC HL Ratio), in red. Dashed horizontal lines have been drawn at 10% levels for the indicator; the line is solid at the 50%, neutral, level.

OTC HL Ratio fell a little; finishing the week at 62%.

The next chart is similar to the one above except it shows the SPX in red and NY HL Ratio, in blue, has been calculated with NYSE data.

NY HL Ratio fell slightly finishing the week at 77%.

Seasonality

Next week includes the 5 trading days prior to the 3rd Friday of November during the 3rd year of the Presidential Cycle. The tables below show the daily change, on a percentage basis, for that period.

OTC data covers the period from 1963 to 2018 while SPX data runs from 1953 to 2018. There are summaries for both the 3rd year of the Presidential Cycle and all years combined. Prior to 1953 the Market traded 6 days a week so that data has been ignored.

Average returns for the coming week have been mixed and weaker during the 3rd year of the Presidential Cycle than other years.

Report for the week before the 3rd Friday of November.

The number following the year is the position in the Presidential Cycle.

Daily returns from Monday through 3rd Friday.

OTC Presidential Year 3 (PY3)

Year Mon Tue Wed Thur Fri Totals

1963-3 0.48% 0.17% -0.06% 0.20% -0.45% 0.34%

1967-3 0.24% -0.10% -0.25% 0.67% 1.04% 1.59%

1971-3 -0.45% 0.26% -0.07% -0.19% -0.47% -0.93%

1975-3 0.15% -0.61% -0.95% -0.26% 0.09% -1.58%

1979-3 0.88% 0.07% 0.45% 0.84% 0.11% 2.34%

1983-3 0.86% -0.21% 0.37% 0.47% 0.01% 1.49%

1987-3 -0.19% -1.74% 0.46% -1.35% -0.46% -3.27%

1991-3 0.48% 0.90% 0.09% -0.24% -4.24% -3.01%

1995-3 -0.51% -1.69% 0.12% 0.25% 0.05% -1.78%

Avg 0.30% -0.54% 0.30% 0.00% -0.91% -0.85%

1999-3 -0.05% 2.29% -0.73% 2.39% 0.66% 4.56%

2003-3 -1.07% -1.46% 0.95% -0.93% 0.64% -1.88%

2007-3 -1.67% 3.46% -1.10% -0.98% 0.72% 0.44%

2011-3 -0.80% 1.09% -1.73% -1.96% -0.60% -4.00%

2015-3 1.15% 0.03% 1.79% -0.03% 0.62% 3.55%

Avg -0.49% 1.08% -0.16% -0.30% 0.41% 0.53%

OTC summary for PY3 1963 - 2015

Avg -0.04% 0.18% -0.05% -0.08% -0.16% -0.15%

Win% 50% 57% 50% 43% 64% 50%

OTC summary for all years 1963 - 2018

Avg -0.16% 0.12% -0.08% 0.08% 0.04% 0.00%

Win% 45% 55% 55% 57% 54% 57%

SPX PY3

Year Mon Tue Wed Thur Fri Totals

1955-3 2.59% -0.43% -0.65% -0.70% -0.11% 0.70%

1959-3 -1.11% 0.28% 1.08% -0.09% 0.05% 0.22%

1963-3 0.22% -0.39% 0.08% -0.46% -0.82% -1.38%

1967-3 -0.26% -0.63% 0.40% 0.92% 0.24% 0.67%

1971-3 -0.34% 0.98% 0.15% -0.78% -0.56% -0.55%

1975-3 0.54% -0.50% -1.12% -0.38% -0.12% -1.59%

Avg -0.19% -0.05% 0.12% -0.16% -0.24% -0.52%

1979-3 1.97% -0.55% 0.44% 0.72% -0.33% 2.25%

1983-3 0.17% -0.73% 0.44% 0.03% -0.63% -0.72%

1987-3 0.46% -1.51% 1.03% -2.24% 0.81% -1.45%

1991-3 0.06% 0.92% 0.17% -0.07% -3.66% -2.58%

1995-3 -0.07% -0.51% 0.79% 0.57% 0.46% 1.24%

Avg 0.52% -0.48% 0.57% -0.20% -0.67% -0.25%

1999-3 -0.12% 1.84% -0.66% 1.01% -0.21% 1.86%

2003-3 -0.64% -0.91% 0.80% -0.84% 0.16% -1.43%

2007-3 -1.00% 2.91% -0.71% -1.32% 0.52% 0.41%

2011-3 -0.96% 0.48% -1.66% -1.68% -0.04% -3.85%

2015-3 1.49% -0.13% 1.62% -0.11% 0.38% 3.24%

Avg -0.25% 0.84% -0.12% -0.59% 0.16% 0.04%

SPX summary of PY3 1955 - 2015

Avg 0.19% 0.07% 0.14% -0.34% -0.24% -0.18%

Win% 50% 38% 69% 31% 44% 50%

SPX summary for all years 1953 - 2018

Avg -0.03% 0.01% -0.05% -0.03% 0.13% 0.03%

Win% 48% 45% 59% 52% 62% 53%

Conclusion

The conclusion is the same as last week.

The market is overbought. New blue-chip highs were not confirmed by the secondaries and some of the breadth indicators. Seasonality for the next couple of weeks has been negative.

I expect the major averages to be lower on Friday, November 15 than they were on Friday, November 8.

Last week's negative forecast was a miss.

Comments

Log in or sign up to join the conversation.