Technical market report for February 1, 2020

The good news is:

- The market had another rough week, but, since the recent all time highs were confirmed by the breadth indicators, there should be new all time highs in the next month or so.

The Negatives

The secondaries represented by the Russell 2000 (R2K) have been leading the way down.

Hindenburg omens were triggered on Monday, Thursday and Friday when NYSE new highs and new lows both exceeded 2.8% of issues traded.

The Positives

The recent highs were confirmed by breadth.

The market is oversold.

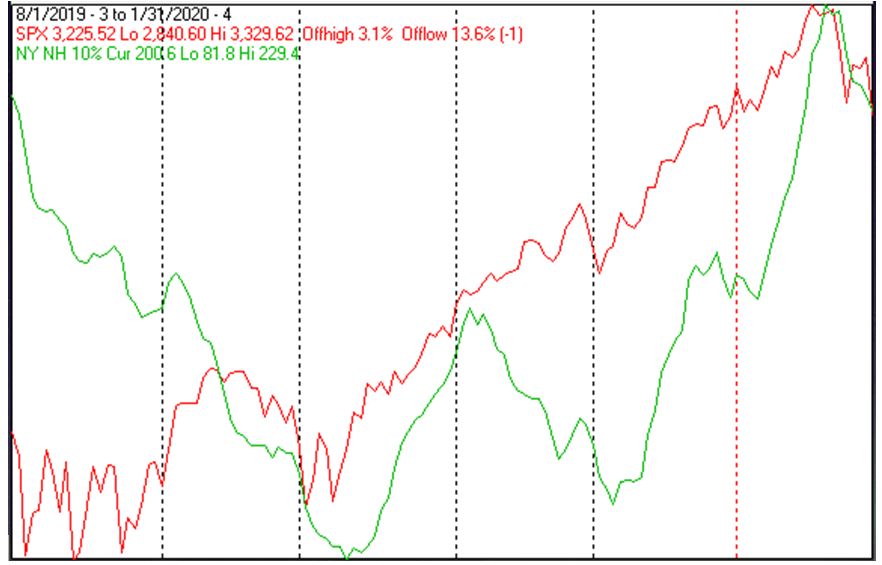

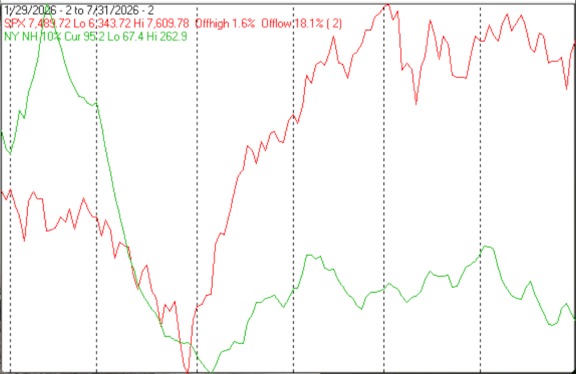

The first chart covers the past 6 months showing the S&P 500 (SPX) in red and a 10% trend (19 day EMA) of NYSE new highs (NY NH) in green.Dashed vertical lines have been drawn on the 1st trading day of each month.

NY NH hit its high a few days after the index.

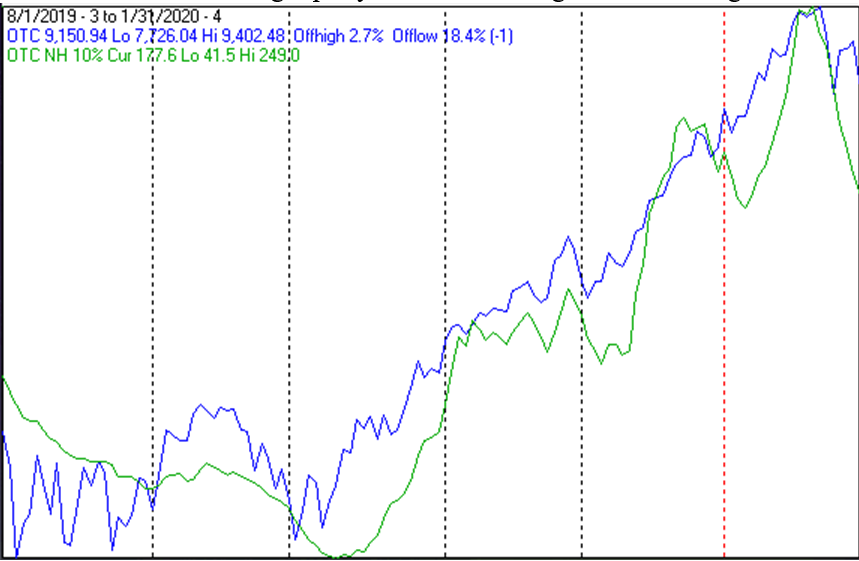

The next chart is similar to the one above except it shows the NASDAQ composite (OTC) in blue and OTC NH, in green, has been calculated with NASDAQ data.

OTC NH has been falling rapidly since confirming the all time highs last month.

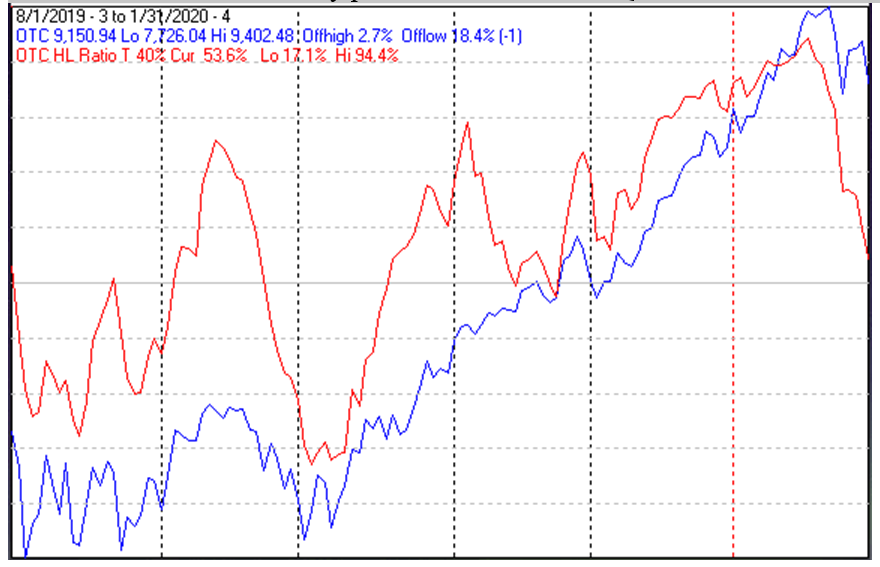

The next chart covers the past 6 months showing the OTC in blue and a 40% trend (4 day EMA) of NASDAQ new highs divided by new highs + new lows (OTC HL Ratio), in red.Dashed horizontal lines have been drawn at 10% levels for the indicator; the line is solid at the 50%, neutral, level.

OTC HL Ratio fell to a barely positive 54%.NASDAQ new lows exceeded new highs on Monday and Friday last week.

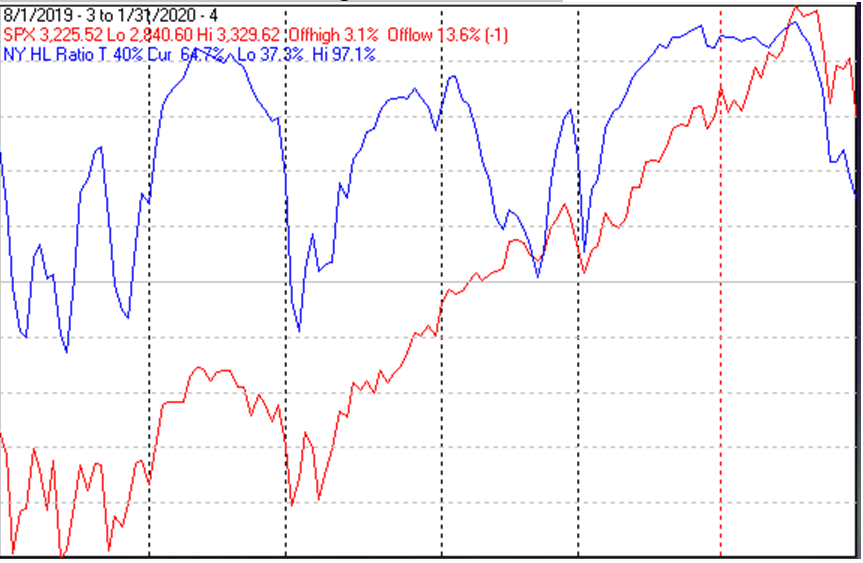

The next chart is similar to the one above except it shows the SPX in red and NY HL Ratio, in blue, has been calculated with NYSE data.

NY HL Ratio also fell finishing the week at 65%.

Seasonality

Next week includes the first 5 trading days of February during the 4th year of the Presidential Cycle. The tables below show the daily change, on a percentage basis, for that period.

OTC data covers the period from 1963 to 2018 while SPX data runs from 1928 to 2018.There are summaries for both the 4th year of the Presidential Cycle and all years combined.

Average returns for the coming week have been mixed.

February

Since 1963, over all years, the OTC in February has been up 56% of the time with an average gain of 0.7%.During the 4th year of the Presidential Cycle February has been up 57% time with an average gain of 2.2%.The best February for the OTC was 2000 (+19.2%), the worst 2001 (-22.4%).

The average month has 21 trading days.The chart below has been calculated by averaging the daily percentage change of the OTC for each of the 1st 11 trading days and each of the last 10.In months when there were more than 21 trading days some of the days in the middle were not counted.In months when there were less than 21 trading days some of the days in the middle of the month were counted twice.Dashed vertical lines have been drawn after the 1st trading day and at 5 trading day intervals after that.The line is solid on the 11th trading day, the dividing point.

In the chart below the blue line shows the average of the OTC in February over all years since 1963 while the black line shows the average during the 4th year of the Presidential Cycle over the same period.

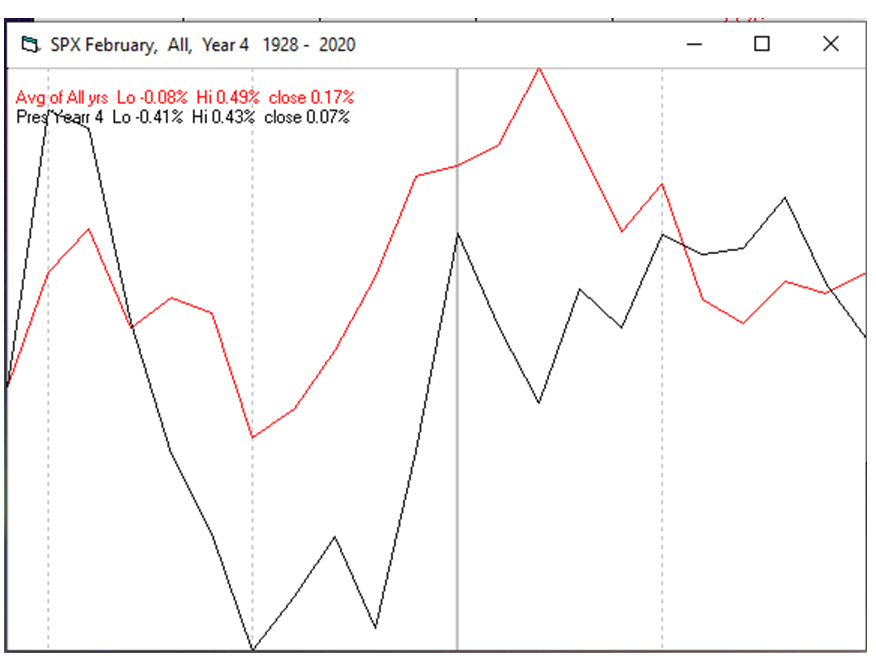

Since 1928 the SPX in February has been up 53% of the time with, on average, no gain or loss.During the 4th year of the Presidential Cycle the SPX has been up 52% of the time with an average gain of 0.1%.The best February for the SPX was 1931 (+11.4%) the worst 1933 (-18.4%).

The chart below is similar to the one above except it shows the daily average performance over all years since 1928 for the SPX in February in red and the performance during the 4th year of the Presidential Cycle in black.

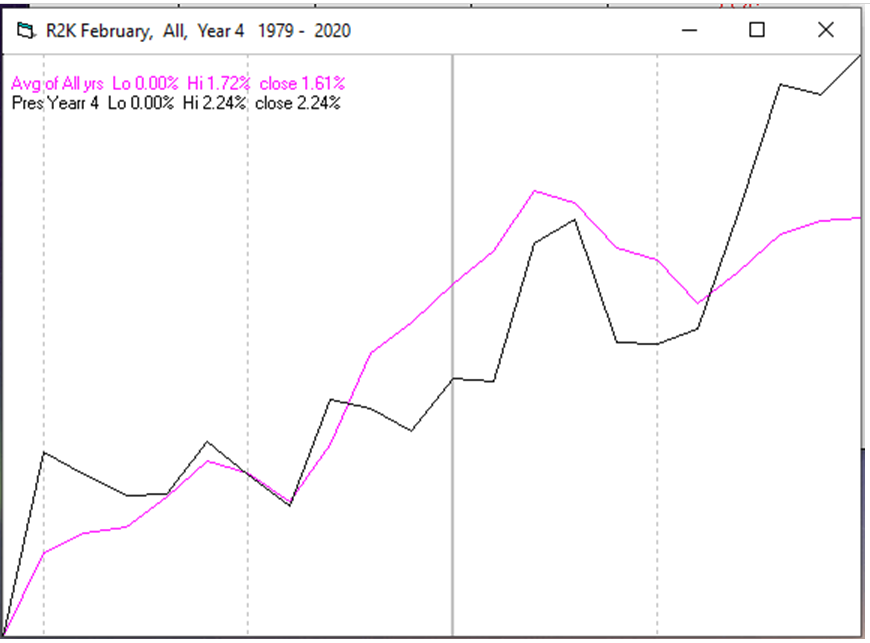

Since 1979 the Russell 2000 (R2K) has been up 59% of the time in February with an average gain of 1.2%.During the 4th year of the Presidential Cycle the R2K has been up 60% of the time with an average gain of 2.2%.The best February for the R2K 2000 (+16.4%), the worst 2009 (-12.3%)

The chart below is similar to those above except it shows the daily performance over all years since 1979 of the R2K in February in magenta and the performance during the 4th year of the Presidential Cycle in black.

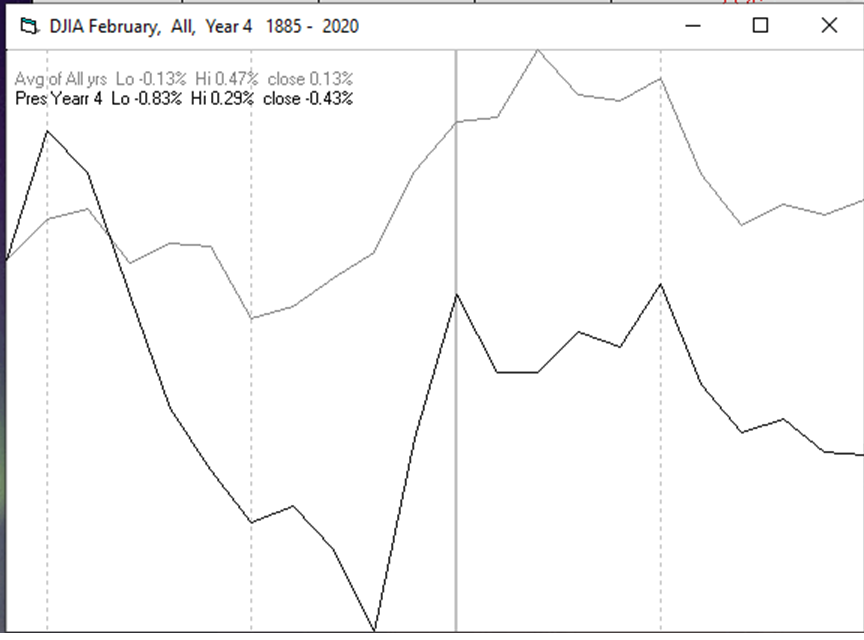

Since 1885 the Dow Jones Industrial Average (DJIA) has been up 53% of the time in February with an average loss of -0.1%.During the 4th year of the Presidential Cycle the DJIA has been up 52% of the time in February with an average loss of -0.6%.The best February for the DJIA 1931 (+13.2%), the worst 1933 (-15.6%)

The chart below is similar to those above except it shows the daily performance over all years since 1885 of the DJIA in February in light grey and the performance during the 4th year of the Presidential Cycle in black.

Conclusion

The decline of the past 2 weeks could go on for a while longer, but since the recent highs were confirmed by breadth it is very likely there will be more all time highs for the blue chip indices.

Utilities and precious metals continued as the strongest sectors while energy remained the worst performer followed by electronics and banks.

I expect the major averages to be higher on Friday, February 7 than they were on Friday, January 31.

Last weeks positive forecast was a miss.

Comments

Log in or sign up to join the conversation.