Image: Bigstock

The Q1 earnings season has come to an end for 9 of the 16 Zacks sectors, with results from 462 S&P 500, or 92.4% of the index’s membership, already out. Most of the still-to-come reports are from the Retail, Tech, and Industrial Products sectors.

Total Q1 earnings for the 462 S&P 500 companies that have already reported results are up +21.1% from the same period last year on +10.4% higher revenues, with 79.9% beating EPS estimates and 78.6% beating revenue estimates. This is a better showing from these companies relative to other recent periods.

The aggregate earnings total for Q1 is on track to be a new all-time quarterly record at $689.8 billion, surpassing the record set in the preceding quarter at $655.4 billion.

The Q1 earnings season showed continued strength and momentum, with companies not only comfortably beating consensus estimates but also providing a reassuring read on the economy despite elevated energy costs and other risks. The momentum is particularly notable on the revenues side, both in terms of the growth pace as well as the beats percentage. We are also seeing positive momentum on the revisions front, with estimates for the current and upcoming quarters rising.

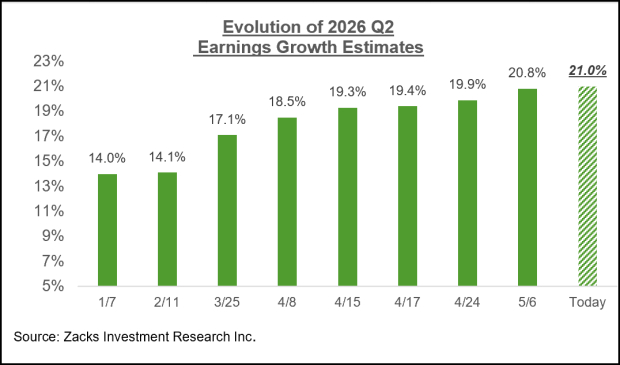

The Revisions Trend Remains Positive

The overall earnings picture continues to be of all-around strength and a steadily improving outlook. This favorable earnings backdrop is evident in the revisions trend, as seen in how expectations for 2026 Q2 have evolved in recent weeks.

Image Source: Zacks Investment Research

We should note that Q2 estimates have modestly come down in recent days, even though the overall revisions trend remains positive.

The sectors enjoying positive estimate revisions since the start of April include Energy, Tech, Basic Materials, Industrials, Utilities, and Business Services. But Q2 estimates in the aggregate would be modestly down since the start of the period had it not been for the increase in Energy and Tech sector estimates.

The Tech sector has been enjoying positive estimate revisions for more than a year now, so the sector’s positive revisions trend is basically more of the same. We have discussed in this space the positive revisions that the Mag 7 group has been experiencing. The Energy sector’s improved earnings outlook is a direct result of the Iran war, as is the upgraded earnings outlook for parts of the Basic Materials sector, particularly the Chemicals industry.

Take, for example, the evolution of Q2 EPS estimates for Dow (DOW - Free Report), LyondellBasell Industries (LYB - Free Report), Methanex (MEOH - Free Report), and others. For Dow and LyondellBasell, the Zacks Consensus EPS estimates for Q2 have more than doubled over the past month, while the same for Methanex has increased by more than 30%.

On the negative side, Q2 estimates have come under renewed pressure since the start of the period for the Transportation, Autos, Medical, and Consumer Discretionary sectors.

The chart below shows S&P 500 expectations for 2026 Q1 in terms of what was achieved in the preceding four periods and what is currently expected for the following three quarters.

Image Source: Zacks Investment Research

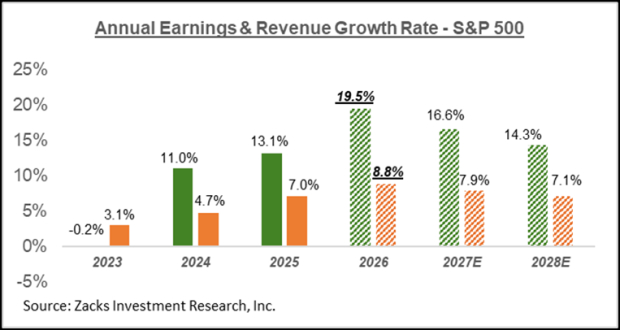

The chart below shows the overall earnings picture for the S&P 500 index on an annual basis.

Image Source: Zacks Investment Research

Comments

Log in or sign up to join the conversation.