Short term investors are hanging on every word spoken by central bankers for clues as to when bank rates will rise. Meanwhile, there are some investors who ignore the daily noise in the marketplace and are looking out 50 years or more on the yield curve. These investors have been scooping up ultra long bonds. It has become increasingly commonplace for pension funds and insurance companies to purchase 50-year bonds issued by many EU countries and a few major corporations. This week Italy issued a 50-year bond that yielded 2.85 percent, and more importantly, the issue was greatly oversubscribed. Clearly, the demand for bonds has structurally shifted further out the yield curve, thus adding a new dimension to the bond market.

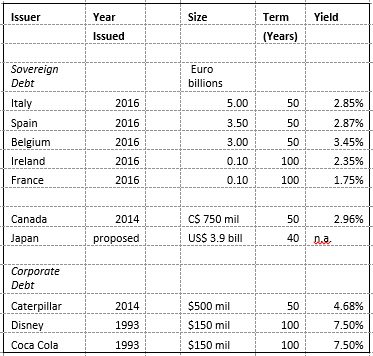

Table 1 lists ultra long bonds issued by selected sovereign and corporate entities, some even extending out to 100 years.

Table 1 Selected Issuance of Ultra Long Bonds

U.S. investors are familiar with long-dated maturities for many years as both the U.S. government and many corporations have issued 30–year bonds. However, 50-year debt is mainly a European phenomenon.

What Motivates Investors / Governments to Go Out 50 Years?

*the stretch for yield. Faced with so much of European debt market in negative territory, investors have been forced into longer-dated bonds that offer the prospect of positive returns. The further an issuer goes out along the curve, generally, the investor base gets smaller because of the higher risk associated with long-date maturities. But the ECB has been successful in moving more and more investors to the very long end.

*outlook for global economy is weak. These investors do not expect any large and sustained increase in yields as the global economy struggles with low inflation, a slowly growing and aging workforce. This will keep yield curves relatively flat.

* the importance of convexity. In principle, the longer the duration of the bond, the more sensitive is its price to changes in interest rates--- the curve is non-linear or convex. Those buying these bonds are not worried about adverse swings in interest rates that will hurt prices. And, in fact, some ultra long bonds have seen their yields actually fall (prices rise) since issuance as the world economy softens. More importantly, they feel that the yield over the life of the bond is adequate to protect them during periods when rates rise. In other words, there is a comfort level, even though the duration is extended.

*governments lock in low interest debts. Many governments are faced with extensive infrastructure projects that will take many years to bring to fruition. Having locked in long term debt at very low rates allows government to plan and execute these projects knowing that the funding will be place for the life of these projects.

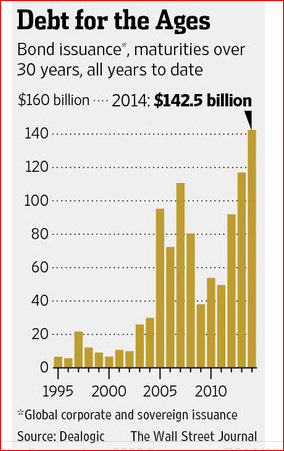

Lest one thinks this is a passing fad, the market for ultra long bonds is now over $140 billion (Chart 1).With the recent success of such countries as Italy, Ireland and Spain—countries considered to be high risk--- we can expect this market to expand.

Chart 1 The Size of the Ultra Long Bond Market

In the 18th century the British government issued “consols” which were ,in effect, perpetual bonds yielding 3 per cent. Today’s consols are the ultra long bonds also yielding within the 3 percent range. A coincidence , perhaps not.

Comments

Log in or sign up to join the conversation.