The $75Bn SpaceX IPO aims for a $1.8 trillion valuation at $135 per share, debuting on Nasdaq under the ticker SPCX on June 12. Investors in mainland China and Hong Kong are excluded.

This has sparked FOMO, driving over $1Bn in volume through Binance’s synthetic exposure product since its launch on May 21, 2026.

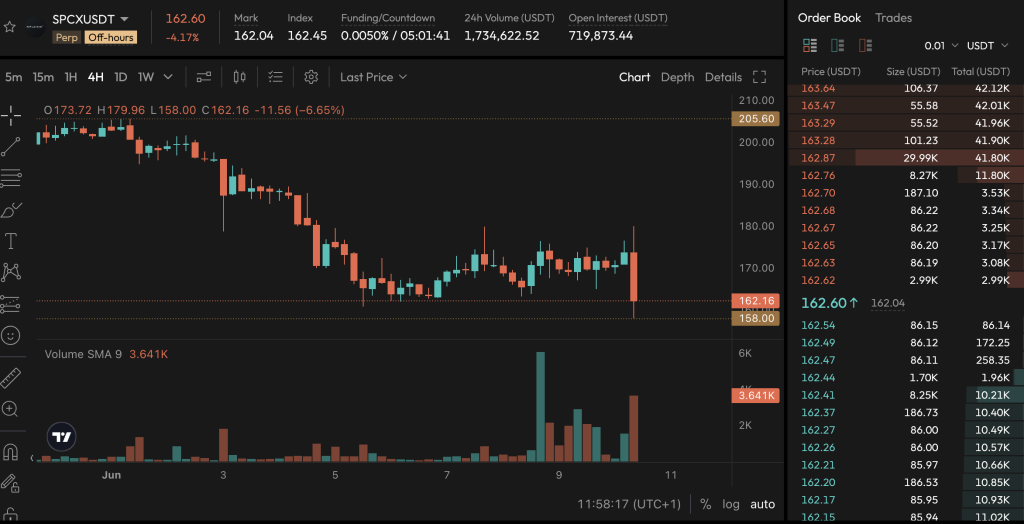

Binance’s SPCXUSDT pre-IPO perpetual futures offer up to 5x leverage and are based on SpaceX’s private-market valuation, carrying no actual equity ownership.

As of June 8, Binance executed a 1.1x contract rebase on open positions, highlighting the experimental nature of these derivatives.

The ITAR Lockout: Why the SpaceX Syndicate Barred Mainland China and Hong Kong From the Record $1.8T IPO

ITAR restricts the export of sensitive defense technology, which directly impacted SpaceX due to its ties with US national security contracts.

Goldman Sachs and Morgan Stanley, the lead underwriters, instructed all banks in the syndicate not to accept orders from investors in mainland China or Hong Kong.

Consequently, the SpaceX website became inaccessible in Hong Kong and Shanghai, showing an Error 1009 for local IPs but loading normally elsewhere.

Chinese online brokers such as Futu and Tiger Brokers informed clients that they would not offer SpaceX IPO allocations in these regions, citing ITAR compliance.

This creates a broad exclusion of investors, highlighting significant regulatory arbitrage as redirected demand flows into synthetic channels.

Chinese Retail FOMO: Offshore Accounts, A-Share Proxies, and the Limits of Every Conventional Workaround

Chinese retail investors and institutional desks in Hong Kong have sought three main workaround channels since the lockout: offshore brokerage accounts in non-restricted jurisdictions, A-share proxy stocks linked to SpaceX’s supply chain, and commercial-space-themed ETFs for broader sector exposure.

However, each channel has limitations. Offshore accounts require accredited-investor status or high asset thresholds, and not all brokers offer access to Chinese nationals.

A-share proxies and ETFs provide indirect exposure to the launch market but don’t connect directly to the SpaceX valuation or SPCX listing price.

As a result, retail investors wanting to tap into the $322Bn AI revenue projection for 2030 find no regulated equity options, creating a demand gap.

This gap, rather than mere speculation, drives the volume of SPCXUSDT on Binance. Elon Musk’s strict stance on Chinese capital in SpaceX contrasts sharply with Tesla’s reliance on China, making TSLA the only publicly traded proxy for Musk’s ventures until SPCX starts trading on June 12.

Binance SPCXUSDT Pre-IPO Perpetual Futures: $1B in Volume, 5x Leverage, and How the Synthetic Gap Trade Works

The SPCXUSDT contract is a perpetual futures instrument linked to SpaceX’s implied private-market valuation via an oracle feed, with no underlying shares or conversion to SPCX shares.

It tracks private-market signals, including Forge Global trades, where SpaceX shares sold for about $129, below the $135 IPO price. The contract allows for 5x leverage, introducing basis risk ahead of the June 12 listing.

On May 18, Hyperliquid launched a synthetic SpaceX perpetual product, generating $33M in first-day volume. In comparison, Binance’s centralized version reached $1Bn by early June, benefiting from its large retail user base and lower friction.

However, Binance’s product has full counterparty exposure, while Hyperliquid relies on on-chain collateral. Both products operate in a regulatory grey zone, with no explicit restrictions on synthetic SpaceX contracts for crypto venues.

What $1Bn in SpaceX Synthetic Volume Reveals: Pre-IPO Derivatives as a Structural Demand Signal for SPCX

The $1Bn SPCXUSDT volume signals demand gathered under challenging conditions, with no equity ownership or passive flows and full counterparty risk on a CEX product.

S&P Dow Jones Indices declined to fast-track SPCX into the S&P 500, blocking an estimated $14Bn to $18Bn in forced index buying due to profitability rules. Until SpaceX’s significant $4.94Bn net loss in 2025 improves, passive demand will remain sidelined.

Goldman Sachs is promoting the orbital compute thesis, projecting a 100-fold increase in SpaceX AI revenue to $322Bn by 2030. Polymarket traders see an 82% chance that the deal will close above $1.8 trillion, while Forge Global’s secondary price suggests caution.

The $1Bn in synthetic SPCXUSDT trading volume reflects genuine demand from excluded retail investors, indicating a stable derivatives market created by the China lockdown.

Comments

Log in or sign up to join the conversation.