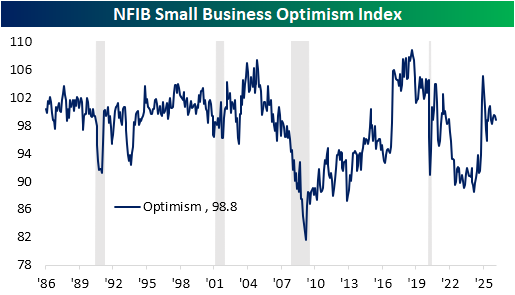

This morning, the NFIB published its latest update on small business sentiment. At 98.8, the headline Optimism Index came in below expectations of 99.6 and last month's reading of 99.3. As shown below, current readings are now middling versus the recent range following the 2024 Election surge and all readings throughout the survey's history. In fact, the current reading is just below the historical median ranking in the 45th percentile.

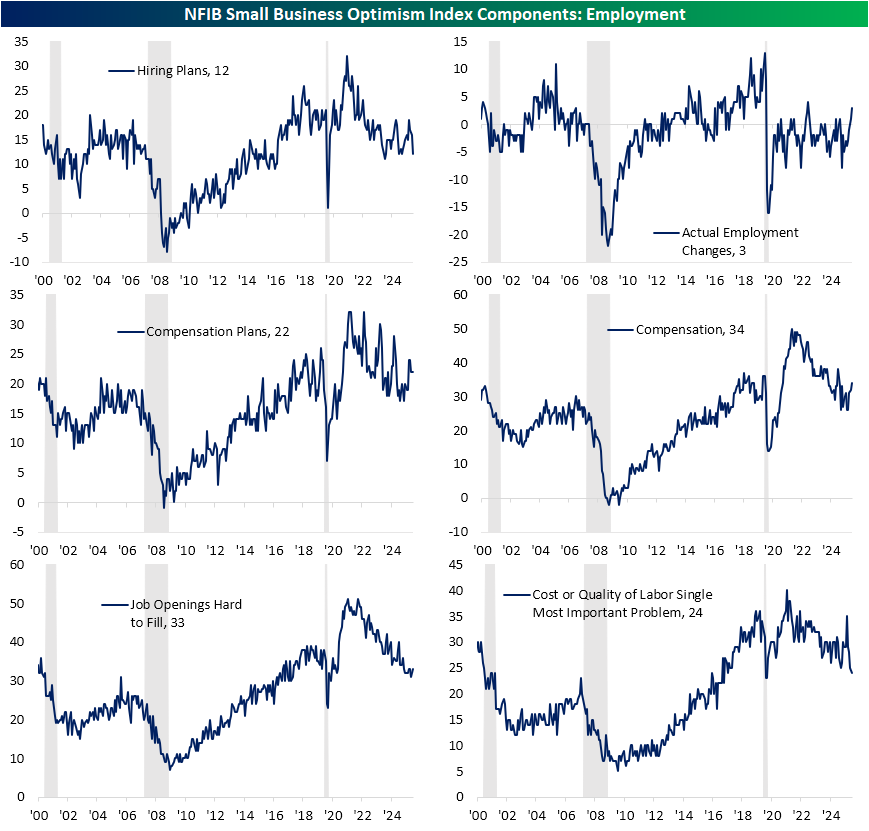

As we discussed in today's Morning Lineup, labor-centric indices included in the NFIB report have suggested improvement over the past year, with another modest month-over-month increase most recently in February. Looking more closely, there are some interesting readings. For starters, hiring and compensation plans appear to be where there has been deterioration. While the latter was unchanged from recent highs in February, the former ranked as one of the larger declines across categories. Hiring plans dropped 4 points to the lowest level since May. Versus the reading of 16 last month, this index went from the 70th percentile down to below the historical median.

Despite those weaker readings in labor-related plans, actual labor changes were much more positive in February. For starters, actual employment changes came in net positive, which has been rare in the post-pandemic period. Further, that was the highest reading since February 2023. Compensation plans rebounded in tow to an eleven-month high. Finally, we would note that among the most important problem section of the report, the combined reading of the two labor-related problems was the lowest since May 2020.

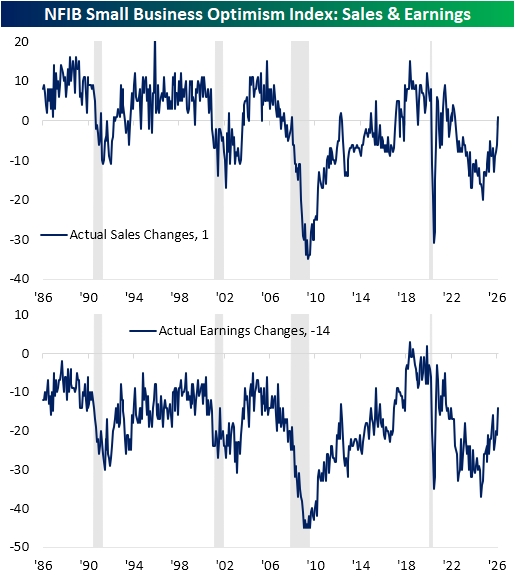

Similar to how "actual" indices were stronger than "expectation" indices regarding labor, the same dynamic was apparent for sales and earnings. Actual sales and earnings both surged in February. Top-line changes were reported as net positive for the first time since May 2022. Actual earnings changes have rarely come in net positive over the history of the survey, but this index rose to the most elevated reading since December 2021.

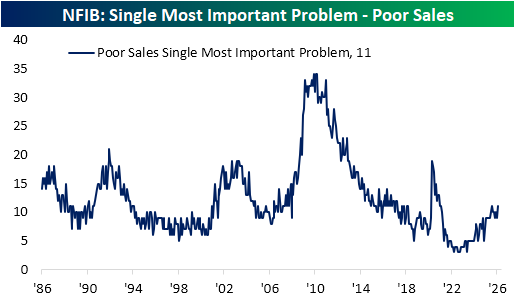

Ironically, the most important problem section again had an idiosyncratic reading versus the aforementioned actual sales change index. 11% of firms reported poor sales as their biggest issue, matching last July for the highest reading since February 2021.

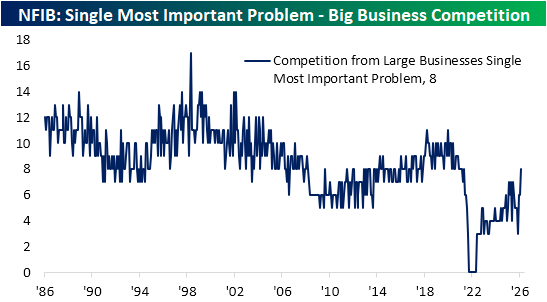

On the heels of the rise in poor sales concerns have been worries about competition from big business. As shown below, that problem has surged from negligible readings in 2022 to 8% of responses in February, the most since May 2021.

Comments

Log in or sign up to join the conversation.