Investors looking at GreenDot (GDOT) may be confused to hear that this company is labeled FinTech. This FinTech label has sent some stocks to sky-high valuations in the past. Looking at the main products though, you will hear a lot of common and typical banking products including:

- bank accounts,

- prepaid debit cards,

- credit cards,

- savings accounts paying 3%,

- and something called moneypak which facilitates payments like PayPal.

The company's strongest selling point may be that they have partnered with several major retailers, such as those listed above. With this list, just about any average American could have access to their services, even if they don't have a traditional banking relationship. Further, some of their products allow people like Uber drivers to have their earnings deposited directly to a prepaid debit card.

I believe the overbought conditions in the stock are due to the FinTech label and irrational investor exuberance, but additionally, a strong economy could be weakening some of the competitive advantage this company has around the "un-banked" customers. At the beginning of 2017, the common stock of this company traded around $24. By 2018, it had more than doubled to $61 and prices topped out around $93 in the fall of 2018. It is currently in sell-off mode.

(Click on image to enlarge)

Now that the prices have corrected, the sharp drop in price is what some investors might characterize as a "falling knife." Above, I identify some long-term price points that could provide support. In early August, the price dropped to as low as $24.19, but rebounded above $27 quickly.

Looking at the historical PE trend, the current valuation is near the lowest points seen in years. Based on next year's earnings projections, analysts expect the company to earn about $3.30 through December 2020. This implies a forward PE of 9.21.

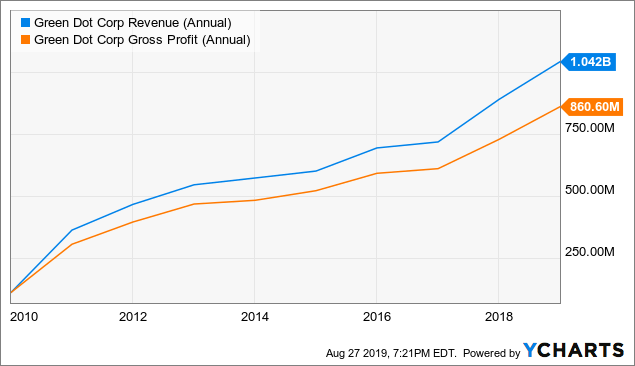

Over the past few years, the company has maintained strong revenue growth and maintained a healthy gross profit as well. However, revenue growth is expected to slow down next year, with revenue growing just 4.31% year over year.

Reading through earnings call transcripts, it appears that investors may be concerned about slowing growth and that starts with some comments made by management.

However, our Account Services segment underperformed our expectations in the quarter and the first half in general, due primarily to a decline in our legacy nondirect deposit active accounts, which we identified as a potential headwind on our last call. These declines continued and accelerated in Q2, resulting in lower than anticipated prepaid unit sales that has caused a material reduction in active prepaid accounts.

In Q2 on a year-over-year basis, we were down by around 500,000 active prepaid accounts, primarily from the loss of nonreloading customers and cash reloading customers, offset by an increase of around 240,000 BaaS active accounts. The digital banking industry segment has become incredibly competitive this year. And over the past several months in particular with several so-called neo-banks, flush with new rounds of venture capital, spending a record amount of marketing dollars to convert customers to their largely free bank account offerings. While Green Dot has fared well historically against competition over many years, and we are still far and away the largest digital bank in this segment, we're taking these competitive pressures seriously.

There's little doubt in our minds that the increased marketing spend from so many competitors in aggregate is taking its toll on our new customer acquisition.

My recommendation is to ease your way into a position by averaging into the stock over time, or just waiting for a lower price. It's too early to tell if analyst estimates might fall further. If conditions continue to deteriorate, the stock could continue to fall, especially since many investors could be sitting on tax losses. Based on forward earnings projections, this stock is a strong buy between $24 to $27.

Comments

Log in or sign up to join the conversation.