There are several schools of thought about debt pay-off with regard to your personal finances. While many of these strategies will work, there are some pluses and minuses to each one. Radio hosts will scream into their microphone if you take an approach that they don't like, but it's really up to you.

One way of thinking says that you should pay down all your non-mortgage debt before investing. This would include debt like credit cards, revolving credit lines, and car loans, but it also includes lower cost debt like student loans. The thinking with this strategy is that people should see all debt as bad debt and proponents argue that there is a psychological barrier created by debt that inhibits you from reaching financial freedom. This is a simple approach. It has worked for many people, but it has drawbacks.

The other strategy takes a more serious and detailed look at your debt and breaks it down into categories. Things like car loans and credit cards are still bad debt because they encourage the borrower to consume more. However, low cost debt like student loans and a mortgage are okay. Sometimes, the interest cost on these loans is so low that it doesn't make sense to pay them off early.

Here's yet another consideration, opportunity cost. If you only focus on the debt side of your personal balance sheet, you are ignoring the opportunity cost of your assets. It's nice to get that guaranteed 3.5% return by paying off your mortgage early, but it would be even nicer to get a 10% return by investing.

My personal strategy around these debts is that you work hard to pay off your more expensive debts, usually the ones with APRs over 7%. Then, you make minimum payments on your other debts, with rates under 7%. Why 7%? Well, that's just slightly below the rate achievable by investing long-term in the stock market.

Historically, the S&P 500 has returned about 9.8% per year1 for many decades. So, long-term expectations could possibly match that outstanding growth. Or, possibly we could have reached a peak and the markets may under-perform. There's risk either way. Using 7% as our benchmark, we know that we have a cushion for under-performance of almost 3%.

What about now?

The biggest flaw in the advice given by many advisors is to ignore the past performance of the market. They ask people to put on their blinders and follow a strict plan. Well, this current bull market is hard to ignore. Total return, including dividends, for the S&P 500 for 2019 was 33.07%. 2 There is a growing chorus of people pointing out that we have the most expensive markets ever, with declining earnings.

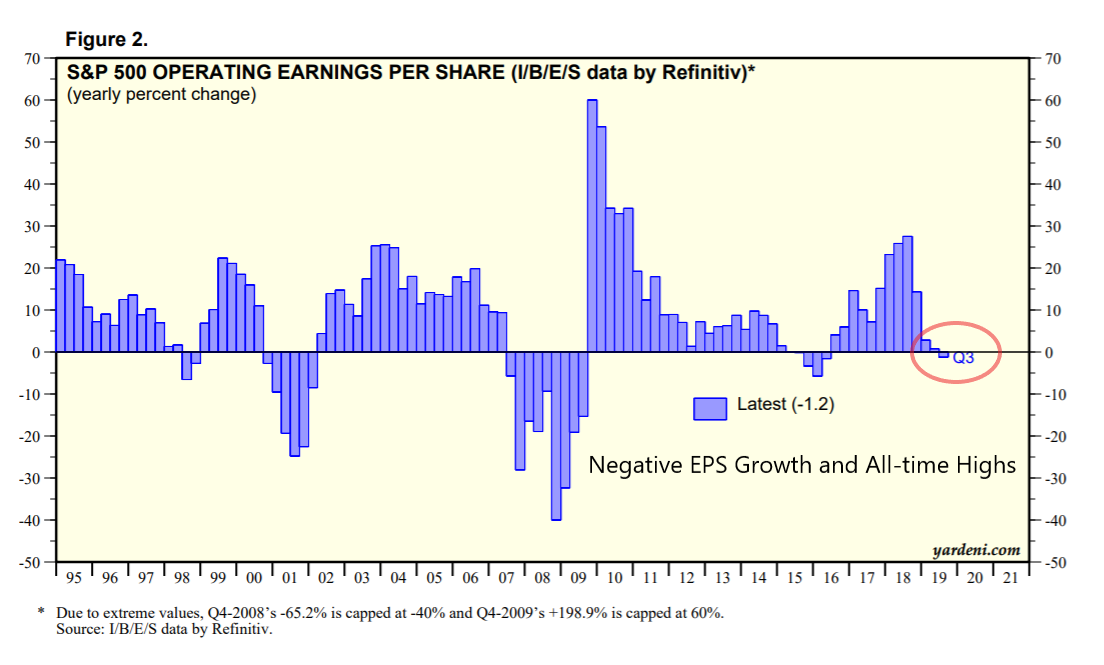

Here's a view of earnings growth for the S&P 500. Note that for the first time since 2016, earnings growth is negative.3

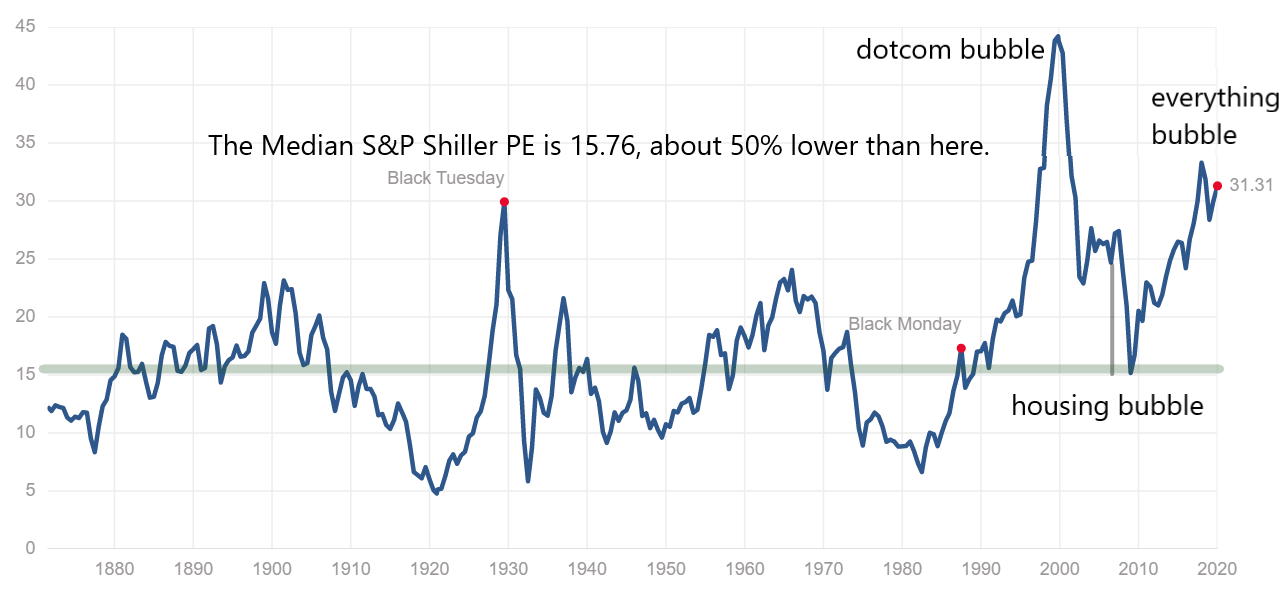

Meanwhile, historical measures of valuation indicate that we are sitting in the bubble zone. The Shiller P/E is at 31.31, while the median for this measure is actually 15.76.4 The Shiller PE is a "price earnings ratio is based on average inflation-adjusted earnings from the previous 10 years, known as the Cyclically Adjusted PE Ratio." It is not largely affected by a small drop earnings during one quarter. It's a long-term measure of valuation.

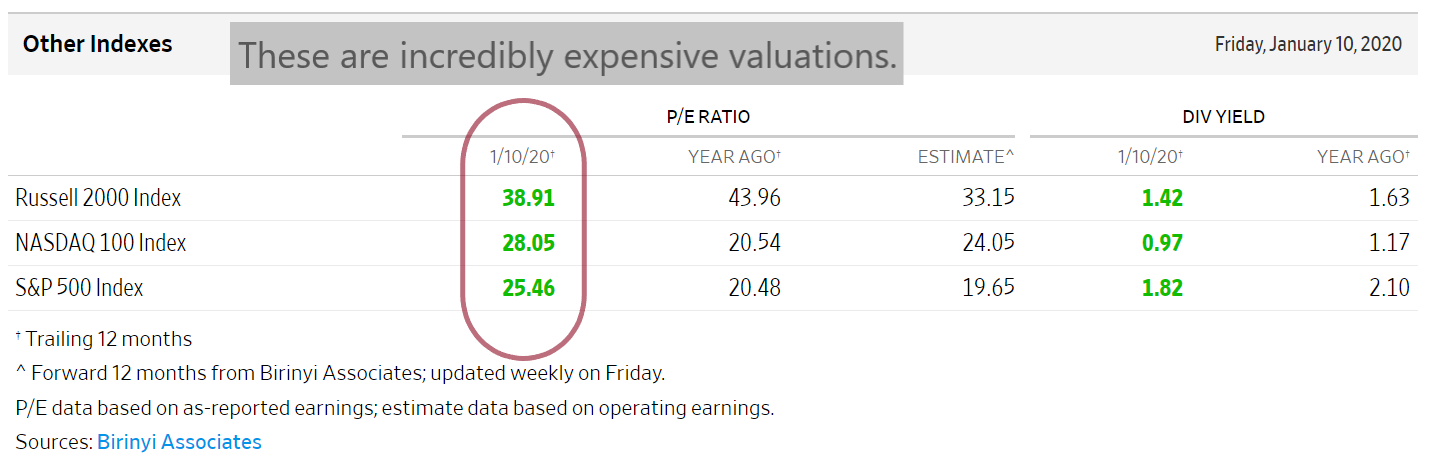

There are some people that are critical of the Shiller PE valuation metric. They believe it is an outdated method and market valuations are better represented by the Fed model. The idea is that you looking at the S&P 500 earnings yield and compare that to the risk free rate provided by Fed intervention. So, what is the S&P 500 earnings yield? It's the inverse of the current PE ratio. This simple PE ratio for the S&P 5005 is currently 25.46 and that creates the earnings yield as 1 / 25.46, or 3.92%.

This article has focused on the S&P 500, but the rest of the market indices are no different.

What's the point of this?

If earnings growth is negative and the S&P 500 is at record levels, then individuals need to take a long look at their capital allocation. Does it make sense to leave debts unpaid, if the earnings yield of the S&P 500 is only 3.92%? Does it make sense to put any more money into a stock market that is possibly poised for a 50% drop in value? An investor looking at their capital allocation really should be thinking of paying down their debts, especially if those debts have a cost higher than 4%. For the first time ever, I'm thinking that I really should consider paying down my student loans and mortgage, before I put more money into the stock market. Any advisor that tells someone otherwise is acting like a fool. If you don't have debt, then raising cash might be prudent as well.

--------

References

1 Merriman, P. (2015). Understanding performance: The S&P 500 Index. https://www.marketwatch.com/story/understanding-performance-the-sp-500-in-2015-02-18

2 PK. (2019). 2019 S&P 500 Return. https://dqydj.com/2019-sp-500-return/

3 Yardeni. (2020). https://www.yardeni.com/

4 Shiller. (2020). Shiller PE Ratio. https://www.multpl.com/shiller-pe

5 WSJ. (2020). PE Ratios. https://www.wsj.com/market-data/stocks/peyields

Comments

Log in or sign up to join the conversation.