The wild indiscriminant selling in equities we witnessed over the last month seems to have eased lately, encouraging many market participants to believe the worst of the sell-off is over. Some even believe that the S&P 500 has already bottomed on March 23rd at 2237.40. However, before jumping in, investors must appreciate the unprecedented nature of this situation, and that getting back to normal could take longer than many currently envision. While financial assets tend to bounce back before the broader economy does, the trouble in equity markets may not be over yet.

(Click on image to enlarge)

US Economy

As the US government (along with various other governments around the world) is forced to shut down the economy to contain the virus, it has consequently been followed by unprecedented stimulus efforts by both the government/Treasury and the Federal Reserve.

Though even after the Fed’s various efforts to support credit markets and the government’s $2.2 trillion fiscal stimulus package, adverse economic ramifications have been inevitable. We’ve already witnessed two back-to-back weeks of record unemployment benefit claims, as last week’s report revealed 3.3 million filings, followed by 6.6 million in this week’s report. Furthermore, the March non-farm payrolls report revealed that the unemployment rate jumped to 4.4%, and 701,000 jobs were lost through March 12th, before the US economy even went into shutdown mode. The dismal jobs number is only the tip of the iceberg, as the non-farm payrolls report next month, along with GDP reports, will give us greater insight into the true ramifications of the unprecedented lockdowns.

Businesses don’t know how long this pandemic will last, thus many firms are becoming reluctant to hold onto staff amid forced shutdowns. This is expected to result in record unemployment rates (at least 10%) and unprecedented GDP contractions in at least the first and second quarter of this year.

The resolution of this coronavirus would certainly be the first, and welcome, step towards returning to normalcy, but economic conditions could take time to restore to pre-coronavirus times. The end of the lockdown may not necessarily lead to businesses embarking on a hiring spree, meaning that the jobless claims number may not naturally decline at the same rate it has escalated. Keep in mind that coming out of this crisis, various businesses (especially the hardest-hit industries like airlines) will have heavier debt loads to repay. Moreover, the government’s fiscal stimulus also entails $500 billion in loans for troubled US corporations as a result of COVID-19.

US corporate debt levels are already extremely elevated, standing at $9.5 trillion. Hence, worsening debt levels as a result of this crisis will mean greater repayment burdens in the aftermath of this pandemic, limiting business’s abilities to engage in hiring sprees and corporate expansion plans. Given that consumer spending accounts for around 70% of GDP in the United States, weak employment conditions (relative to pre-coronavirus conditions) would imply weaker consumer spending trends, and a slower economic recovery path. Though a lot also depends on how generous the government decides to be to businesses, whereby if the additional debt burdens are forgiven in exchange for employee retention and other conditions, then we could witness a faster economic recovery.

Furthermore, while the $2.2 trillion fiscal stimulus is certainly a step in the right direction, it is still not enough to combat this unprecedented crisis. As part of this legislation, the Treasury received $450 billion to boost its Exchange Stabilization Fund, to support the Federal Reserve in handling default risks amid the unprecedented lending facilities rolled out to overcome this catastrophe. However, Scott Minerd, the chief investment officer at Guggenheim Partners, believes the Treasury will need to receive at least around $2 trillion for it be able to sufficiently support the economy through the crisis. The need for additional government support will only magnify the longer this pandemic continues.

Equities

As soon as we witness improvements regarding the crisis, whether in terms of declining cases/deaths, or the discovery of a medicinal cure/vaccination, markets will most certainly bounce higher, as a path to economic normalcy will finally be visible amid the end of forced lockdowns.

However, according to sources, “a number of epidemiologists have also suggested that once lockdowns are relaxed, the world will be at risk of rates of infection rising again”. This would induce more lockdowns/ economic shutdowns, and pressure equities once again. Though in a previous article, through a unique form of analysis I had revealed that we can expect the pandemic crisis to abate by May (latest). Hence, this risk of re-acceleration in infection rates would only occur if the government were to prematurely end lockdowns, the chances of which seem evidently low in places like the US and Europe. Therefore, investors should not fear the resurgence of this coronavirus going into next month, though until then, stocks could remain under pressure.

That being said, once the bounce higher in stocks occurs as the virus abates, the path forward for equities may not necessarily be a straight line up, and we could even witness a period of sideways movement in the stock market. Following the crisis, companies will need to focus on repaying the high debt burdens, which could be exacerbated by rising yields (leading to higher interest rates across the economy) as we witness a reversal in safe-haven buying that has occurred amid this dilemma.

Furthermore, while the fact that stocks are down more than 20% (in bear market territory) from the all-time highs reached on February 19th can entice investors to buy into this market, the stock market overall is not necessarily in massive discount territory, especially given the fact that equities were already very expensive coming into this pandemic.

Most of the typical valuation metrics, such as forward P/E and P/S, can be considered meaningless at the moment amid the uncertainty regarding the extent of damage caused to business activity due to the unprecedented lockdowns.

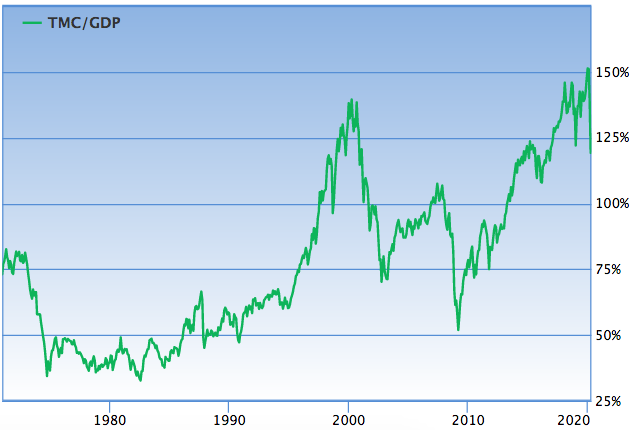

Nevertheless, one noteworthy metric is the total stock market capitalization to GDP ratio, which currently stands at 116% (1.16), reflecting that stocks are still significantly overvalued relative to the size of the economy, and also relative to its average since 1970, which is 0.8. Furthermore, take into consideration the fact that the current GDP number used to calculate the ratio still doesn’t completely reflect the contraction as a result of COVID-19. Hence, the stock market is actually even more expensive than currently indicated by the ratio.

In fact, to put this into more context, during the height of the Global Financial Crisis this ratio had reached a bottom of 0.6. So while stocks may appear more appealing relative to the February peak, when the ratio was at a record-high of 1.5, they still can’t be considered dirt cheap to entice investors to bet the ranch (especially for passive-style investors).

Bottom Line

While stocks have been rebounding recently, there are still a lot of unknowns surrounding the coronavirus, in terms of its impact on both the US and global economy. Higher debt repayments and a weaker jobs market in the aftermath of this crisis could slow down the economic recovery, though a lot is also dependent on how far the government goes to support Corporate America through this catastrophe.

Even though stocks have notably retreated from their all-time highs in February, they are still very expensive, with a stock market capitalization to GDP ratio of 1.16 (well above the 0.8 average). Therefore, while certain individual stocks could be cheap enough to buy into, the valuation of the broader market overall is still very lofty, and not one where investors should go all in.

Comments

Log in or sign up to join the conversation.