S&P’s rating affirmation provides much-needed breathing space ahead of a heavy second half.

S&P’s rating affirmation is a much-needed reprieve and means that downgrade fears have been put off to 4Q20. The next six months will be decisive for Romania’s political and fiscal outlook which remains fragile, but near-term optimism is underpinned by the European Central Bank repo line and hopes on a European recovery fund.

In line with our expectations, S&P affirmed Romania’s BBB- rating which remains on a negative outlook. The rating agency said that “Romania will have the ability to absorb the level of deterioration” from Covid-19, notably with debt/GDP expected to increase by 11 percentage points to 46.2% over 2020 on the back of a 5.9% GDP contraction and an 8% fiscal deficit, thanks to solid market access, measured monetary policy, and EU membership.

Our take is that despite the negative fiscal fallout from Covid-19, rating agencies appear willing to wait, in the case of S&P reflected by the reference to “risks to Romania’s fiscal and external balances over the next 18 months”. However, as we highlighted in our note of 29 April, the next six months will be crucial for rating agencies and markets. First, the 40% pension hike penciled in for September poses a key risk, and in line with our view (and that of Fitch), S&P now expects that the crisis will allow the government to reduce the hike to 10%. Second, hopes are underpinned by a credible medium-term fiscal strategy post-election (around December 2020).

For now, near-term risks of a downgrade have disappeared but uncertainty about the pension hike and populistic initiatives ahead of the elections mean that downgrade fears will run high into the rating reviews in 4Q20 and beyond (see table below for review dates and rating drivers).

Rating drivers/factors that could lead to an upgrade or downgrade

Source: Moody’s, S&P, Fitch Ratings, ING

Many questions unanswered on ECB repo line and EU recovery fund

Just hours before S&P’s review on Friday, the ECB and National Bank of Romania announced a repo line of EUR4.5 billion aimed at securing Romania’s access to euro liquidity should there be a need. The timing was interesting as – putting aside the upcoming S&P rating review – market concerns about Romania’s FX reserves and access to hard currency market funding had decreased (reflected by the recent EUR3.3bn Eurobond issuance in end-May). We also note that in contrast to Bulgaria and Croatia (both ERM II accession candidates), Romania had secured a repo instead of a swap line. There are however few details beyond the headline (notably on the cost, the NBR’s exact reserve structure and what would be considered as “high-quality euro-denominated collateral”), and we can only focus on the outcome which is essential that Romania’s access to funding is looking better with, rather than without, this facility.

Although with no implications this year, Romania’s economic and fiscal story for the following years could be substantially influenced by the recently proposed European recovery fund. While the matter is still subject to negotiations, at least at first sight Romania will be one of the main beneficiaries, standing to receive around EUR31bn, roughly split into EUR19.5bn in grants and EUR11.5 in loans. Importantly, the net amount will be only around EUR19bn as Romania will need to contribute EUR12bn to the fund. According to official statements, the funds will be primarily used for highways, healthcare, and education. Recognizing the complexities in negotiation patterns at the EU level, we are waiting for the final version of the plan to be approved before starting to crunch numbers and estimating how much the fiscal story will be influenced.

Crunch time for policymakers

After a surprisingly resilient 1Q20 when the economy advanced by 0.3% vs 4Q19, we recently revised this year’s GDP contraction forecast to -5.5%.

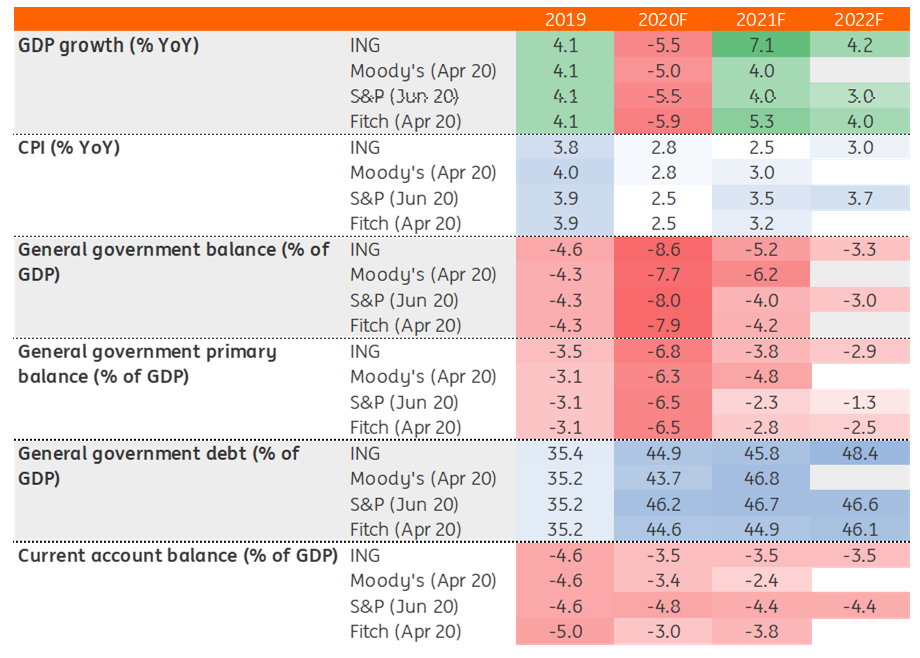

Comparison of INGF and rating agency forecasts

Source: Moody’s, S&P, Fitch, ING

On the fiscal outlook, given the budget execution data after the first four months and the prospects of having pensions raised by 10%, we have revised our budget deficit forecast to 8.6% of GDP for 2020 at the same time. As we have highlighted before, the pre-election environment makes estimations particularly uncertain, on top of the already high uncertainties generated by the coronavirus outbreak.

On monetary policy, the NBR recently cut the key rate from 2.0% to 1.75% which likely marks the end of the road for this key rate cut cycle. Meanwhile, the NBR’s presence in the secondary bond market will likely remain a constant in upcoming months, with the intention to maintain the feasibility of public finances. In total, we believe that the central bank will need to buy the equivalent of at least 1.5% of GDP in 2020.

On the political front, things start to heat up again, after a period of relative calm during the lockdown. The PSD (which, together with its allies, controls Parliament) has threatened a no-confidence motion should the pension hike be less than the scheduled 40%. There is an increasingly probable scenario where we could see the government being toppled but still be allowed to continue its work on an interim basis until the elections. This would seriously limit its abilities to control spending for the remainder of the year and to counter the spending-increasing initiatives still likely to be promoted in Parliament. The latest polls continue to point to a lead for the ruling PNL but down from a peak of around 47% in January.

Comments

Log in or sign up to join the conversation.