Image: Bigstock

The Q2 earnings season gets going in earnest this week, with almost 70 companies on deck to report results, including 29 S&P 500 members. The big banks dominate this week’s reporting docket, but we also have several bellwethers from other sectors reporting, including Netflix (NFLX), Johnson & Johnson (JNJ), UnitedHealth Group (UNH), United Airlines (UAL), and others.

If you’ve been following our earnings commentary over the past year, you’re already familiar with the "improving earnings narrative" we keep talking about. In plain English: when you look at the S&P 500 as a whole, aggregate profit estimates are consistently trending upward.

For over a year, the Tech sector single-handedly carried the torch for these upward revisions. Recently, though, the rally has found reinforcements. The Energy and Basic Materials sectors have vigorously joined the party, largely thanks to a geopolitical bump from developments in the Persian Gulf back in early March.

In fact, the shift in Energy has been spectacular—Q2 earnings estimates for the sector have roughly doubled since April. Utilities and Finance are also enjoying a nice lift, seeing their Q2 expectations climb higher as the quarter progressed.

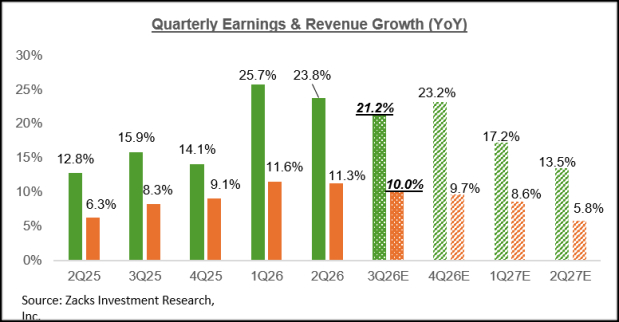

To give you a bird's-eye view of how this all shakes out, the chart below maps out the total S&P 500 earnings landscape. It highlights current Q2 expectations right alongside actual results from the past four quarters and forecasts for the next four.

Image Source: Zacks Investment Research

As you can see here, total S&P 500 earnings for 2026 Q2 are expected to increase by +23.8% compared to the same period last year on +11.3% higher revenues.

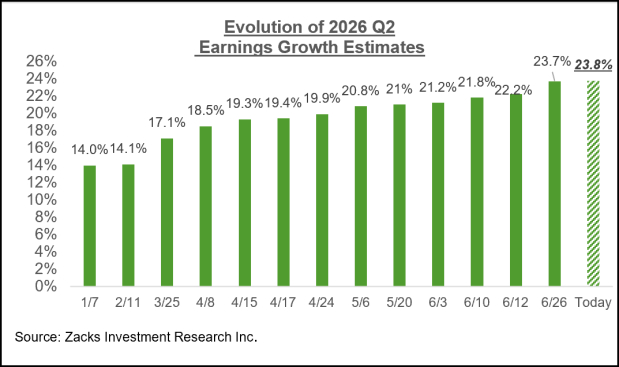

The chart below shows how 2026 Q2 earnings growth expectations have evolved lately.

Image Source: Zacks Investment Research

With Q2 earnings expectations surging by nearly 7 percentage points over the last three months, the bar has been set exceptionally high. Naturally, some market watchers are getting a bit anxious that companies might trip up and miss these loftier targets in the days ahead. If they do come up short, it could spell trouble for a stock market currently sitting right at all-time highs.

We don't view these earnings expectations as overly ambitious. In fact, there is plenty of underlying fundamental momentum to keep driving profit forecasts higher.

The chart below shows the earnings picture on an annual basis.

Image Source: Zacks Investment Research

Big Banks in the Spotlight This Week

JPMorgan (JPM - Free Report), Wells Fargo (WFC - Free Report), Citigroup (C - Free Report), and Bank of America (BAC - Free Report) will kick off the Q2 reporting cycle for the Finance sector on Tuesday morning.

Estimates for the Finance sector, as well as for these money-center banks, have moved higher since the start of the period, reflecting positive momentum in the core commercial banking business, continued strength in the trading business, and overall stable trends in investment banking activities. Aggregate industry data suggests that JPMorgan, Wells Fargo, Citigroup, and Bank of America will likely report their best loan growth numbers in almost three years.

For Wells Fargo, the expectation is of +12.3% EPS growth on +4.7% revenue growth, while Q2 EPS for JPMorgan, Bank of America, and Citigroup are expected to increase by +11.3%, +27%, and +38.8% from the same period last year, respectively.

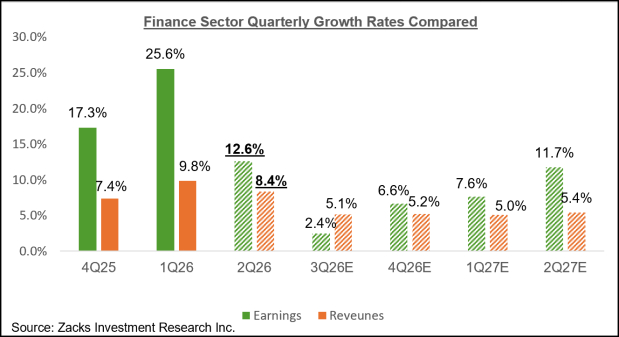

For the Finance sector as a whole, total Q2 earnings are expected to increase by +12.6% from the same period last year on +8.4% higher revenues, as the chart below shows.

Image Source: Zacks Investment Research

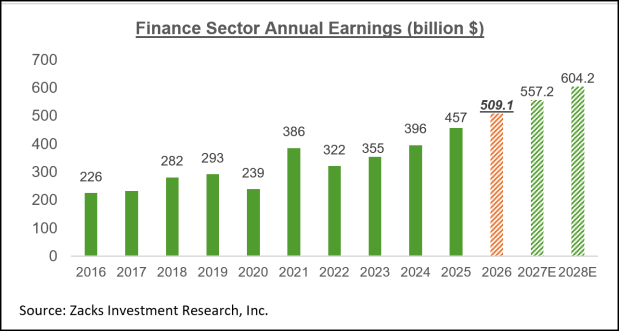

For full-year 2026, total Finance sector earnings are expected to increase by +11.4% compared to +15.3% earnings growth achieved last year and expectations of +9.4% growth in 2027. Please note that these are record aggregate earnings totals for the Finance sector, as the chart below shows.

Image Source: Zacks Investment Research

Q2 Earnings Season Scorecard

While many in the market will tune in to the Q2 earnings season this week, the reporting cycle is already underway. Through Friday, July 10th, we have already seen quarterly results from 18 S&P 500 members. All of these 18 index members have reported results for their respective fiscal quarters ending in May, which we count as part of our June-quarter tally.

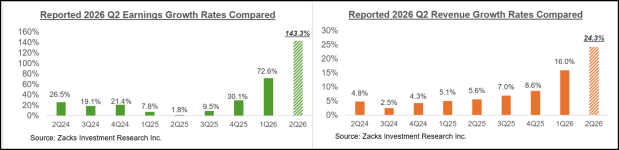

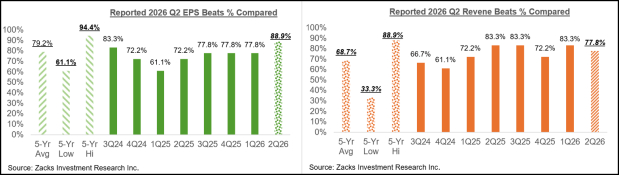

Total earnings for these 18 index members that have reported results are up +143.3% from the same period last year on +24.3% revenue gains, with 88.9% of the companies beating EPS estimates and 77.8% of them beating revenue estimates.

The comparison charts below put the Q2 earnings and revenue growth rates for these index members in a historical context.

Image Source: Zacks Investment Research

The comparison charts below put the Q2 EPS and revenue beat percentages in a historical context.

Image Source: Zacks Investment Research

We are not drawing any conclusions from these results, given the small sample size at this stage.

Comments

Log in or sign up to join the conversation.