With increasing term spreads (or, steepening of the yield curve), fears of imminent recession have waned. Does this make sense?

In previous posts [1], I have been reporting estimates of a recession-month 12 months ahead, using probit models, estimated 1985 onward. Here, I use unadjusted 10yr-3mo spreads as well as adjusted by estimated term premium, 1967-onward. But what might be of greater interest is whether a recession will start any time within the next twelve months.

In order to assess this, I estimate two probit regressions, 1967-2019M11. First, the conventional specification.

Prob(recessiont+12) = -0.245 – 0.752 spreadt + ut+12

McFadden R2 = 0.31, NObs = 623. Coefficients significant at 5% msl bold. The spread is in percentage points.

Next, the specification for recession any time within the next twelve months

Prob(recessiont,t+12) = 0.266 – 0.595 spreadt + ut+12

McFadden R2 = 0.21, NObs = 623. Coefficients significant at 5% msl bold. The spread is in percentage points.

The resulting recession probabilities are shown in Figure 1.

Figure 1: Estimated probability of recession within 12 months up to indicated date (blue), and in indicated month (red). NBER recession shaded gray. Light green shading denotes forecast period. Source: NBER and author’s calculations.

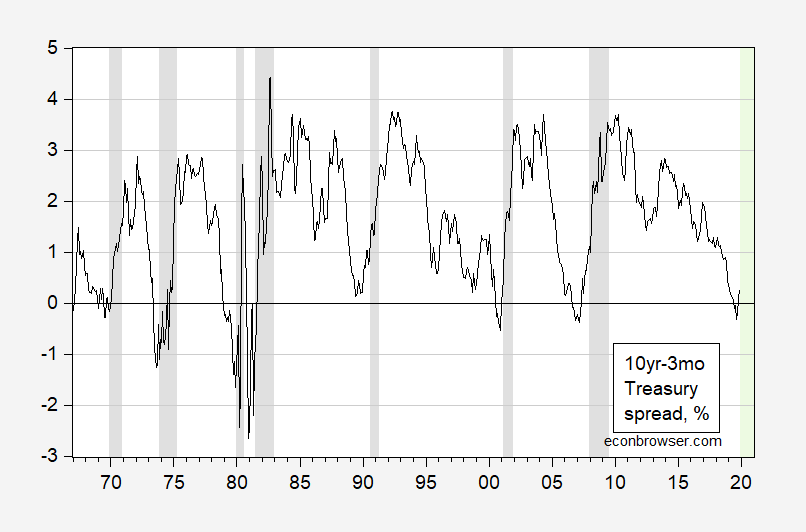

These estimates based on the 10yr-3mo spread (3 month is Treasury bill secondary market).

Figure 2: Ten year-three month Treasury spread, % (black). NBER defined recession dates shaded gray. Light green shading denotes the forecast period. Source: Federal Reserve via FRED, and NBER.

While the estimated probability of a recession in November 2020 is 33%, down from 50% for August 2020, the estimated probability of a recession within the next twelve months is fairly high, at 54%.

So, too early to relax…

Comments

Log in or sign up to join the conversation.