From BLS today:

The Producer Price Index for final demand increased 1.0 percent in July, seasonally adjusted, the U.S. Bureau of Labor Statistics reported today. Final demand prices rose 1.0 percent in June and 0.8 percent in May. (See table A.) On an unadjusted basis, the final demand index moved up 7.8 percent for the 12 months ended in July, the largest advance since 12-month data were first calculated in November 2010.

Nearly three-fourths of the July increase in the final demand index can be traced to a 1.1-percent advance in prices for final demand services. The index for final demand goods rose 0.6 percent.

The PPI and core PPI inflation rates topped the Bloomberg consensus numbers.

Here’s the CPI against the PPI for final demand, and less discussed PPI for final, finished goods. (For more on yesterday’s CPI, see this post.)

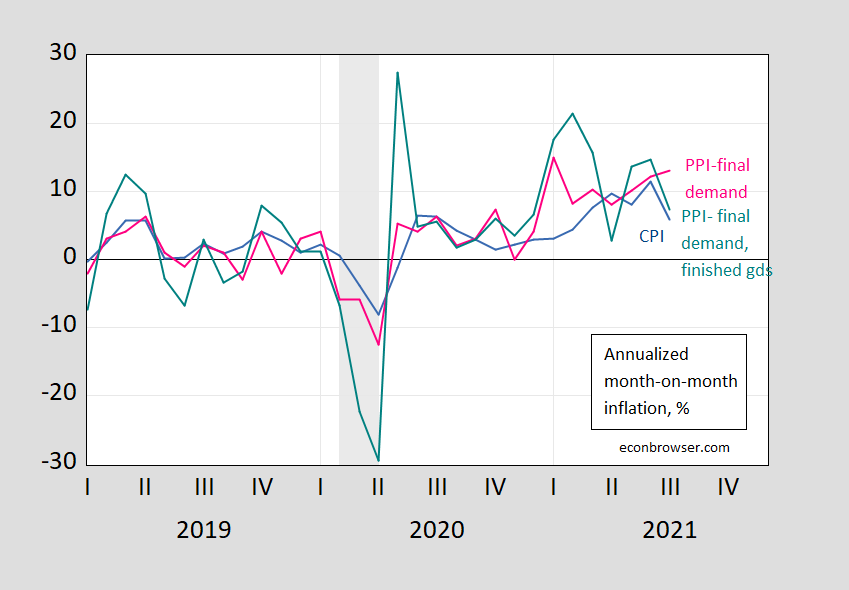

Figure 1: Month-on-month annualized inflation rate for CPI for all urban consumers, goods and services (blue), PPI for all final demand, finished goods (pink), and PPI for all commodities (teal), all in %. Source: BLS and author’s calculations.

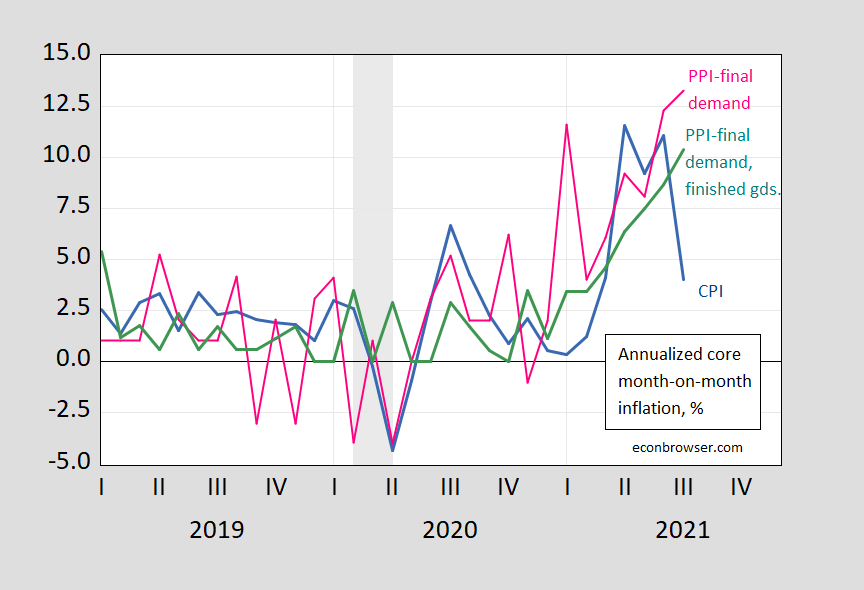

Core measures show continued acceleration, m/m. (Note, scale is narrower in below figure.)

Figure 2: Month-on-month annualized inflation rate for CPI for all urban consumers, goods and services ex-food and energy (blue), PPI for all final demand (pink), and PPI for all final demand, finished goods ex-food and energy (teal), %. Source: BLS and author’s calculations.

Do PPI’s lead CPI’s in the US? Clark (1995) provides a skeptical view that PPI’s provide additional systematic predictive power.

Some analysts project that recent increases in prices of crude and intermediate goods will pass through the production chain and generate higher consumer price inflation. While simple economics suggests such a pass-through effect may occur, more sophisticated reasoning and careful consideration of the construction of the PPI and CPI data suggest any pass-through effect may be weak. Consistent with this more sophisticated analysis, the empirical evidence also shows the production chain only weakly links consumer prices to producer prices. PPI changes sometimes help predict CPI changes but fail to do so systematically. Therefore, the recent increases in some producer price indexes do not in themselves presage higher CPI inflation.

Caporale et al. (2002) uses a more formal multivariate approach to conclude that for G-7 economies, PPI’s do lead CPI’s. Whether these findings still pertain in the current environment (and using the updated versions of the PPI) remains to be seen.

For now, Cleveland Fed‘s nowcasts indicate that using their model, m/m July PCE inflation has risen and core inflation fell in response to today’s release of PPI information.

Comments

Log in or sign up to join the conversation.