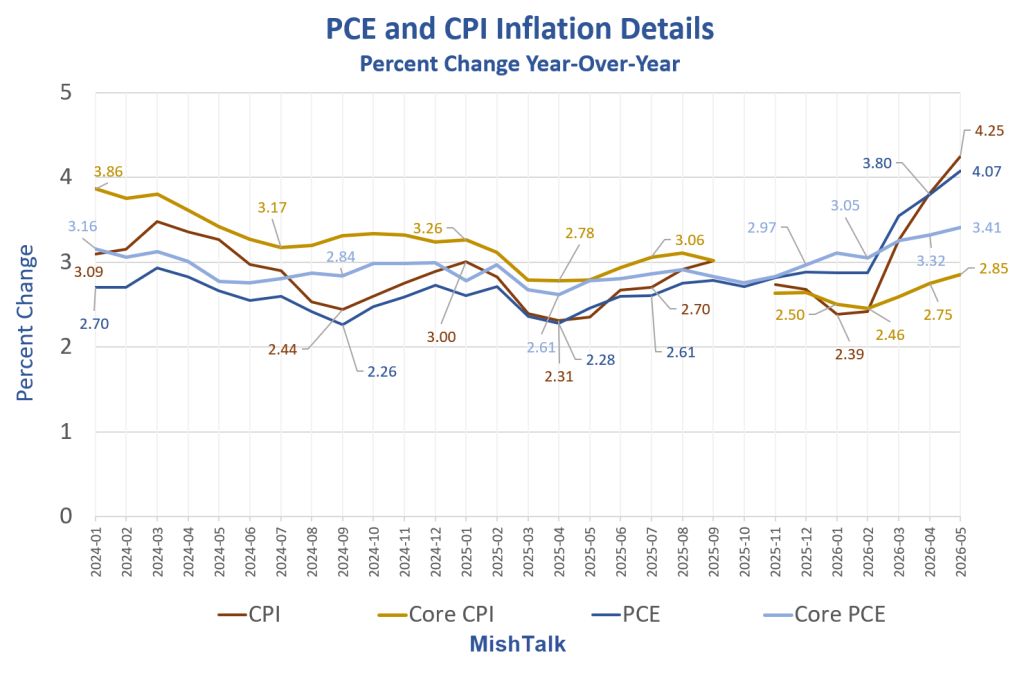

The Fed’s target is 2.0 percent, actual is 4.1 percent, up 0.4 percent from last month.

The BEA’s Income and Outlays report shows the PCE Price Index is up 0.4 percent from last month and 4.1 percent from a year ago.

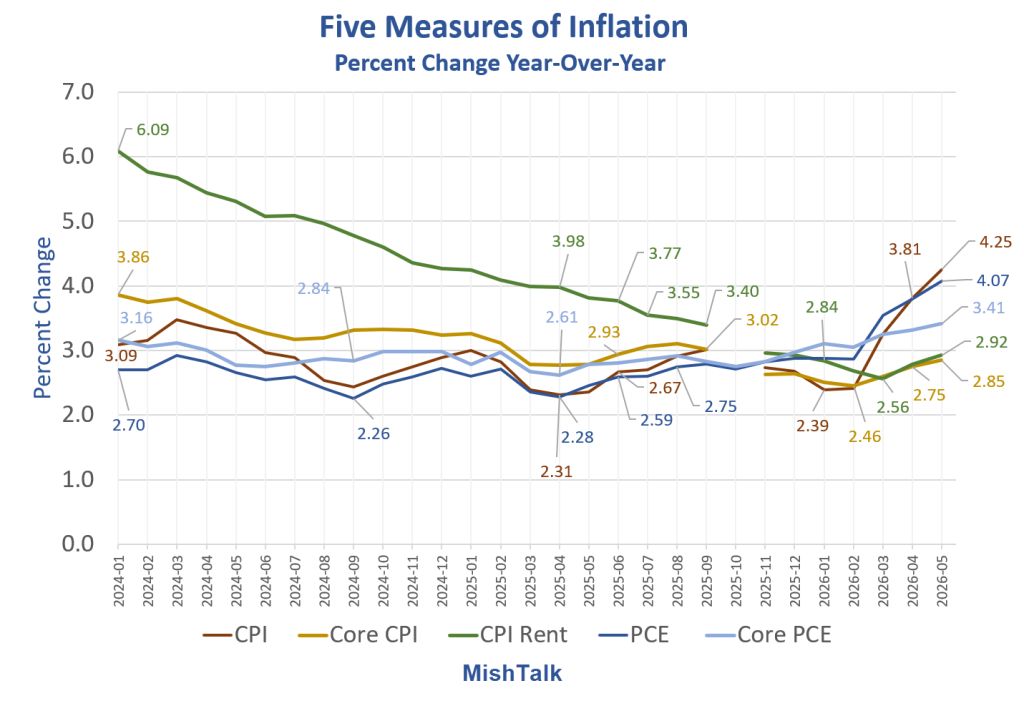

Five Measures of Inflation Year-Over-Year

CPI: 4.25

Core CPI: 2.85

CPI Rent: 2.92

PCE: 4.07

Core PCE: 3.41

I calculate to two decimal places, the reports rounds to one decimal place.

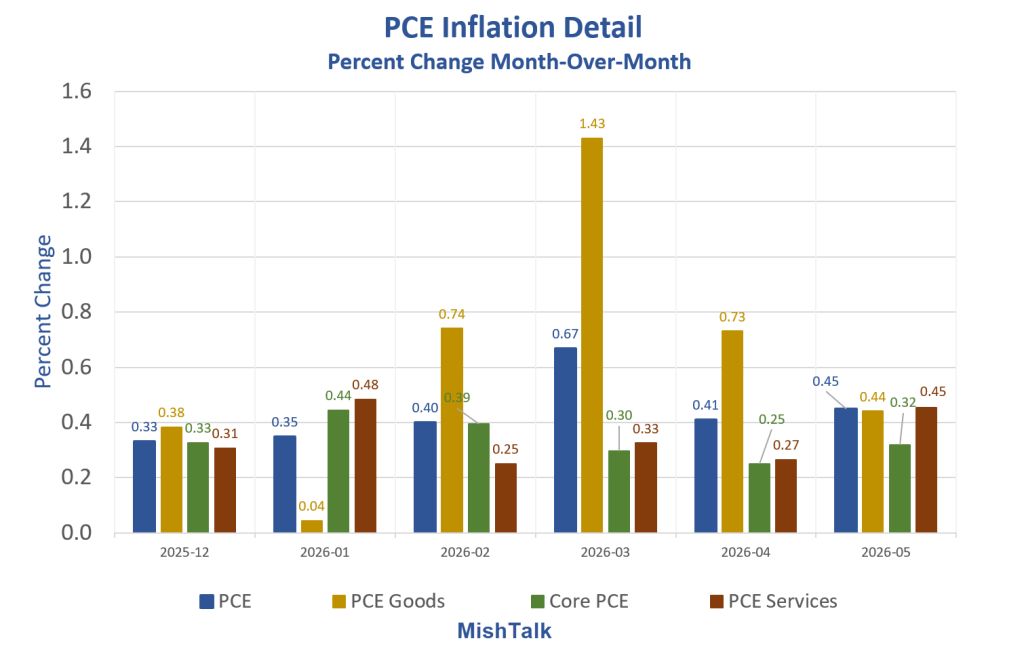

PCE Inflation Detail Month-Over-Month

PCE Month-Over-Month Percent Change

PCE: 0.45 percent

PCE Goods: 0.44 percent

Core PCE: 0.32 percent

PCE Services: 0.45 percent

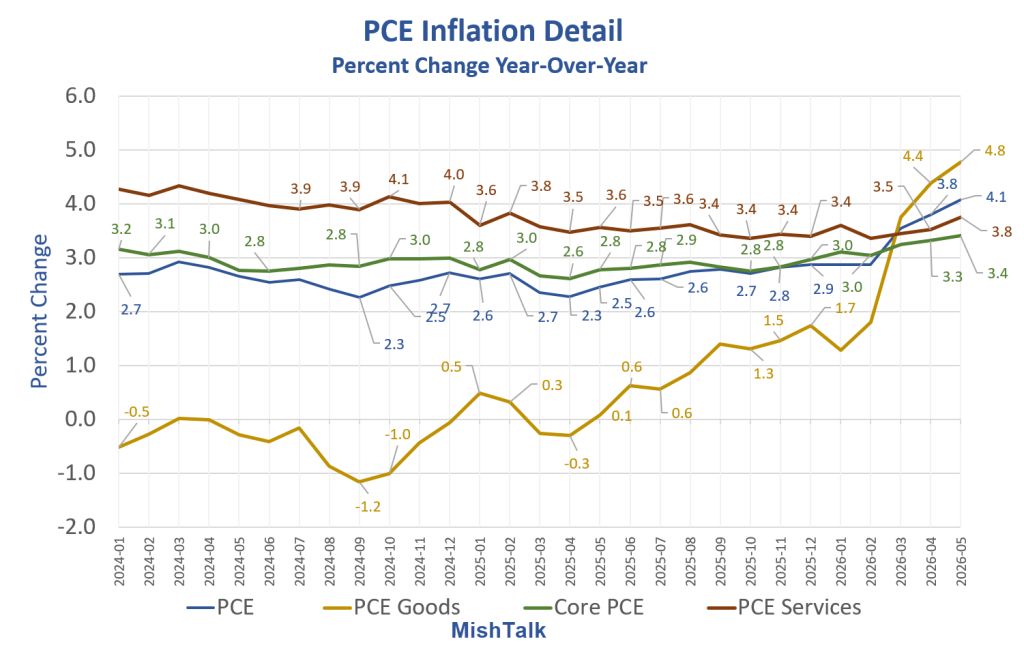

PCE Year-Over-Year Detail

PCE Year-Over-Year Percent Change

PCE: 4.1 percent

PCE Goods: 4.8 percent

PCE Services: 3.8 percent

Core PCE: 3.4 percent

The PCE was last under 2.0 percent in February of 2021, 63 months ago.

The Main Question

The main question is less whether both headline and core go up—they are widely expected to—but rather how “stale” these numbers already are.

Specifically, the consensus forecast is for monthly headline inflation to edge higher from 0.4% to 0.5%, with the annual rate rising from 3.8% to 4.1%. Monthly core is expected at 0.3% (from 0.2%) and the annual rate at 3.4% (from 3.3%).

These numbers come before the recent sharp fall in oil prices, which will result in lower headline inflation and ease some of the pressures on core. The question being debated is by how much, including whether May will prove to be the peak inflation month.

Looking Ahead

Goods inflation is going to drop substantially due to falling gasoline prices.

However, services are 65 to 70 percent of the PCE price index. If medical care services and housing are elevated, the disinflation will be less than most expect.

On a year-over-year basis, the next four months are neither difficult nor easy to beat. It’s not until January of 2027 before year-over-year comparisons become easy to beat.

By January 2027, anything can happen ranging from mild stagflation to a disinflationary recession crash.

Consumer and Corporate Spending Buoyancy

Much buoyancy in consumer spending comes from the stock market.

Much buoyancy in corporate spending is related to AI.

Completing the circle, AI is fueling the stock market, trucking and other things.

Expect housing to remain in the gutter. And expect hiring to be weak.

Effectively, the economy is firing on one cylinder: AI. But it’s a big cylinder.

So, a key question is “Where does AI take us?” But no one can say for sure.

Other Factors

AI is not the end of it. The war in Iran can easily break out again. But that’s not my expectation.

In contrast, I expect Trump is highly likely to make matters worse with tariffs. Notably, the USMCA deal has a joint review on July 1.

I will discuss USMCA in a separate post, but even if the war is settled, there is plenty of room for Trump to make matters worse elsewhere.

I think we know most of the numbers on the dice, even the likelihood of some question marks. However, we don’t know the outcome of the roll.

Related Posts

June 23, 2026: Oracle Cuts 21,000 Jobs to Fuel AI Push, Warns of Soaring Costs

Oracle’s head count drops 13% according to latest annual report. Many Risk Warnings

June 24, 2026: Trump’s Demand on SAVE Act Makes Passing Any New Reconciliation Bill Difficult

Trump insists the SAVE Act be part of a new reconciliation bill.

June 25, 2026: New Home Sales Drop Another 7.3 Percent, Builders Struggle with Rising Inventory

Sates are down. Inventory is high and rising, pressuring builders.

How long we can fire on a single cylinder remains to be seen.

Comments

Log in or sign up to join the conversation.