Photo by Scott Graham on Unsplash

💰 Oppenheimer: The Risk Calculus Has Changed

Peter Oppenheimer, Goldman Sachs’s chief global equity strategist and one of Wall Street’s most closely followed market voices, published a research note this past week that should focus the attention of every portfolio allocator. His argument is direct and increasingly difficult to dismiss: “the risk backdrop for equities has fundamentally changed.”

“After an unusually powerful post-pandemic rally that ranks among the strongest multi-year stretches in a century of market history, valuations across virtually every global region are elevated, equity risk premia have compressed to levels not seen since the months preceding the 2008 financial crisis, and leadership within the market is undergoing a dramatic, generational rotation. The near-term risk of a correction is rising—even if the probability of a full-blown bear market remains low.”

That final distinction matters enormously. We have noted for some time that the risks of a corrective period in the market are rising. Whether it is from excess valuations, speculation, or leverage, those risks are more prevalent than we have seen since the pandemic.

Let me be very clear: this is not a call to sell everything and retreat to cash. It is, however, a call to recalibrate expectations, reassess portfolio construction, and recognize that the margin of safety embedded in equity prices has eroded considerably, particularly in areas previously considered “value.” Understanding the difference between a corrective environment and a structural bear market is critical to positioning correctly in the months ahead.

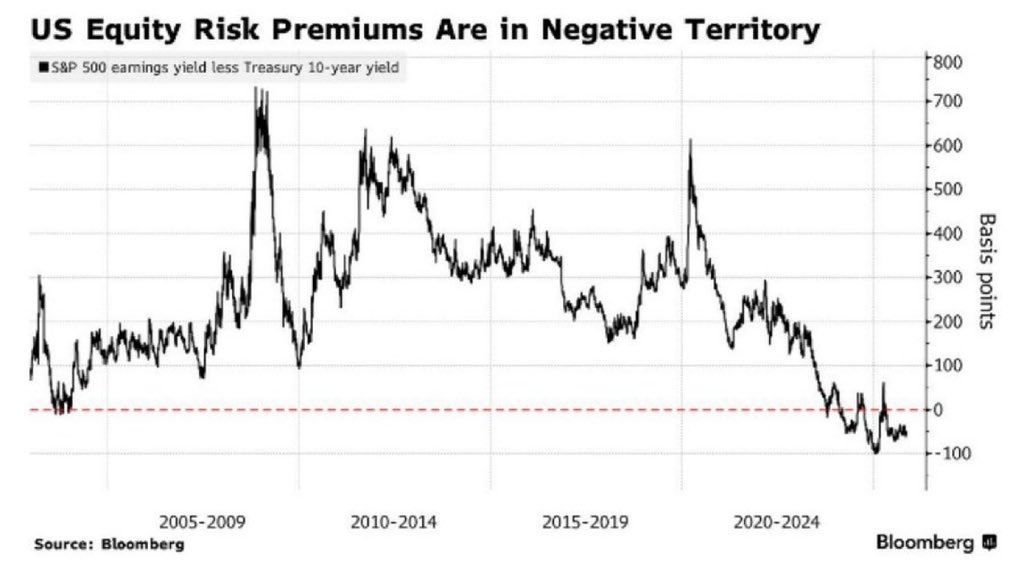

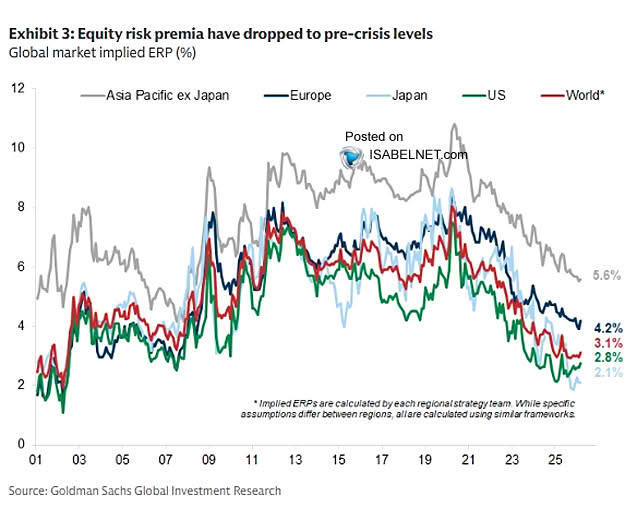

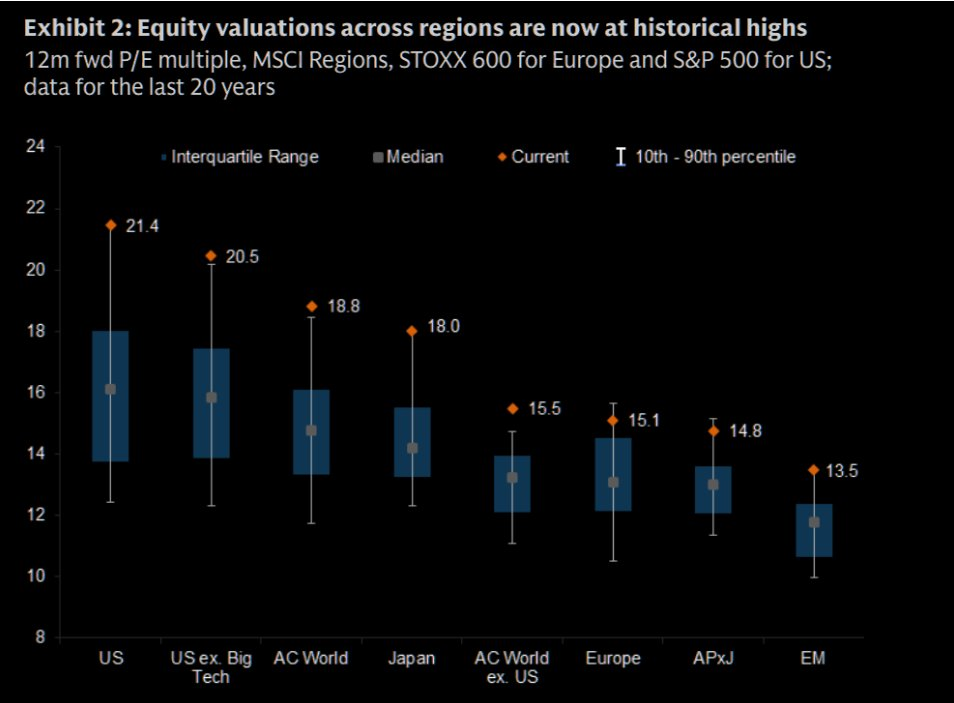

The epicenter of Oppenheimer’s thesis lies in the equity risk premium. The equity risk premium (ERP) can be calculated in different ways, but essentially, it is the incremental return investors demand for owning stocks relative to safer government bonds. The ERP is the market’s embedded compensation for uncertainty, and when it compresses to thin levels, it means investors are accepting equity-like volatility for bond-like expected returns. Today, and as Oppenheimer identifies, the equity risk premia across most markets have now fallen back to levels last observed in the run-up to the Great Financial Crisis.

As Oppenheimer noted, the ERP is not just exceptionally low in the U.S. but globally. The exceptionally low ERP is another reason that even though investors may “think” they are buying “value,” or at least markets that “seem” cheaper than the U.S., they really aren’t.

With the S&P 500’s forward earnings yield now near parity with the 10-year U.S. Treasury yield, and as Oppenheimer points out, the ERP in the US is among the lowest readings on record. For context, the long-run average ERP for the S&P 500 has historically ranged from 3% to 5%. Professor Aswath Damodaran of NYU Stern, widely regarded as the leading academic authority on ERP estimation, noted in his January 2025 data update that even assuming the ERP climbs back to 4.5%, above the 1960-2024 average but below the post-2008 norm, the implied fair value of the S&P 500 would sit roughly 12% below where the index traded at that time.

That gap has only widened since.

Crucially, a near-zero risk premium does not guarantee an imminent selloff. What it guarantees is that the market has almost no capacity to absorb negative surprises. As Oppenheimer stated, equities are now “more vulnerable to disappointments or shocks” driven by technology competition, geopolitical disruption, or a deteriorating growth-inflation mix. When investors are paid nothing extra to own stocks rather than Treasuries, even modest disappointments can trigger outsized repricing.

The Great Rotation: Technology’s Historic Reversal

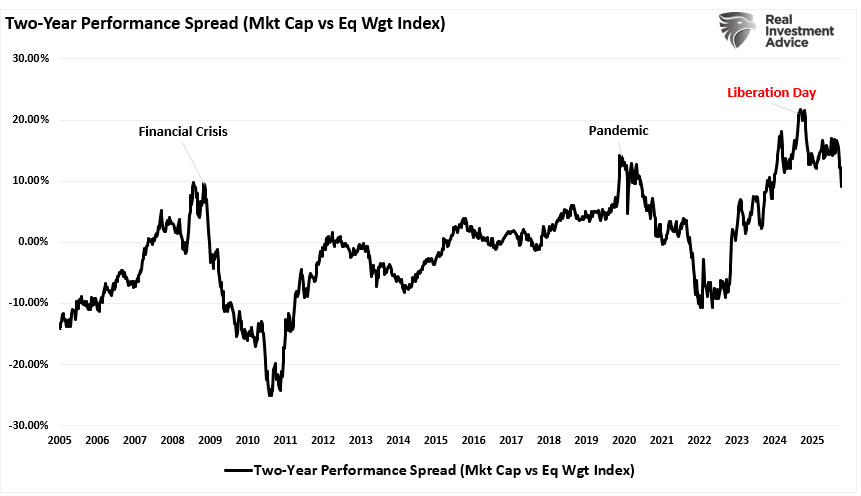

Over the past couple of months, we have discussed what Oppenheimer highlighted as one of the most significant sector-level developments in modern market history. That, of course, has been the massive rotation out of Technology stocks into the “value” sectors of Staples, Energy, Industrials, Materials, and Utilities. That rotation has led to one of the weakest relative periods for the market-cap-weighted index compared to the equal-weighted index since the Pandemic.

The narrative behind that rotation was driven by escalating anxiety over the returns on capital expenditures in artificial intelligence and fears that AI capabilities are disrupting existing software revenue streams faster than they are creating new ones. However, while that narrative lacks grounding in facts, it has been more of the “reflation” narrative that supported the rotation. That narrative assumes stronger economic growth, with little inflation, that keeps the Federal Reserve accommodative and improves earnings growth rates for the “asset-heavy“ companies involved in data center construction.

However, here is the problem.

The reversal has been so profound that U.S. asset-heavy industrial stocks now trade at a price-to-earnings premium over asset-light technology companies. Oppenheimer noted that cyclical stocks outperformed defensive names for 14 consecutive trading sessions in late 2025, the longest such streak in over 15 years. As shown, the current valuations for Industrials, Energy, Materials, Staples, and Utilities are now trading at historical extremes, with sector-level dispersion in the 99th percentile of historical norms.

Crucially, this rotation itself creates new vulnerabilities. Cyclical sectors, which are sensitive to the economic cycle, have now dramatically outperformed defensive sectors, and cyclicals trade at roughly the same valuation as defensives. That pricing dynamic leaves virtually no margin of safety if economic confidence wavers.

Investor Positioning: Tactical Adjustments for a Correction-Prone Market

The current conditions certainly suggest a potential for a corrective cycle in which value shifts back to growth due to valuation differentials. However, I agree with Oppenheimer’s view that the conditions needed for an extended bear market are largely absent. While there are currently some concerns about “private credit,” those issues are largely contained and relatively small compared to the “subprime credit issues” that led up to the financial crisis. There is also no impending risk of a severe recession, banking-sector collapse, or consumer withdrawal.

What is present is a market priced for perfection, leaving it fragile to anything less. In Oppenheimer’s framework, the current cycle sits in the “optimism phase” that follows the despair of a bear market, the hope of a rebound, and the growth phase driven by fundamentals. It is in these late-cycle periods that valuations stretch and corrections become more frequent. Oppenheimer’s historical analysis shows that most geopolitical shocks produce a median S&P 500 correction of roughly 6% over 18 days, followed by stabilization. Yes, it is painful but not catastrophic, and often provides attractive re-entry points. As Oppenheimer wrote,

“Correction risks are high, but any pullback should present a buying opportunity rather than the onset of a sustained downturn.”

So, what is Oppenheimer’s prescription for navigating the next phase of the market cycle? For investors seeking to align portfolios with a shifting risk landscape, it will be more critical and warrants consideration:

Rebalance Geographic Exposure. As shown below, the tailwinds of a weaker US Dollar have been hugely supportive of international and emerging markets. However, those markets are now exceptionally overvalued relative to their long-term averages. Rebalance exposures to reduce the risk of a stronger US dollar cycle.

Diversify Across Factors and Sectors. With technology’s relative premium compressing and cyclicals having already repriced sharply higher, the opportunity increasingly lies in quality-oriented, dividend-growing companies that can deliver returns through earnings and distributions rather than further multiple expansion.

Integrate High-Quality Fixed Income. For the first time in nearly two decades, bonds offer a genuinely competitive alternative to equities. With the equity risk premium near zero, investment-grade corporate bonds and intermediate-duration Treasuries provide attractive yields without requiring investors to bear the full downside risk of an equity selloff.

Maintain Disciplined Cash Reserves. With pullback risks elevated but bear market probabilities low, the optimal posture is not wholesale de-risking but rather ensuring sufficient dry powder to deploy opportunistically when the inevitable repricing arrives. This is especially prudent in a midterm election year where historical drawdowns tend to be front-loaded before November, with the subsequent six-month period historically delivering average S&P 500 returns of 14%.

Reduce Concentration Risk. Portfolios that are heavily concentrated in specific sectors or markets carry idiosyncratic risk that diversified approaches can mitigate without necessarily sacrificing upside participation.

Build Optionality Around Tail Risks. In a market priced for perfection, the cost of hedging tends to be lower than investors expect precisely because complacency suppresses implied volatility. Protective put strategies, collar structures, or systematic risk-management overlays can provide asymmetric payoff profiles that cushion drawdowns without requiring precise market timing.

The overarching thesis of these adjustments is a single imperative: reduce fragility. Like us, Oppenheimer’s discussion is not about fostering fear, but about preparation. The structural supports for this bull market remain intact. Earnings are growing, balance sheets are healthy, and monetary policy remains broadly accommodative. But the price investors are paying for those favorable conditions has left almost no margin for error.

The bottom line is not complicated. The post-pandemic rally has been extraordinary, but the risk-reward calculus has shifted. Valuations are rich, the cushion of the equity risk premium has largely evaporated, market leadership is rotating at historic speed, breadth is deteriorating beneath the surface, and the smart money is selling into strength. Investors who acknowledge this shift and position accordingly will be best prepared to navigate what comes next and capitalize on the buying opportunities that corrections inevitably create.

Comments

Log in or sign up to join the conversation.