One year ago today after the markets closed on 4/2/25, President Trump made an appearance in the Rose Garden of the White House. At the event, which he labeled as "liberation day," the President announced a slew of new reciprocal tariff rates on countries all around the globe. The tariff rates ranged from a baseline of 10% on all imports upwards of 100% on some specific countries such as China. Headed into the announcement, the S&P 500 (SPY) had already fallen 7.7% versus its 2/29/25 high, but over the next several days, the index fell another 12.4% through the 4/8/25 low (for a total decline from February's high to April's low of 18.9%). While equity markets took a big hit last spring, the S&P 500 made a full recovery by June and are now up solidly over the past year.

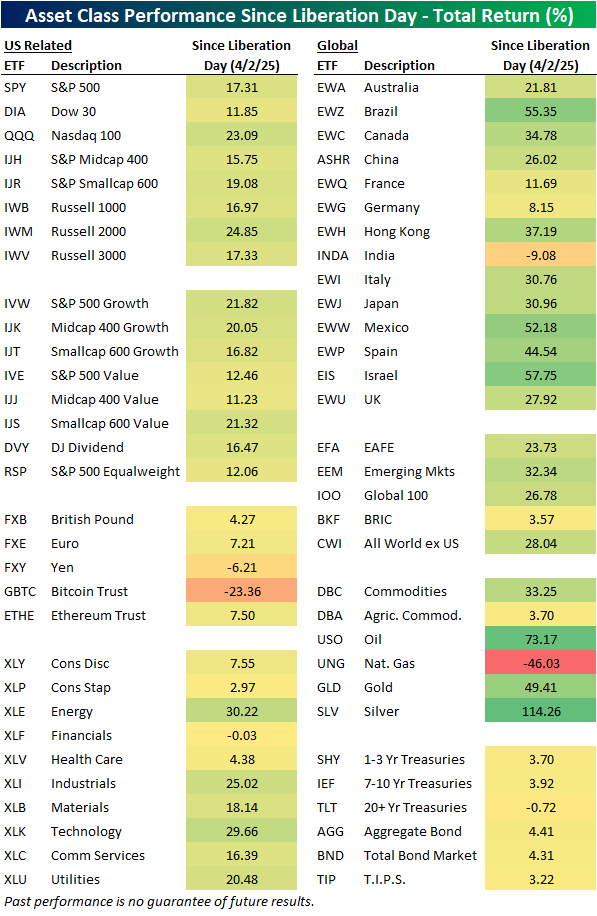

Below we show our asset class performance matrix with total returns for a range of ETFs since liberation day.

The biggest winners have been in the commodity space. Silver (SLV) is up 114% and that is even after falling 38% from its January high. Oil (USO) has been the next best performer with a 73% gain.

As for equities, the S&P 500 (SPY) has provided a 17.3% total return in the past year. The small cap indices like the S&P Smallcap 600 (IJR) and Russell 2,000 (IWM) have outperformed with gains of 19.1% and 24.9%, respectively. While small caps have provided larger total returns than large caps, large cap growth (IVW) and small cap value (IJS) are up similar degrees.

International equity ETFs have broadly outperformed US indices with the likes of Brazil (EWZ), Mexico (EWW), and Israel (EIS) all up well over 50%. Only one country ETF is lower in the past year: India (INDA) with a 9.1% decline. Germany (EWG) and France (EWQ) are the only two other country ETFs in our matrix to underperform the S&P 500.

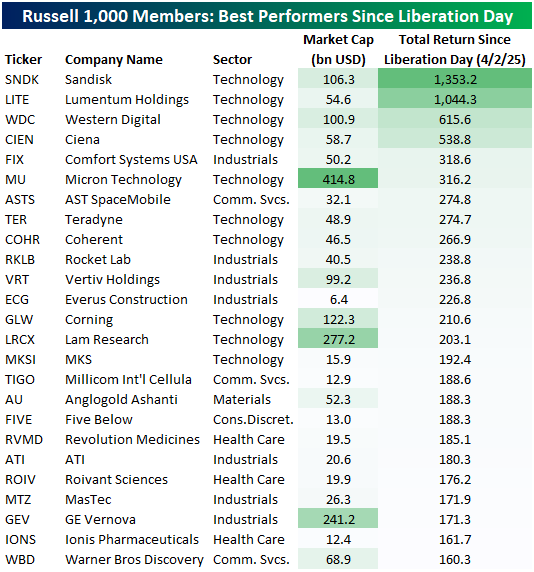

Moving back to look at the US, in the tables below we show the Russell 1,000 members that have provided the best and worst total returns over the past year. For the biggest winners, we have two 10-baggers in memory chip maker Sandisk (SNDK) and optical and photonic product maker Lumentum (LITE). SNDK is by far the biggest winner even of those two, up 1,353%. Not far behind SNDK and LITE are two more AI Infrastructure stocks: Western Digital (WDC) and Ciena (CIEN). Many of these top performing stocks are plays on AI buildouts, however, there are some other stocks from other parts of the market such as Warner Bros Discovery (WBD), GE Veranova (GEV), and Five Below (FIVE).

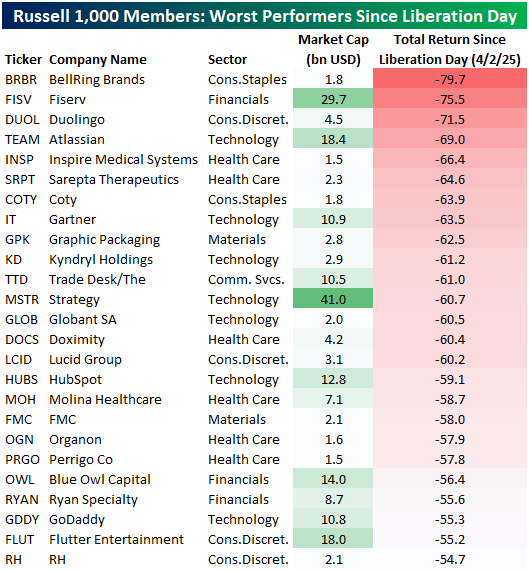

Turning over to the other end of the spectrum, the Russell 1,000 currently has 36 members that are down over 50% in the past year. Of those, the biggest loser is nutrition company BellRing Brands (BRBR), which has fallen close to 80%. Fintech firm Fiserv (FISV) and language learning company Duolingo (DUOL) are the only others down more than 70%.

Comments

Log in or sign up to join the conversation.