A gap between household expectations and economists forecasts is widening.

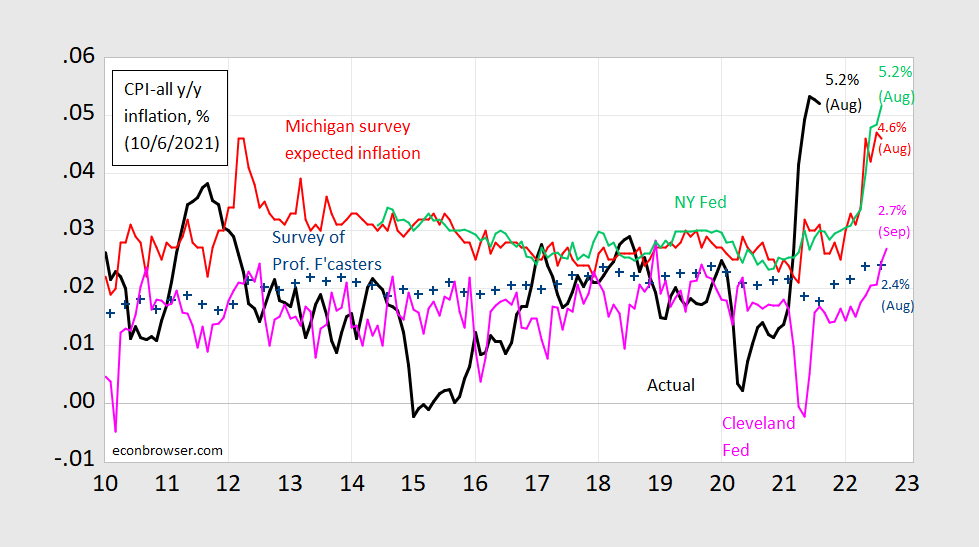

Figure 1: CPI inflation year-on-year (black), median expected from Survey of Professional Forecasters (blue +), median expected from Michigan Survey of Consumers (red), median from NY Fed Survey of Consumer Expectations (light green), forecast from Cleveland Fed (pink). Source: BLS, University of Michigan via FRED, Reuters, Philadelphia Fed Survey of Professional Forecasters, NY Fed, and Cleveland Fed.

All measures of expected inflation rose in August (and September for the Cleveland Fed measure). This continues the pattern exhibited remarked upon back in July. What is perhaps more interesting is the fact that the gap between household expectations and professional forecaster measures has widened (again). In November 2019, the gap between the Michigan Survey of Consumers and the Survey of Professional Forecasters measures was 0.7 percentage points. As of August, the gap was 2.2 percentage points. Another way of illustrating the difference in views is to note that 1 year ahead inflation has risen by 2.1 percentage points for the Michigan survey, and only by 0.3 percentage points for the Survey of Professional Forecasters (SPF).

Now, which one is more accurate? Over the period shown above, the Michigan survey exhibits an upward bias of 1.1 percentage points, statistically significantly different from zero. In comparison, the SPF is 0.2 percentage points upwardly bias, with the bias not significantly different from zero.

Rudd’s recent working paper(not an official Fed publication) has sparked a controversy over the role — both theoretical and empirical — of expectations in actual inflation behavior. Many of the arguments make sense to me, but I still think expectations still matter. The question (I think he’d agree) is how much. On the other hand Coibion et al. (2017) suggest that using household expectations (such as the Michigan survey) make estimates of the Phillips curve more stable, than using professional forecasts (e.g., SPF), and definitely than using full-information rational expectations (FIRE). (I’d like to add in firm expectations, e.g., as in the one compiled by Candia, Coibion, and Gorodnichenko, but those aren’t available online.)

As an aside, as noted in the Rudd working paper, most of the policy debates center on long-term inflation expectations (i.e., anchoring of expectations) whereas this discussion has focused on short term expectations).

Comments

Log in or sign up to join the conversation.