At the beginning of the week (9/27), Bruce Bartlett forwarded me a link to a remarkable document, entitled “Scoring the Trump Economic Plan: Trade, Regulatory, & Energy Policy Impacts” (strangely, dated 9/29), coauthored by Peter Navarro* and Wilbur Ross. I’m way behind the curve, and there have been numerous examinations of the document, so I will not discuss the entire paper. Rather I’ll focus on the following specific question: would renegotiating trade agreements and slapping tariffs on China, conjoined with the Trump fiscal policy, induce a drastic change employment and trade flows? The short answer — yes, but probably in a direction opposite of that posited by the authors.

Trade Flows under Exogenous Financial Capital Flows

There are (at least) two views of Donald Trump’s threats to impose sanctions on Mexico and China. The first is as a negotiating tactic, which will wrest concessions from these parties so that in the end, tariffs will not be imposed. The second is that these are real threats that will be carried out in a Trump presidency. I’ll take the second as given (since the US would not in my opinion have much basis for argument under the terms of the WTO).

If the 45% tariffs are imposed on China (presumably, as the Trump campaign website indicates, based on assertions of ongoing currency manipulation to undervalue the yuan,a dubious assertion), the most likely outcome is retaliation by China, of some sort. Hence, any sort of gain in jobs in import-competing industries would be mitigated by losses in exporting industries. In addition, it is likely that such sanctions would induce migration of production away from China and toward other East Asian countries where labor costs are still low (in other words, it would accelerate a process already underway). [For discussion of this single policy measure, see here] That means the impact on the overall US trade deficit with the rest of the world would be relatively small, and hence the impact on manufacturing jobs in the US would be small (or depending on the extent and nature of the retaliation, negative).

There are two important economic factors to remember when discussing this general issue of manufacturing. First, a lot of trade today is not in final goods, but rather intermediates. The canonical example is the i-phone; there is lots of US-China trade in the final products, but the value added actually comes from all over East Asia (and the US), so a heavy tariff on Chinese goods would not address the basic problem that the relevant labor costs are much lower abroad. Second, labor productivity in manufacturing has grown rapidly since the passage of NAFTA and the granting of PNTR to China, and so even if production comes back to the United States (as some has already), jobs would not necessarily.

Finally, it is unrealistic to think that other factors will remain unchanged. The partial equilibrium/elasticities approach to trade balances implicitly holds the trade balance…balanced. Or at least the trade deficit fixed. That partial equilibrium approach is, I think, unrealistic.

What Determines Trade Balances? Macro vs. Micro

Recall the balance of payments:

CA + FA + ORT ≡ 0

The current account (CA) is approximately the trade balance (or net exports) for the US. FA is financial capital flows. ORT is official reserve transactions. For the United States on a full float, ORT can be thought of as zero. Then to a first approximation CA and FA must be of equal and offsetting magnitudes. Which account drives the other depends on the model? Most macroeconomists (of most flavors, be it Keynesian, Classical, Humean) would likely place primary importance at business cycle frequencies on macro factors.

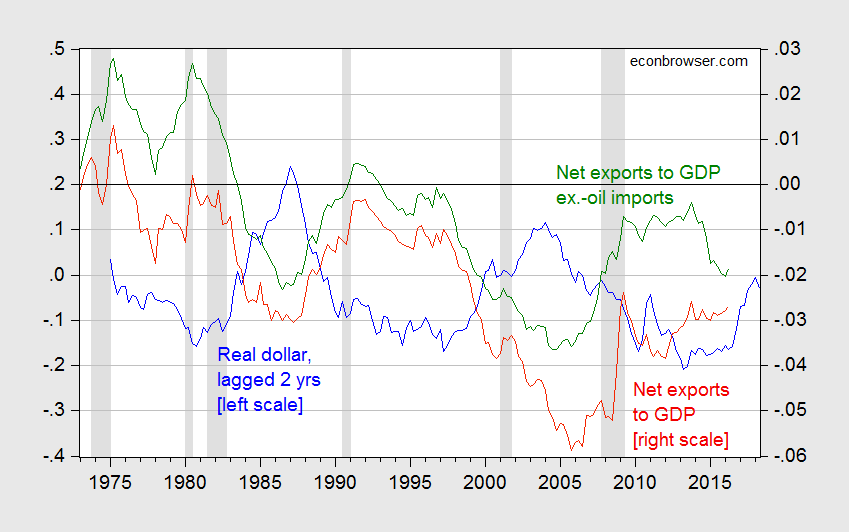

If the full Trump agenda is implemented, the likely outcome is (1) an elevated government budget deficit which would tend to offset other contractionary effects of policies, and thereby supporting imports, (2) strengthen the dollar thereby further increasing imports and diminishing US exports to the rest of the world. Figure 1 depicts dollar/net export correlations.

Figure 1: Log real value of US dollar lagged two years (blue, left scale), and net exports to GDP (red, right scale), and net exports to GDP ex.-oil imports (green, right scale). NBER defined recession dates shaded gray. Source: Federal Reserve, BEA (2016Q2 2nd release), NBER, and author’s calculations.

Of course, it is conceivable that Mexico and China would roll over and just accept wholesale renegotiation of the conditions under which China accession to the WTO occurred (in the latter case), and NAFTA (in the former). Alternatively, as has been pointed out, withdrawal from NAFTA could be relatively easily implemented without retaliation, but I do not see how this would have a noticeable impact on manufacturing employment, on its own.

Quantitative analysis of partial implementation of the overall Trump agenda, discussed here.

Comments

Log in or sign up to join the conversation.