When central bankers say they have more tools at their disposal to ward off a worsening recession, one tool is negative interest rates. With world economies seemly in free fall we cannot rule out this possibility no matter how radical it might seem. We have seen negative rates in Japan and Europe for the better part of a decade in the hope of reaching inflation targets. But it has yet to be tried in North America. Fed Chairman Powell and other FOMOC members have dismissed suggestions that negative rates are on the table. The Bank of Canada’s outgoing Governor Stephen Poloz was quite adamant that Canada not go there during his tenure despite worsening economic conditions.

Recent analysis by Kenneth Rogoff has provided some very compelling arguments in favor of negative rates, especially in the wake of COVID-19’s devastating effects. While the Federal Reserve is on track to backstop virtually every form of public and private debt, he asks “does that have to mean dispensing with market-based allocation mechanisms “such as interest rates? It appears that central banks are going to push interest rates cuts to the sidelines and instead concentrate on bond-buying programs once interest rates are permanently zero-bound. If the bond-buying efforts do not spark rapid recovery and it takes several years for the economy to return to 2019 levels, then negative interest rates may have to be introduced sooner than later.

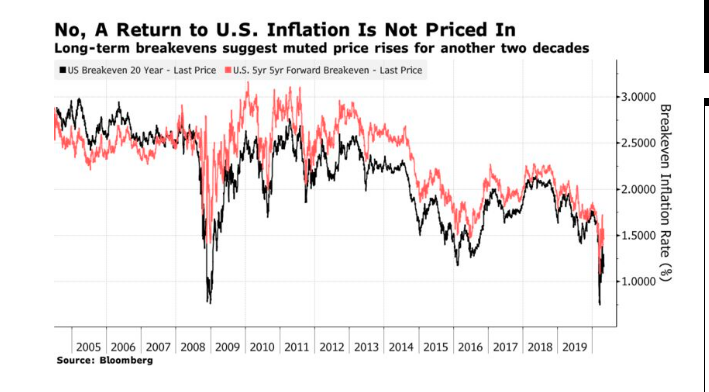

Trading in interest rate futures has already anticipated negative nominal rates. The market-implied probabilities of 3-month LIBOR rates are trading below minus 0.25% to 2021. Traders understand fully that the Fed is going to hold its funds at zero for at least 3 years and possibly beyond. In effect, the markets no longer believe that the Fed has the wherewithal to meet its inflation target of 2%. If anything, interest rate swaps (e.g. 5yr5yr forward breakeven) indicate that the CPI will barely hit 1% over the next decade and many traders expect outright deflation to take hold (see accompanying chart).

(Click on image to enlarge)

Rogoff argues the financial markets are trying to look beyond the current economic crisis. Traders are considering just how constrained the Fed will likely be without cutting rates below zero. In other words, bond-buying will not be enough to sustain growth in the future. Nominal rates have to fall further. As Rogoff puts it:

Given the steady downward drift in global real interest rates, the difficulties in raising expected inflation, the ineffectiveness of quasi-fiscal instruments at the zero bound, and ultimately the importance to central bank independence of having an instrument of unilateral control, create a strong imperative for proactively preparing now for a negative interest rate world that is perhaps inevitable.

As expected, conventional thinking within the economics profession is that negative rates are harmful and must be avoided. Of course, the banking community detests negative interest, although they need not destroy bank profits. It appears, however, that Interest rate traders are looking much further down the road and are staking out positions that rates are going negative.

Comments

Log in or sign up to join the conversation.