Micron left little doubt that the supply-demand equation is grossly out of balance for AI memory chips, benefiting semiconductor companies. In its latest earnings report, Micron reported astronomical growth with revenue of $41.46 billion, up a stunning 346% year over year and 74% versus the prior quarter. Its adjusted EPS of $25.11 beat the $20.28 consensus by nearly 25%, extending Micron’s streak of beating estimates to seven consecutive quarters. Its gross margin hit 84.9%, more than double the year-ago level.

Data center revenue reached $25 billion in the quarter, driven by insatiable demand for high-bandwidth memory (HBM) chips, which power Nvidia’s AI GPU stacks. HBM products remain fully booked, and management said the supply shortage is expected to continue well beyond 2027.

Micron’s forward guidance was equally stunning. To wit, Micron guided Q4 revenue of $50 billion, well above the $43 billion Wall Street consensus. They expect gross margins of approximately 86% and EPS of $31. Free cash flow is expected to exceed $30 billion in Q4 alone. Micron shares jumped nearly 20% in after-hours trading, and the strong results indicate that the AI memory supercycle is not slowing down. Per Micron’s CEO, Sanjay Mehrotra:

Micron’s record fiscal Q3 financial results and even stronger outlook for Q4 reflect the strategic value of memory in the AI era.

What To Watch Today

Earnings

No earnings releases today.

Economy

Market Trading Update

Yesterday, we previewed Micron’s (MU) earnings, which, as noted above, were stellar, leading to a resurgence in the semiconductor rally on Thursday. However, yesterday, we did something that, on the surface, doesn’t make sense. In our Rotation Factor model, we switched from value to growth. Let me walk you through it.

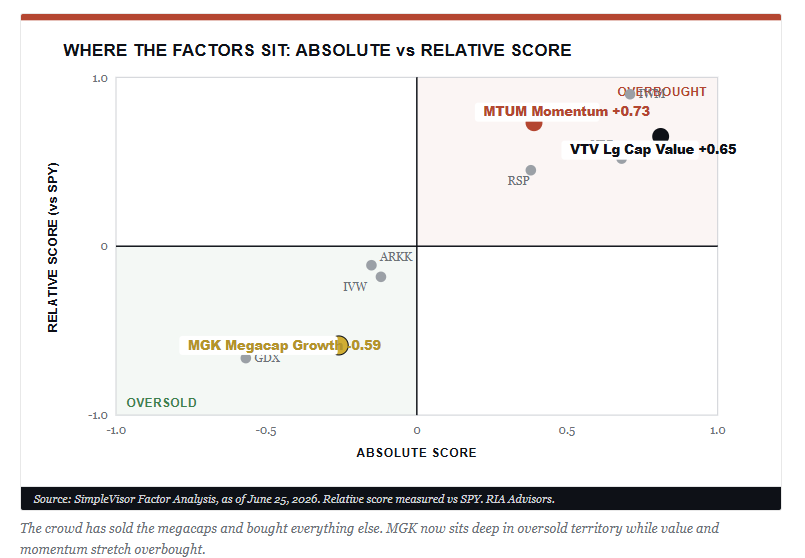

First, yesterday’s market action told you nothing about what’s moving underneath the surface, which in turn tells you a lot about where money is moving. Notably, we are into the end of the quarter rebalancing window, so some of yesterday’s action is certainly attributable to that. However, look at where the factors sit on our SimpleVisor screen. Mega-cap growth (MGK) has fallen to a relative score of -0.59 against the index, the most oversold pocket of the large-cap complex. Large-cap value reads +0.65 and momentum +0.73, both stretched. This isn’t subtle. The crowd has spent six months selling the megacaps and chasing everything else.

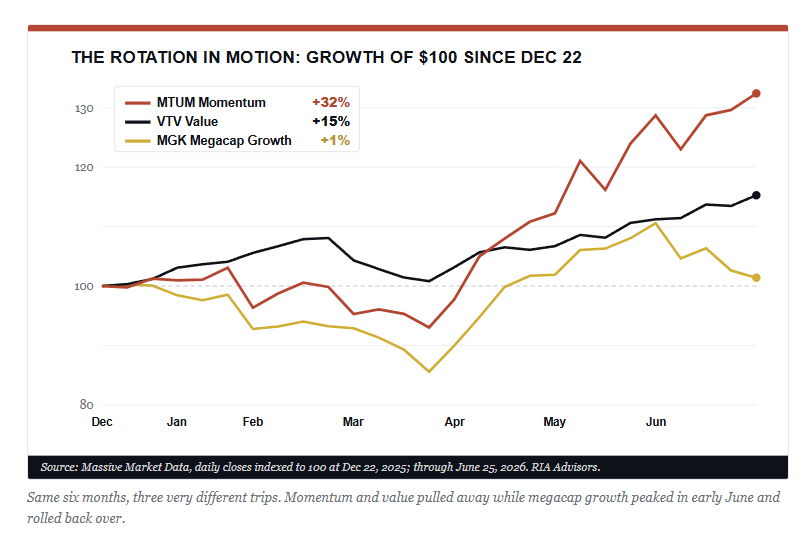

The performance gap confirms it. Since late December, momentum has run up more than 30%, value is up around 15%, and mega-cap growth has gone basically nowhere, at just over 1%. A big slice of that “value” win is really a semiconductor trade in disguise. Micron screens as VALUE in most large-cap value indices because of its low multiple on peak memory earnings, and it has gone parabolic. As Bob Farrell’s Rule #4 reminds us, exponential moves usually run further than you think, but they don’t correct by going sideways.

That brings us to the setup. The money leaving the megacaps has crowded into the value and momentum chase, and the semiconductor names riding inside the value indices are doing the heavy lifting. Meanwhile, the largest, most profitable companies in the market are washed out and unloved heading into the one event that resets the narrative. Earnings.

Q2 reporting season starts in earnest in mid-July. The MGK names report into low expectations and oversold positioning, exactly the conditions that produce mean-reversion rallies. As we’ve flagged in recent commentary, the narrowing into the momentum and semiconductor trade was getting stretched, and the other side of that trade is now the oversold megacaps. I’m not calling a top on Micron or the memory cycle. The point is narrower. The risk and reward have flipped, with oversold quality becoming an earnings catalyst that looks better than overbought momentum into the same catalyst.

Make no mistake, oversold can get more oversold, and megacap growth is fading for a reason as the market digests the AI capital-spending bill. That’s the honest counter. But “oversold plus a catalyst plus washed-out positioning” is a very different bet than “oversold” sitting by itself. We’re watching the early-July megacap prints for signs of a turn.

When Will Gasoline Catch Down To Crude?

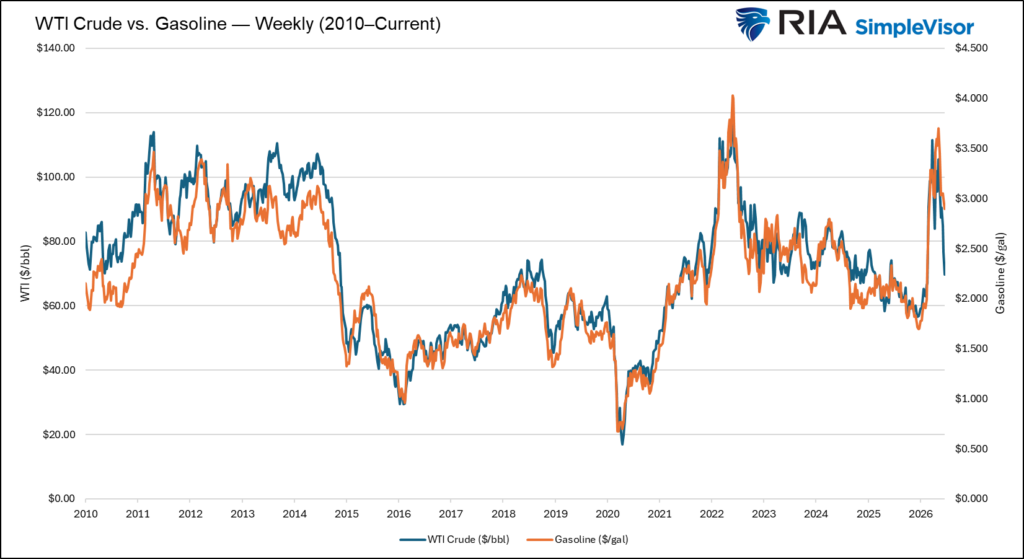

Crude oil has fallen sharply on optimism surrounding a US-Iran peace deal. As shown below, the price of crude oil is now only a few dollars higher than where it stood on the eve of the conflict. However, gasoline prices have not kept pace. Understanding the gap and when it will close is very important for tracking the inflation relief trade.

The divergence comes down to three factors.

Refinery margins: The gap between crude oil prices and refined product prices, which include gasoline, jet fuel, diesel, and heating oil, is known as the crack spread. The crack spread, and refiners’ profit margins are well correlated. At times, like today, when crude falls sharply, refiners don’t immediately pass the full decline through to refined products. They may absorb a portion as margin recovery, particularly if crack spreads were compressed during the disruption period.

Seasonal demand: Gasoline futures are responding to their own supply-and-demand dynamics, independent of crude. We are entering the period of maximum gasoline consumption in the US. Structural demand for gasoline is high, creating a natural floor under gasoline prices that crude lacks.

Hormuz-specific dynamic: The disruption to the Strait hit refined products particularly hard because Persian Gulf exporters ship finished gasoline, diesel, and jet fuel, not just crude. As peace deal optimism normalizes, crude flows will normalize quickly, but refined-product logistics take longer to unwind, meaning gasoline will remain physically tighter than crude even as the geopolitical premium deflates.

The disinflationary impulse from falling crude oil prices will flow through to gasoline futures and, eventually, to pump prices. The inflation relief is coming.

Tweet of the Day

Comments

Log in or sign up to join the conversation.