Summary:

Bonds remain in a major compression regime. Our bias is for a breakdown lower, but short-term disinflationary trends likely keep things compressing for a while longer. The USD continues to hold its breakout level, but has so far failed to move much. The weight of evidence still supports a bullish breakout in SPX, with breadth broadening out. Though a few key internals say otherwise and need to be watched closely. 3m SOFRs are set up for a positioning fade tactical long. Semis are at an inflection point. And Meta (META)is trading close to its cheapest levels in history.

MO Portfolio & Trades

1. The portfolio ended last week down -70bps, bringing year-to-date returns to +43.3%, below our YTD NAV high of +61%.

Current positioning: All cash as we recently did a portfolio reset but we’ll be repositioning back into biotech (XBI, ARKG and select names), cyber security, energy / crude oil, and select Mag7 (META, NVDA).

2. Bonds continue their compression on the monthly tape with BB width at its tightest range since 2018. Compression regimes precede big trends but are directionally agnostic, though our bias is for a breakout to the downside (more on this below).

3. Bonds are testing key levels of support. Yesterday’s weak CPI surprise provided only a temporary boost before reversing and closing the day unchanged. There’s no clear short entry yet, as it’s oversold against its 20dma. We’re continuing to keep a close eye on this as I expect things are setting up for a bearish breakdown come end of summer, once this short-term disinflationary impulse runs its course.

4. There is a tactical long in the front end, 3m SOFRs. Speculative positioning is record short. I’ve laid out why I’m bullish rates (bearish bonds) here, but I think we’re in a 1-2 month window where inflation and growth surprise to the downside, making this a tradeable setup. I’m considering putting in a buy stop above recent highs to see if the market can pull us in long.

5. But again, this is a short-term tactical trade at best. The best central banker (2yr yields) says the Fed’s next move will be a hike.

6. Our Leading Yield Indicator continues diverging higher.

7. DXY continues to hold its breakout / support level. Not much to say here. We’re willing to play it in either direction; long on a move above recent highs and short on a bull trap breakdown.

8. Our bias for risk assets continues to be bullish. SPX is still trading in a 2 month sideways range, within a Bull Quiet regime.

9. Breadth continues to expand putting the odds strongly in favor of a bullish breakout. Notice the opposing breadth picture that preceded the March selloff, where breadth diverged lower compared to today’s where its diverging higher.

10. However, one thing we’re closely monitoring is the negative divergence in a few key internals, such as credit (green line) and Qs vs SPY (tan line). I suspect we’ll see both bottom out and reverse soon. If not, I’d be hesitant to buy any breakout in SPX as it’d likely be a trap.

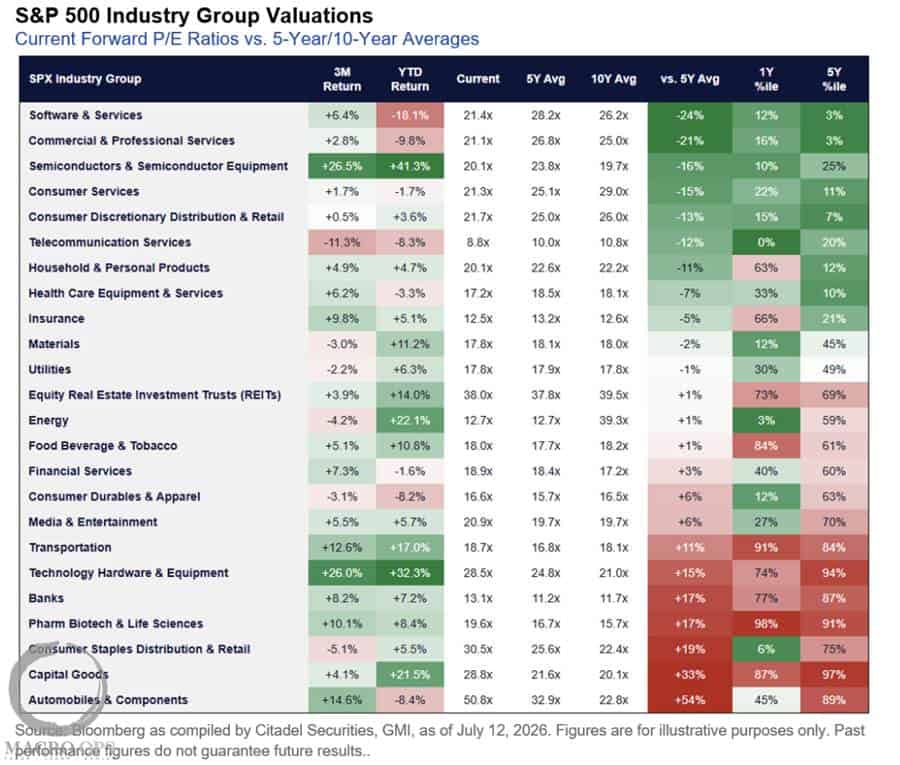

11. From Citadel Securities: “Despite the S&P 500 trading within 1% of all-time highs, S&P 500 Information Technology, the Nasdaq 100, and even the S&P 500 Semiconductor industry all trade below their respective 10-year average forward P/E multiples.

Some of the market’s highest-quality growth companies are entering earnings with valuation support rather than valuation headwinds.”

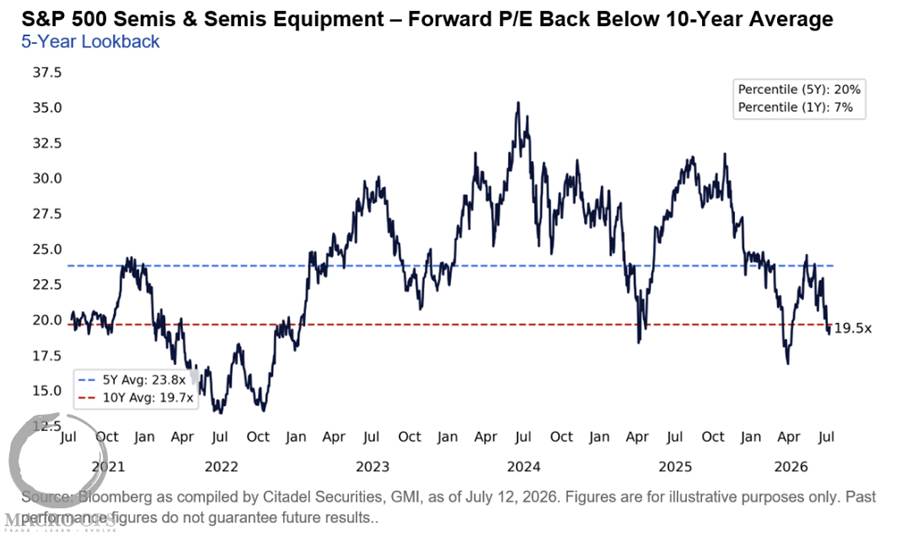

12. Semi’s forward PE is back below their 10yr average. Admittedly, this is on the back of elevated earnings expectations (chart via Citadel).

13. Speaking of semis, RenMacLLC recently pointed out that nearly 87% of semi names are oversold.

14. The memory ETF DRAM is bouncing off its lower band, offering a decent spot to play for a tactical long with a tight stop, which we might do in small size.

15. Semis should continue to perform well as long as actual CAPEX keeps pace with expectations. 3Fourteen Research shows that MAG 7 CAPEX estimates are approaching 3% of GDP. These are insanely large numbers.

16. META’s valuation recently dropped to its second lowest level ever — the all-time low marking the end of its 22’ bear trend. The key catalyst is monetizing its massive compute base: if Meta can rent out spare AI capacity without slowing its own roadmap, investors stop treating capex as vanished cash flow. That reframe alone could re-rate the multiple.

Comments

Log in or sign up to join the conversation.