The CPI surprised on the upside by 10 bps relative to Bloomberg consensus (also higher vs. Cleveland Fed nowcasts). How did financial markets respond?

Photo by Sara Kurfeß on Unsplash

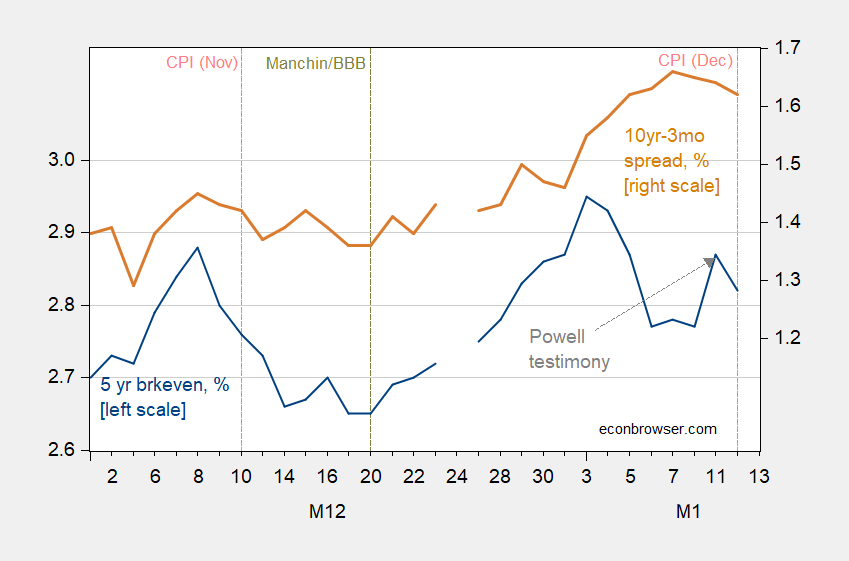

The 5 year breakeven (unadjusted for inflation risk, liquidity premia) fell 5 bps.

(Click on image to enlarge)

Figure 1: Five year inflation breakeven calculated as 5 year Treasury yield minus TIPS yield (blue, left scale), and Ten year-three month term spread (brown, right scale), both in %. Source: Federal Reserve Board via FRED, and author’s calculations.

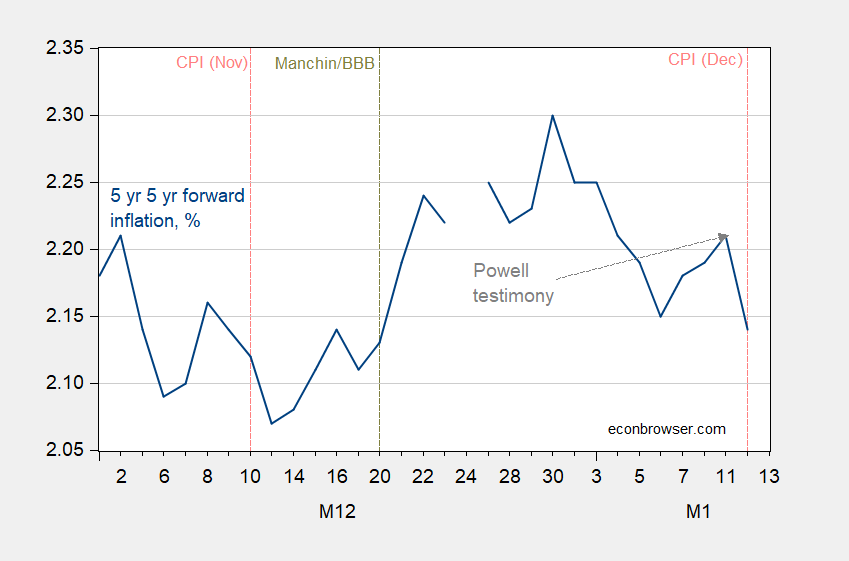

Not much of an effect on the term spread. The 5 year 5 year forward expected inflation fell as well.

(Click on image to enlarge)

Figure 1: Five year five year inflation forward in % (blue). Source: Federal Reserve Board via FRED, author’s calculations.

Longer term inflation expectations seem well anchored, pretty much the same as mid-January 2021.

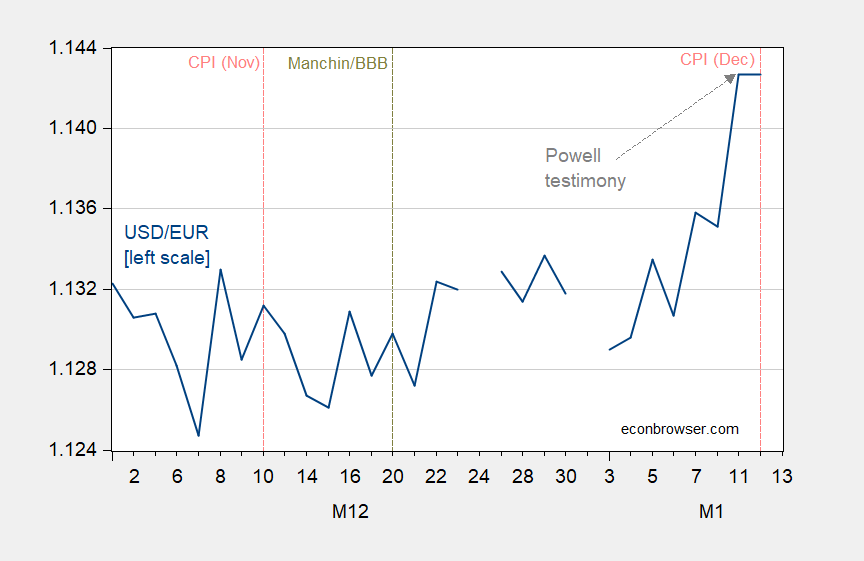

Finally, in a sticky price world where there’s a Taylor rule in place, one would’ve expected a dollar appreciation on the inflation surprise (as in Clarida (2007)). Instead, the dollar stayed flat.

(Click on image to enlarge)

Figure 3: US dollar/euro exchange rate (blue), up is dollar depreciation. Source: Federal Reserve Board via FRED, Pacific Exchange Services.

To me, this means the market was not particularly surprised by the CPI number, notwithstanding the headlines about record y/y inflation. That makes sense to me as soon as one realizes that month-on-month inflation continued to fall in December.

Comments

Log in or sign up to join the conversation.