Interestingly, if implied forwards are to be believed, the Fed won’t be raising rates too fast.

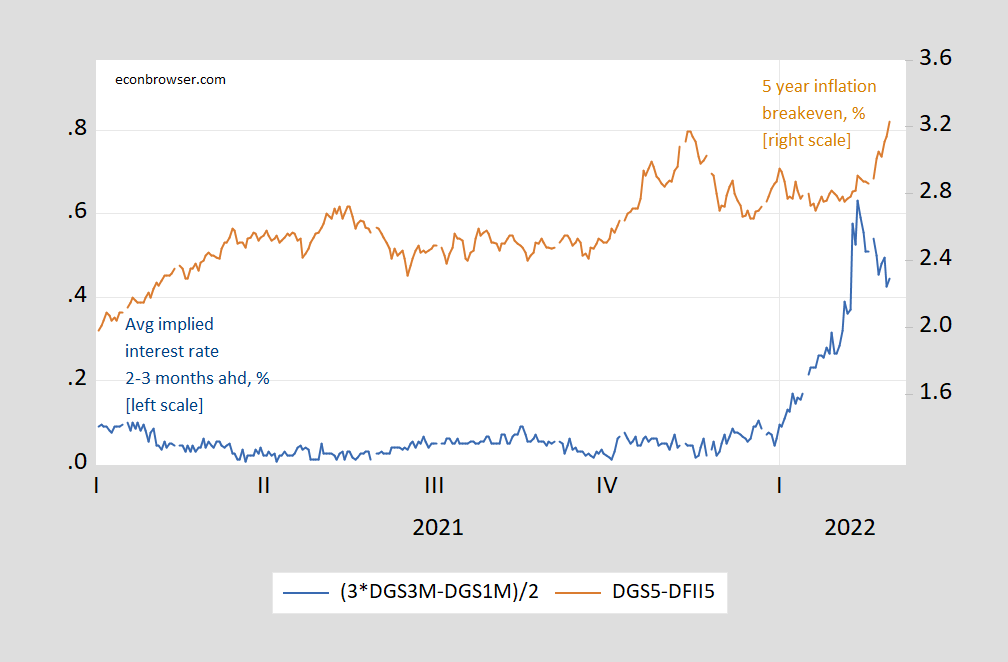

First, forwards as the 5 year inflation break even moves up.

Figure 1: Implied Treasury yield 2-3 months ahead, % (blue, left scale), and 5 year inflation breakeven, calculated as simple difference between Treasury and TIPS yield (brown, right scale). Source: Treasury via FRED, and author’s calculations.

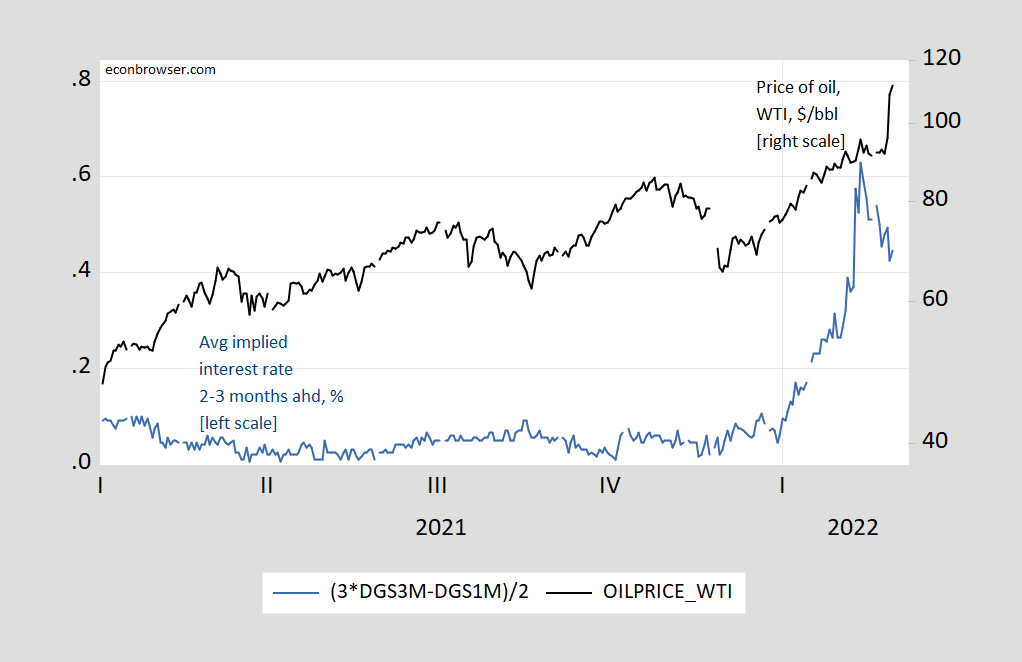

Second, forwards as the price of oil (WTI) rises.

Figure 2: Implied Treasury yield 2-3 months ahead, % (blue, left scale), and price of oil, WTI, $/bbl (black, right log scale). 3/1 and 3/2 observations are near month futures. Source: Treasury, EIA via FRED, NYMEX, and author’s calculations.

Of course, the calculation of forwards abstracts from any term premia, and the the calculation of inflation breakeven abstracts from term and liquidity premia (see this post).

Update, March 2, 6pm Pacific:

The CME Fed Watch utility shows how the probability of a 25 bps increase fell, as the probability of a 50 bps increase rose to a peak at February 10th, and then fell — even before the Russian invasion of Ukraine.

Source: CME FedWatch, accessed 3/2/2022.

Comments

Log in or sign up to join the conversation.