An absence of sellers ahead of the Fed's (likely) rate hike increase, as well as a Tax Bill likely devoid of an FIFO capital gains tax sales provision, is (as projected) allowing the Senior Indexes to step up to new highs early in this trading week.

That was anticipated and we sure didn't fight it while noting that persistent discussions in the financial press about whether this is the 'last days' of the overall move and so on, actually mitigate against that being the case.

Now whether or not this can stair-step into 2018 and persist with the rally, well, that's a far different question. And it's one we suspect will not fulfill a slew of presumptions about developing growth persisting with a tightening of monetary policy. Up to now we thought overall rate levels were not at all a hindrance to the markets, nor an impediment to business activity.

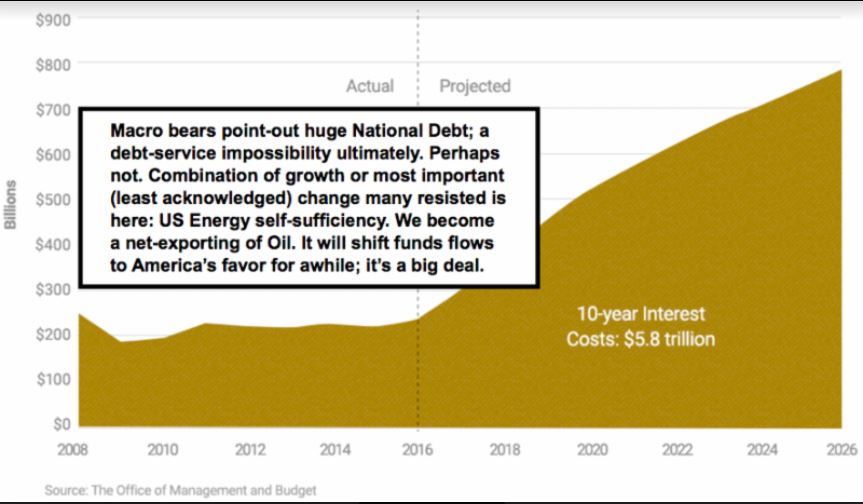

Eventually we get to a point where rates do start to impact US debt service (along with an awareness of the overall indebtedness); but that's not at the forefront of concern yet either. Neither are geopolitical events momentarily, although that can change sharply at any moment.

The stability of this market is a bit of a facade however. Generally, with the prospect of FIFO being absent a Tax Bill when it emerges later this week, I suspect this is as simple as investors relieved (as we've said for days now) that they can presumably just ride the move (including small shakeouts) a bit longer, and nurse their holdings until they settle within a new tax year.

Beyond the New Year it becomes tenuous (and you might see a bit of this reflected the last two sessions of the month when settlements occur within the next tax year) at best; and downright risky at worst. However, even the first shakeout in the New Year should be contained (barring shocks again of course) because then institutions can breathe their own variation of a sigh-of-relief, anxious for annual seasonal reinvestment funds to arrive.

Bottom line: it may be unexciting (persistent upside without excitement is fine); although if this unfolds into a blow-off (stepper uninterrupted angle of attack on the charts); that's the ultimate bearish alternative, even if just for an overall correction that 'sort of' eluded the market his year.

I say 'sort of' because we did get the 'rotational sector corrections' for more than the couple weeks last month; but really since mid-Summer. That kept the bears at bay; was the forecast pattern ideal; and now you have mostly a broad sector advance (aside healthcare and such) helped by tech and of course Oil. As that persists, and providing there's no 'real' disappointment in the Tax Bill, we should see this hold together for now; and absorb a Fed hike; unless they stun markets by raising a half point rather than a smaller quarter-point increment.

Also it's Quarterly Expiration Week; so the open interest gets whittle-down every day and probably is a favorable factor for the moment as well.

In sum: I'm generally contending this is 'sort of' late-stage activity for now; but not necessarily on the edge-of-an abyss or anything like some suggest without considering the structure that allows this.

Also what I'm addressing has absolutely nothing to do with the surrounding frenzy with Bitcoin; which of course went up initially since shorts were not permitted; although that will change in time. I do see it as mania but mania can continue (with shakeouts such as you had late today) until tulip seeds run out; and that can be some time.

For the stock market, I see tumult in the near future; but the tenacious rise persisting for now; not necessarily any historic secular high, yet.

Comments

Log in or sign up to join the conversation.