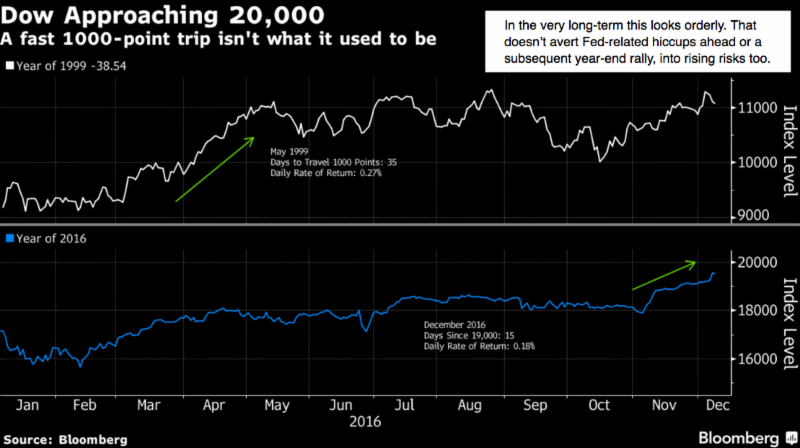

Extended bouts of euphoria are actually tamer than appreciated. That is not to suggest that we have to advance immediately upon DJIA 20,000 but it does reflect how there's an orderly sense to the ongoing rotation. It's been visible simply by noting the market's ability to forge ahead absent a continuous oil firming. On Friday oil did gain a bit; aiding the S&P and DJIA in achieving ever-higher levels.

We haven't and still don't believe that just because it's spiky and seriously ahead of valuation metrics (any type of fundamental assessment aside of course, wishful thinking), it has to reverse aside periodic refreshing pauses to refresh. Now sure, I hear the comparisons with 1999 or even 1929 out there; and I understand the parabola they're looking at. Just following what I have said for a month now; and that's the belief that 'everything changed or is at least perceived to be changing' for the better as far as business.

Of course there's going to be a day-of-reckoning; and a short-term top of some consequence is in the offing over the course of the next three weeks or so (as we approach the point where trades can settle in a new tax year). I suspect next week could see some pause or hiccup related to the FOMC, and perhaps their statement more so than just the hike they implement. I also suspect that will be contained (should there be selling on that) and to the chagrin of any wannabe bears out there, the market catches itself in fine fashion, and trucks ahead as the blizzard of money comes back in.

Now again, this is not to say I'm entirely comfortable with everything that our new President is setting up.

For now, with clear understanding of how divided society is about things, I am focused on the business and market implications of perceived policies as regard taxes, regulations and trade. I am not saying all are endorsed or anything like that. And I'm not saying there won't be monetary, currency or debt service issues (there will be); nor am I suggesting all that is being done is somehow ideal for society. I simply projected (even weeks before the vote) that it would be well received and thrust the market much higher (and not necessarily this high; just that we stayed bullish seeing how it all unfolded).

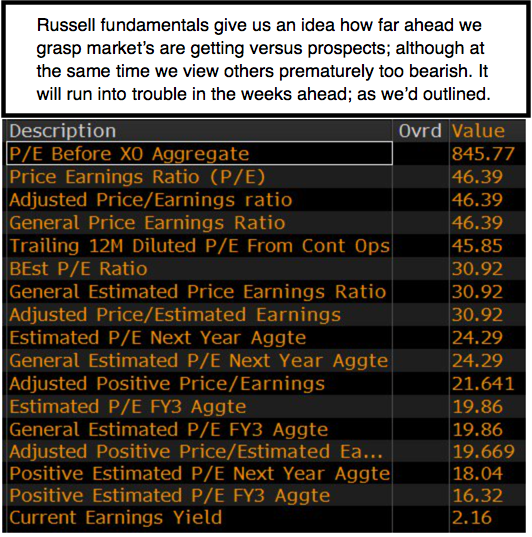

The important part is recognizing this was a potent trend, and not leaning heavily against it. That remains true now, although of course we see this as ludicrous based on logical fundamental anticipations for the quarters just ahead (though business has perked-up in some sectors just from the greater optimism). We included the 'table' referencing the Russell to show we're not oblivious to the disconnect between markets and fundamentals.

The difference is two things from the disconnect with a higher market; say at mid-July (just as or after the President-Elect was a seller of his stocks): 1) the Nation was entering a new recession and increased stagflation as prevailed, so the market, even though eroding for months, was way high in the way of the buybacks and the Fed policy assist. This is not the case now as frustration has become euphoric optimism about industrial base recovery (and yes, perhaps too much so at this rate of price appreciation for equities).

And then there is: 2) we're got sector rotation beyond what's recognized by virtue of 'multiples' or anything that can be projected for a company or for that matter a sector. It's 'price and sector weighting'. Mutual funds and others who now recognize the 'capital intensive' industrial transformation they weren't prepared for (because they didn't think he could win, so thus it would most likely have been business as usual with a little better policy on trade perhaps).. well, those money managers now have to give greater 'weight' to all heavy equipment, telephony, communications, infrastructure and other areas, which took a backseat to technology and healthcare for so many years.

Clearing the air?

And incidentally, the meeting of President-Elect Trump and Ivanka, at Trump Tower...with Leonardo DiCaprio...really should comfort those who presume we'll all be underwater with most environmental achievements reversed. How about just the opposite perhaps. At the end of the meeting; the head of DiCaprio's Foundation, focused on fighting climate change said: "We look forward to continuing the (Trump) conversation with the Administration as we work to stop the dangerous march of climate change, while putting millions of people to work at the same time".

But Trump designated the Oklahoma AG as Environmental head; and he's a climate change denier. So we'll see. However, majority views on all sides of the argument are in favor of clean air and water, so maybe this combines with a similar end result. Humanity can certainly cross their fingers a bit.

This may not be just lip-service. After all while Trump wants an explosive growth and jobs story;,he also is in favor of a clean environment. On the other hand he knows the pushback that's coming against reviving energy industries; so the Administration will need an 'environmental protection' or similar plan to control the situation; and perhaps there's therefore this odd (but conceivably welcomed) fellowship between Trump and DiCaprio. For sure there's a view that the EPA is inept and not meeting their mandate as it is... so who knows, the surprise may be if this is not 'Alice in Wonderland' but shaping a plan (such as the gasoline blending issue) for progress.

They met for 90 minutes (which is more than a courtesy greeting) .. and comments thereafter boiled down to this:"Today, the President-elect and his advisors were presented a framework - developed in consultation with leading voices in the fields of economics and environmentalism - detailing how to unleash a major economic revival across the United States that is centered on investments in sustainable infrastructure."

The focus was how to create millions of secure, American jobs in construction and operation of commercial and residential, clean, renewable energy generation. So if we get an EPA that doesn't run amok; but gets the job done; maybe that's not merely 'hoping for the best with Trump', but actually an improvement.

Bottom line

That shift in equities, and sector 'weighting', isn't reflected in PE trailing or forward multiples based on what's out there now. Rather it is seen largely in new concentrations in those sectors, which generally were laggards in Indexes, but are nevertheless huge capitalization companies.

Now and then, they rotate funds back into some technology stocks; or oil bubbles up a bit (they're having meetings within OPEC and NOPEC trying to apportion what was loosely agreed to in Vienna), while Europe calms as they realize Italy wasn't going to have an immediate bank disaster (as we suggested would be sidestepped and despite the Moody's downgrade), and the accomodative ECB didn't really matter.

We expect bouts of profit-taking but generally this defies normal logic as we have said before and say again. It's a major national transition and it is based on hopes that it becomes a transformation. Even if successful to the nth degree you'll get setbacks (typical of the first year of a new term of a new President). And if not successful; then yes you're building a bubble of colossal proportions. Perhaps both (meaning like Reagan; you go up on hopes and promise; then retrench significantly, then advance anew). Stay tuned as there's a lot more coming; but not an immediate plunge in absence of an exogenous event (and there is a slight risk should we see an intervention in Syria for instance, though that would be foolhardy at this stage since the Russians and their pals almost wrapped Aleppo up).

On a daily basis we have advocated staying long and still do.

Comments

Log in or sign up to join the conversation.