| Complacency dominates in multiple, not particularly surprising ways. That relates both to our own expectations for third Quarter re-balancing holding up the S&P, but also the greater optimism for 'tax-reform' actually forthcoming. At Friday's end, we got record highs closes for the S&P and even the DJIA, all is suspected likely to cap off this historically calm but firm September.

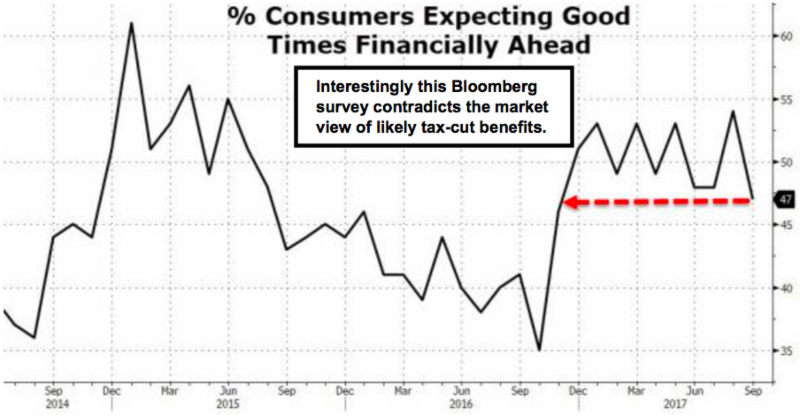

So, yes, the corporate sector and private business (including Sub-S and LLC grandfathered taxpayers) are likely to be prime beneficiaries in a probable lower 2018 tax environment. Nevertheless markets are absolutely focused on having these moves finally codified in a radically redrawn tax policy, that really should help small business at least as much as big companies, while bringing improved job prospects to many who already pay little or virtually nothing in taxes (who should look forward to that opportunity ahead). There has actually been a 'pop' in President Trump's popularity as these plans get rolled out, perhaps as more people see the benefit of tax simplification.

During my extended travel in Europe, we generally held a neutral view that was on guard for decline, but unwilling to overtly short the stock market with a degree of cynicism towards the trading and hedge crowd doing just that. It is surely incredible how docile the averages were during September; and of course the pundit consensus expects nothing disruptive to occur in October.

Maybe that's enough reason to be concerned: nobody's worried. Reality has a way of surfacing when many believe the 'black swans' are all back-burner items, which they really are not. Higher Oil prices, incidentally, have been an associated occurrence with the higher S&P, as I've suggested would occur, versus the old-fashioned conventional wisdom of higher oil dissuading new consumer spending and so on. It may be diminished but not for that reason.

In fact, the Saudis finally have a reason to worry less about over-producing, and indeed that's why their expressed desire to contain OPEC production... it's ARAMCO's IPO expected to hit London and New York later next year. In a nutshell, a higher Oil price (like 60 in their dreams) would be ideal to float that IPO (about 5% probably with the rest retained by that State) strongly. If that's really underpinning our projected move up from the lower 40's in Oil, it might be a characteristic that predominates during much of the year ahead.  The Saudis are not unaware that the world is moving towards alternative or hybrid power for transportation and California's proposal to deny sale of all combustion auto's by 2040 is indicative of the trend that is slowly unfolding. Of course to do that you'll need radically improved batteries and more.

|

Market Briefing For Monday, Oct. 2

Complacency dominates in multiple, not particularly surprising ways. That relates both to our own expectations for third Quarter re-balancing holding up the S&P, but also the greater optimism for 'tax-reform' actually forthcoming.

Disclosure:

None.

Comments

Log in or sign up to join the conversation.