Cinco de Mayo does not refer to the sinking of a huge Spanish Galleon a couple hundred years ago off of Veracruz, entailing total loss of a multiyear supply of 'mayo' for the Conquistadors wishing more tasteful dressings :)

It might however refer to the submergence on a rotational basis of a number of leading equity sectors, which analysts generally are celebrating as being 'buys' because they're the equivalent of a melting 'frozen Margarita' (sounds good actually). The melting of the stocks sort of dilutes optimism, while sure, it also simultaneously creates better value for new buyers.

However, given that the overall market has yet to discount the real 'lag time' between proposals, enactment and implementation of new Federal growth initiatives, (and while realizing that consumer and industrial loan demand tends to stay at low levels) there seems to be no rush to satiate buyers with many rewards for essentially waiting to slurp down a diluted melted Margarita, as so many did Friday.

For sure these stocks (like Autos, a few Semiconductors and several Oils) will become reasonably safe buys; however we don't have evidence of base building as of yet. In fact that would ideally come 'if' any fail to decline once the broad market presumably takes a significant hit. That would reveal if lots of stocks can be vulnerable to something like what happened with autos and oils of late, drop, and then have a bit of a 'capitulation wave' upon liquidation by any hedge (or even large fund) manager, desiring or compelled, to sell. It is something to contemplate down the road, not now into record levels.

In sum, the market has shown incredible resilience in the face of numerous challenges, on the oil supply-demand front (Saudi production spin failed); at the same time as the Russian-Iranian-Turkish (axis?) takes shape; with the Pentagon nervous about the 'no-fly safe zones'.

The onset of another military weekend did not impede the S&P, while there's no doubt the market, though extended, has tried to work off overbought and extended technicals and valuations through a rotational process. This likely isn't over and while there can be more relief rallies (or even briefly stronger Euro and weaker Dollar on a Macron victory in France) and even new highs; it is still a market poised to defy the excessive near-term optimism.

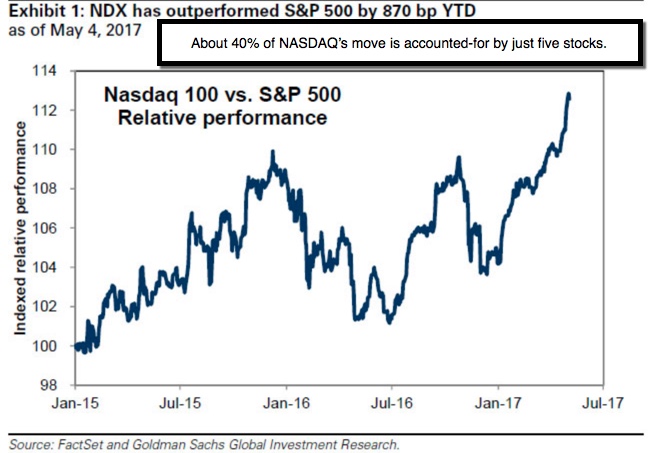

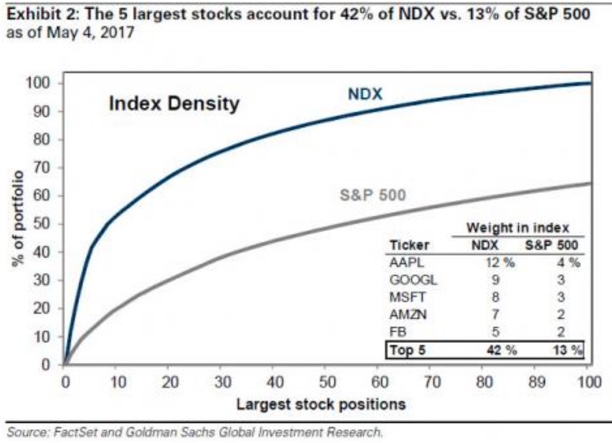

Daily action reflects the market's persistent resilience against meaningful declines, despite some of the prominent Senior Index sectors repeatedly in a defensive mode, or just faltering altogether. How the market accomplishes this involves a tricky combination of rotational corrections; broadening out to (in some cases so-called) lower quality stocks; and maintaining a focus on a handful of issues including the FANG stocks, which accounted for an outsize proportion of the market's gains or stabilization.

It may be like this for the market (in-inverse): following new highs as finally reached for the S&P; eventually the seemingly frightening setback phases (alternating initially); and then a gradual course upwards renews.

The trek will be dependent on outcomes of skirmishes and battles, that will be pending along the way to better times promised not by Napoleon, but by policies that are empowering for growth of our nation, and most importantly, stability of household income growth, which so far falls far shy of promises, or the delusion so many have about prosperity in the US; as a majority of the population is still slugging it out.

So we have new highs barely eked out at last; now enjoy a margarita or three and we'll address markets in the new week. Nothing Draconian occurred up to this report Saturday. The French Election, that may be key to Monday's opening.

|

|

Comments

Log in or sign up to join the conversation.